Level up your open finance game five times a week. Subscribe to the Bankless program below.

Dear Bankless Nation,

We recently closed out Q3. You know what that means?

It’s time for Lucas Campbell to drop his quarterly token report.

You might see evidence of a small bull run in Q3 in the report. Just a revenue increase of 27x for token protocols. No big deal. 😎

Valuations too. Because tokens can be valued. DeFi tokens are protocol shares. They’re capital assets. We value them based on expectations of future value flows.

Guess what the means?

It means our friends on Wall Street can value DeFi protocol tokens the way they value equities. And we made a downloadable institutional friendly .pdf to help them out. So spread the word and send someone this report! The crypto asset class is real and growing like crazy!

The theme this quarter: the Rise of the Ownership Economy—you’ll see it in the data.

This quarter was one for the books.

Special thanks to our friends at DeversiFi for making this report happen. A fantastic place to trade—fast, non-custodial, secured by Ethereum. Try it out!

Let’s get to the goods.

- RSA

Report sponsor: Deversifi—a DEX for serious traders. Trade crypto assets with private transactions & instant settlement without a bank! Start trading now! 🔥

🙏 Sponsor: Zerion – Invest in DeFi from one place. 🚀 (I use this app daily - RSA)

Writer’s Corner

Bankless Writer: Lucas Campbell, Analyst at Bankless

Bankless Q3 Token Report

The Rise of the Ownership Economy

Crypto capital assets experienced explosive growth in Q3. The surge was largely led by the emergence of yield farming as crypto investors had endless opportunities to leverage a range of protocols to earn high-yielding income opportunities.

While the mania subdued towards the end of the quarter, it created a fundamental shift in the way the industry approaches token distributions: give ownership to the users.

It’s the equivalent of Uber distributing equity to anyone that took or gave an Uber ride during its early years or Google giving out shares to anyone who used the search engine. And this distribution mechanism may have profound effects in the decades to come.

Any company or protocol that relies on its users to create value can execute this distribution mechanism to bootstrap those network effects. No one goes on Facebook to look at the content Facebook creates, it only becomes a valuable platform when your friends are on it and everyone starts creating content. This is the beginning of the ownership economy. A new paradigm where the early users of a platform also become the stewards of it.

And crypto capital assets are the backbone of this paradigm shift.

For those still learning about this crypto capital assets, here’s some reading to get you up to speed:

- How to think about crypto PE - January 2020

- Are DeFi tokens worth buying - February 2020

- How to value crypto capital assets - May 2020

- A framework for token value flows - August 2020

In short, crypto capital assets are tokenized assets that represent both (1) economic rights and (2) governance rights over a network or protocol.

A prime example is MakerDAO’s MKR as Maker generates revenue based on the total outstanding debt (i.e. circulating DAI) in the system. The cash flows are distributed to MKR holders via token burns - almost like a company executing stock buybacks. But instead of holding buybacks on a company balance sheet, shares are destroyed to effectively create a universal dividend for all existing holders as everyone’s percentage ownership of the network increases equally. Equally important, MKR also has governance rights where tokenholders can vote on changes to the protocol based on the amount of MKR they hold.

What’s interesting about crypto capital assets is that they have strong similarities to a company’s equity. Public equities represent the rights to a company’s profits along with governance rights in the form of shareholder voting. The difference between the current system and DeFi is the notion of the ownership economy and how the users of the protocol or platform today become the shareholders in the future. What emerges is a significantly more inclusive governance system where the users have influence over the platform they use (and pay for).

While it’s not perfect (token vote is still a plutocracy), we believe this leads to far more inclusive and better aligned systems than the incumbent system.

User ownership was the major theme. If the last quarter saw the rise of crypto capital assets this quarter saw the rise of the ownership economy--rocket fuel for the growth of DeFi.

A Synopsis on DeFi Protocols

Below is a quick synopsis on the DeFi protocols included in this article and their respective revenue mechanisms

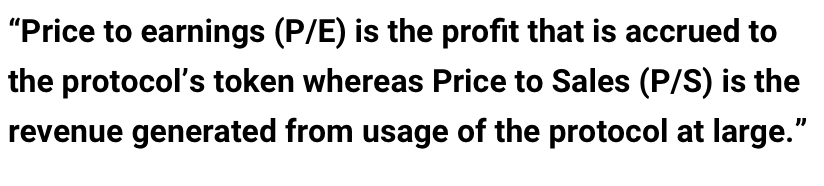

The Shift from Price to Earnings (P/E) to Price to Sales (P/S)

In previous reports, we generally referenced the price to earnings ratio as the metric for valuing crypto capital assets based on their cash flows. However, as we’ve mentioned before, we’re still learning and evolving our understanding of this new asset class.

Thanks to our friends over at Token Terminal and a discussion with Chris Burniske on the Bankless Podcast, one of the major changes is the shift from Price to Earnings (P/E) to Price to Sales (P/S). While many of these protocols are generating revenues, not all of it (if any) accrues to the protocol’s native token - an important distinction to recognize when valuing these assets.

Price to earnings (P/E) is the profit that is accrued to the protocol’s token whereas Price to Sales (P/S) is the revenue generated from usage of the protocol at large.

A great example of this is Kyber Network. While the liquidity protocol is on track to generate ~$10M in revenue from its 0.2% trading fee, the most recent governance proposal states that only 73.5% of that revenue will accrue to KNC holders through a combination of ETH dividends and KNC burns. The remaining ~26.5% is distributed as reserve rebates based on the amount of volume each reserve facilitates. As a result, Kyber’s Price to Sales is ~21 versus a Price to Earnings of ~29.

This nuance becomes more apparent when looking at other DeFi protocols. Kyber’s competitor, Uniswap, charges a 0.3% fee for token swaps and was on track to earn a monstrous $268M in annualized revenue in Q3. However, NONE of that accrues the UNI token as the entirety of the revenues are distributed to liquidity providers. We’ll dive into this more later.

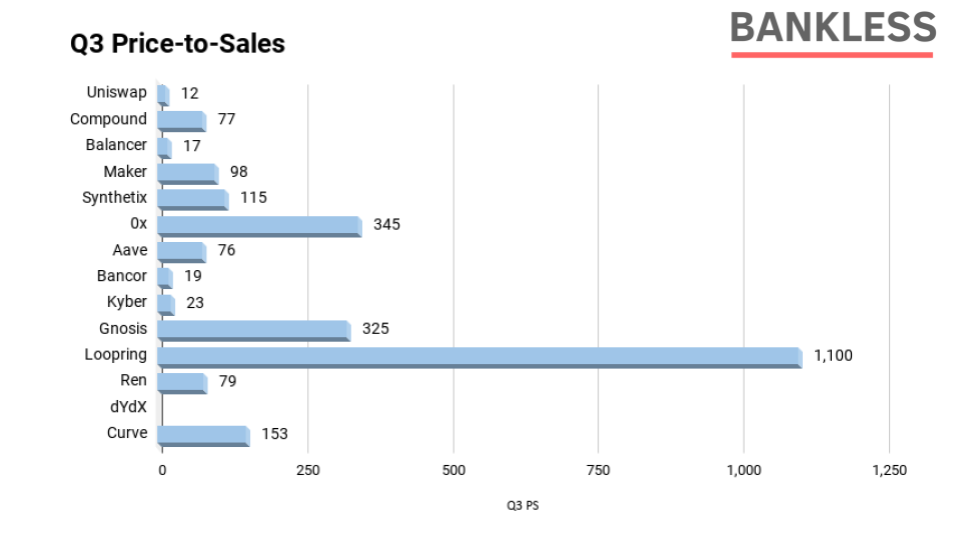

Below is a look at how our money protocols stack up relative to each other in terms of Price to Sales:

(Above) PS Ratio calculated as market cap on September, 30th divided by annualized Q3 revenues. Data via Token Terminal.

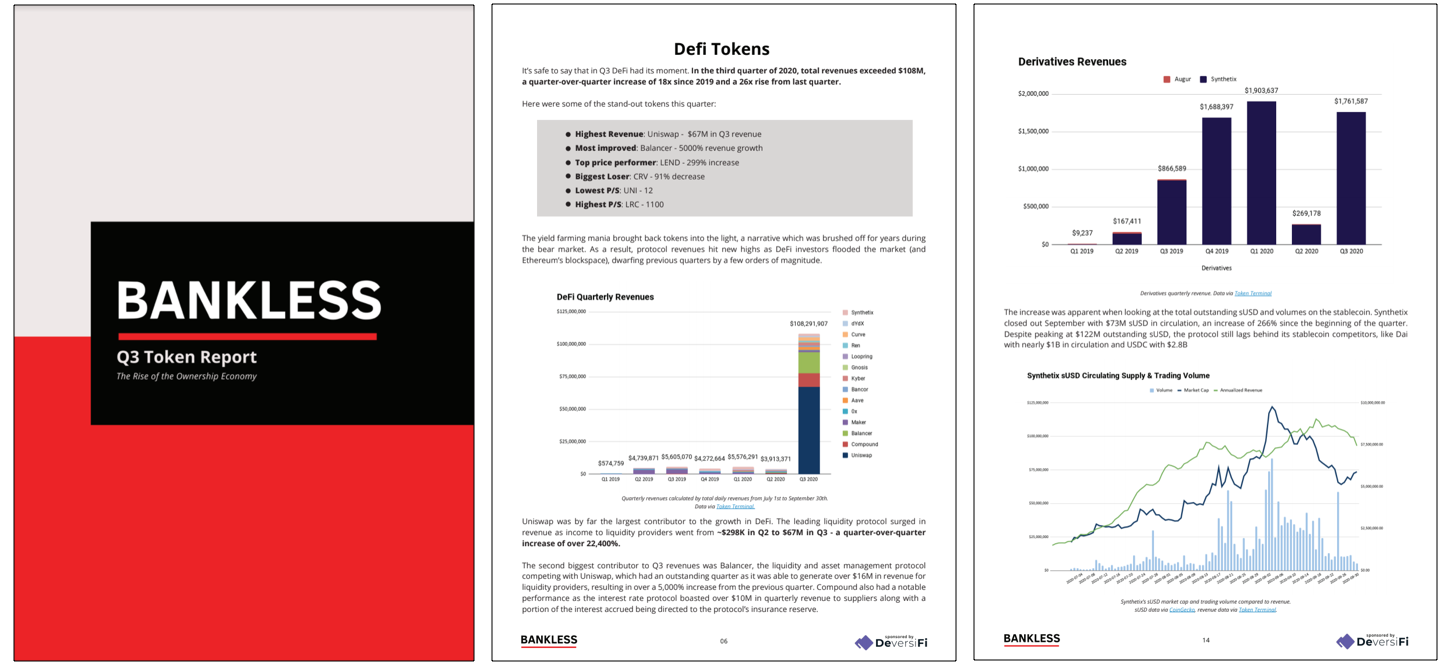

DeFi Tokens

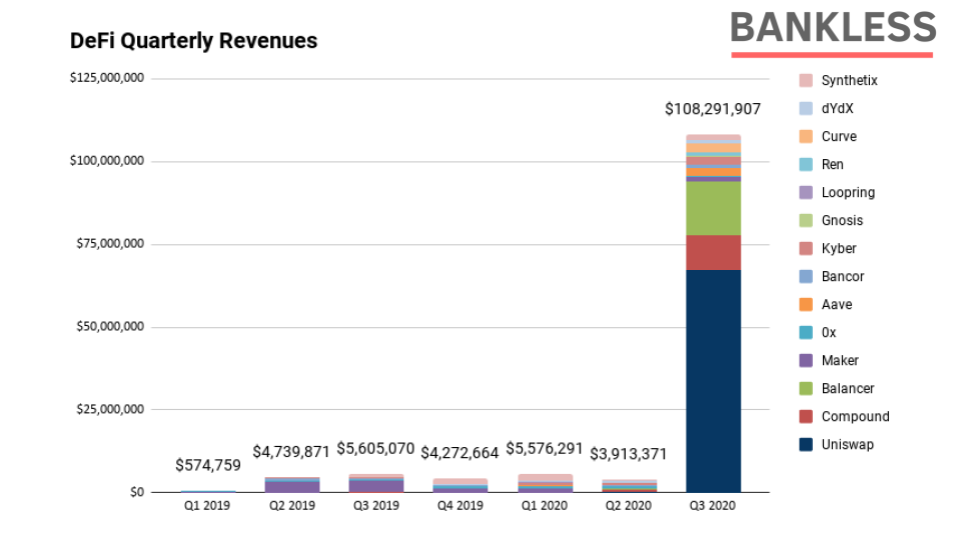

It’s safe to say that in Q3 DeFi had its moment. In the third quarter of 2020, total revenues exceeded $108M, a quarter-over-quarter increase of 18x since 2019 and a 26x rise from last quarter.

Here were some of the stand-out tokens this quarter:

- Highest revenue: Uniswap - $67M in Q3 revenue

- Most improved: Balancer - 5,000% revenue growth

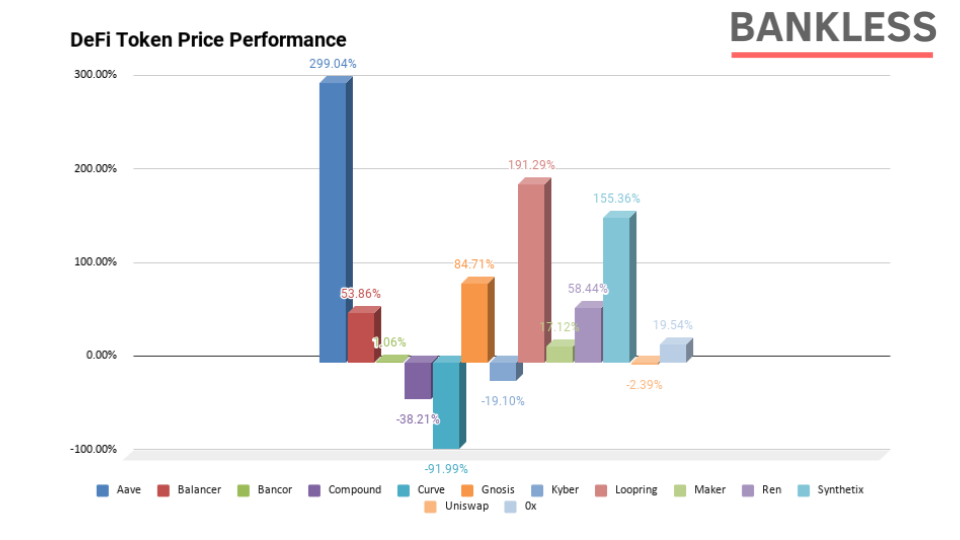

- Top price performer: LEND - 299% price increase

- Biggest loser: CRV - 91% price decrease

- Lowest P/S: UNI - 12

- Highest P/S: LRC - 1100

The yield farming mania brought back tokens into the light, a narrative which was brushed off for years during the bear market. As a result, protocol revenues hit new highs as DeFi investors flooded the market (and Ethereum’s blockspace), dwarfing previous quarters by a few orders of magnitude.

(Above) Quarterly revenues calculated by total daily revenues from July 1st to September 30th. Data via Token Terminal.

Uniswap was by far the largest contributor to the growth in DeFi. The leading liquidity protocol surged in revenue as income to liquidity providers went from ~$298K in Q2 to $67M in Q3 - a quarter-over-quarter increase of over 22,400%.

The second biggest contributor to Q3 revenues was Balancer, the liquidity and asset management protocol competing with Uniswap, which had an outstanding quarter as it was able to generate over $16M in revenue for liquidity providers, resulting in over a 5,000% increase from the previous quarter. Compound also had a notable performance as the interest rate protocol boasted over $10M in quarterly revenue to suppliers along with a portion of the interest accrued being directed to the protocol’s insurance reserve.

(Above) Quarterly Price Performance. Data via Token Terminal

Even though DeFi had a phenomenal quarter in terms of revenue, price performance was a mixed bag across the board. Last quarter’s best performer, LEND, continued its dominance with a 299% increase in Q3. The rising interest rate protocol announced Aavenomics, a new token economics upgrade focused on introducing a new token (at a rate of 100:1), yield farming incentives, and decentralized governance along with launching Credit Delegation and other innovative features.

The second best performer in Q3 was Loopring, the L2 solution featuring a built-in DEX for near-instant, cost efficient trades. It seems that the market garnered some interest for the L2 protocol as a result of the increasing gas fees on Ethereum’s base layer. This move seems to be more speculative than driven by tangible usage as revenue for Loopring dropped by 50% from last quarter, a decrease from $115K to $57K.

The last notable performer was Synthetix which, per usual, highlighted another quarter filled with new products & releases. Synthetic rolled out 5 official releases which included improvements to binary options, further integrations on ETH collateral, limit orders on Synthetix.Exchange, new indexes, trading & volume incentives, trialing the Optimism L2 solution, and more. You can learn about all the upgrades on their official bog.

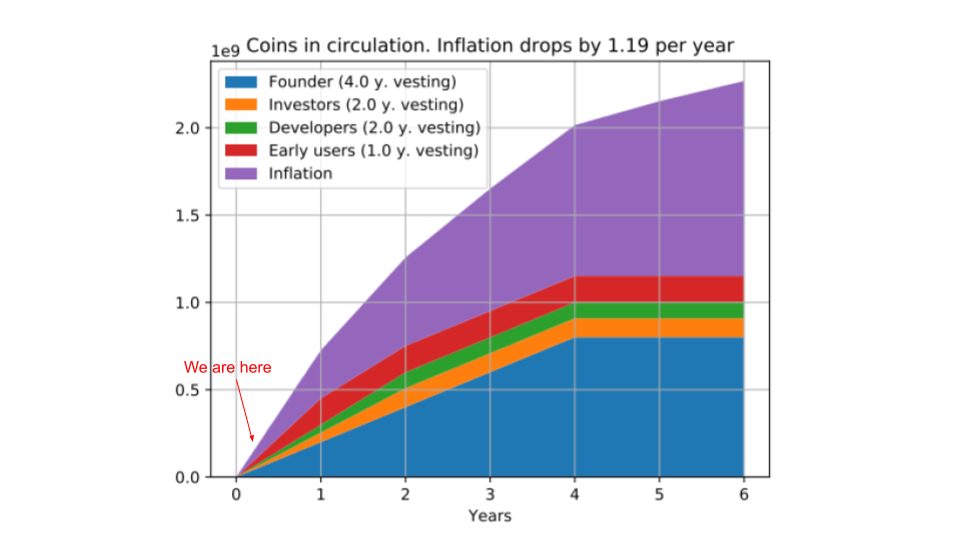

On the other hand, the worst performer was Curve’s CRV, the stablecoin-focused AMM. Despite the liquidity protocol being highly successful, the protocol’s native token is fighting against a hyper-inflationary supply schedule, which has led it to struggle in terms of price performance. According to CoinGecko, only ~83M of the total 3.3B CRV is in circulation, meaning there’s another 97.5% of the supply awaiting to come into circulation over the next 5 years. Unless there’s a governance change on the supply schedule (there’s discussions here), it seems that CRV will continue to fight an uphill battle over the coming years.

(Above) Curve’s CRV supply schedule via Curve Guides.

Ether as a Capital Asset

While ether is not commonly referenced as a crypto capital asset we argue it is becoming one. (See the triple point asset and Ether: the birth of a digital bond.) Ether represents the future right to cash flows on Ethereum through two mechanisms. In the upcoming Eth2 upgrade, holders will be able to earn transaction fees (plus ETH issuance) by becoming a validator on the network and staking ETH. Additionally, with the introduction of EIP1559, all ETH holders will earn a slice of Ethereum’s revenue via fee burns when network usage is high.

That said it’s important to recognize that ETH doesn’t represent on-chain governance rights -- at least in the same way as many DeFi protocols. Eth2 validators have soft governance rights in the same lens as traditional hardware miners. In other words, Eth2 valdiators will always retain the right to choose which software they run, allowing them to oppose any contentious code changes by simply not running the code and opting into the code that better aligns with their views.

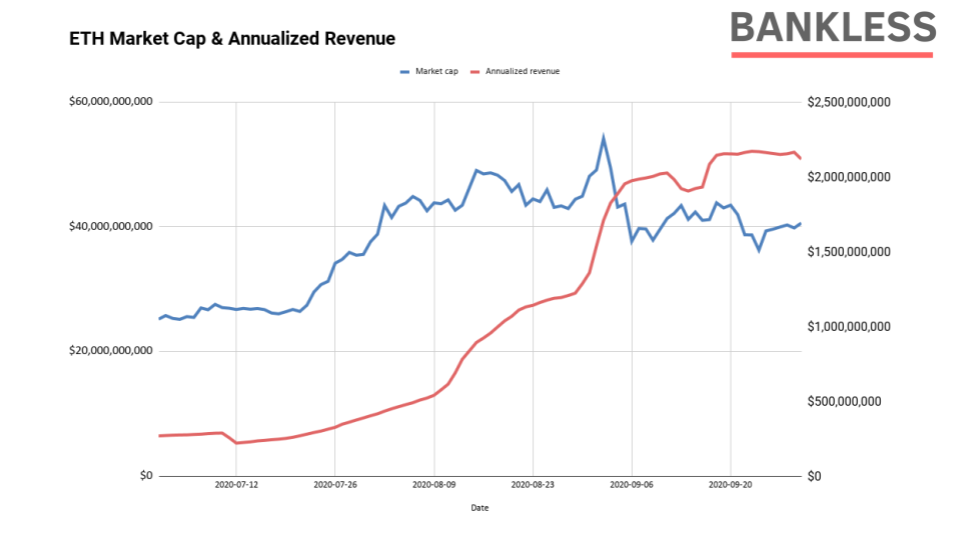

(Above) ETH market cap compared to annualized transaction fee revenue. Data via Token Terminal.

The yield farming mania in Q3 drove Ethereum’s transaction fees to new highs. In July, Ethereum was on track to generate $284M in annualized revenue from fees. Fast forward to September and the network was averaging $2.0B in annualized revenue, an increase of 610% from the beginning of the quarter. And while price performed well over the same period, surging 61% in Q3, revenue substantially outpaced the asset as the PS ratio decreased from ~93 to only ~19.

For reference, the average PE ratio in the S&P 500 is ~22. Despite the fact that Ethereum continues to show a promising future as a platform for financial innovation, the market may be undervaluing the asset severely as there’s no shortage of future growth and the network is generating substantial cash flows for future ETH holders.

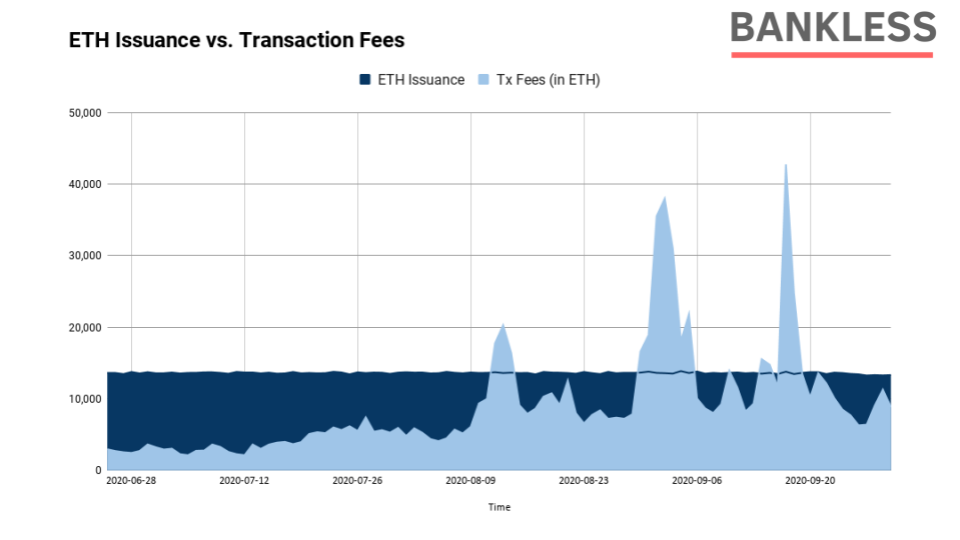

Ethereum transaction fees also outstripped issuance on multiple occasions throughout the quarter. Meaning, that under EIP1159, there may have been a few instances where ETH experienced a deflationary environment - a strong indicator for a demand for blockspace and the network at large.

(Above) ETH issuance versus daily transaction fees. Data via CoinMetrics

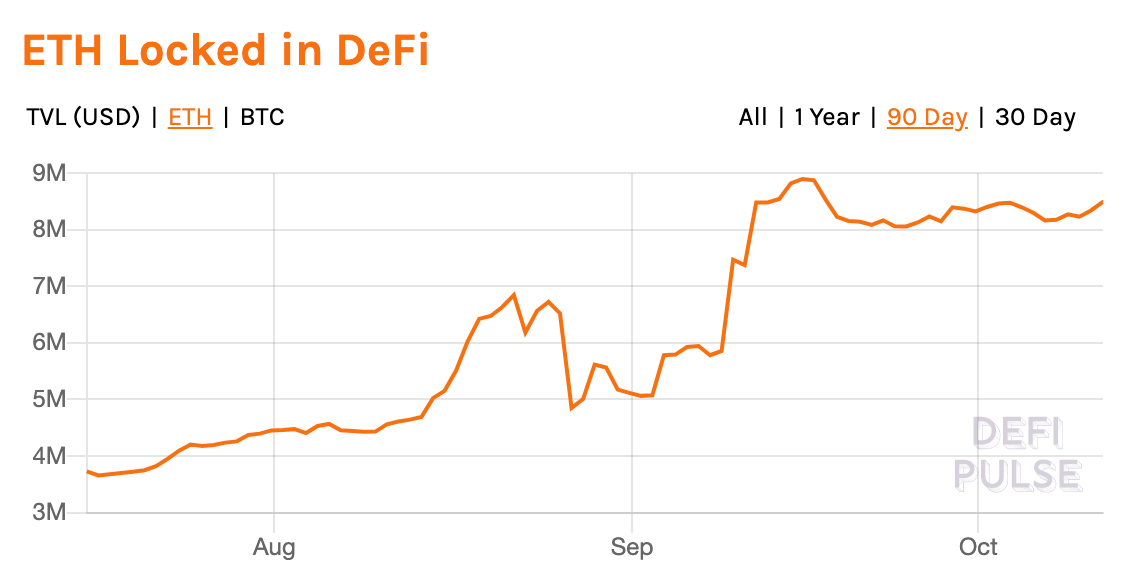

The last bull indicator for ETH is the demand for ETH as trustless collateral in decentralized finance. While this metric lagged for the most part of the year, there’s been a resurgence in ETH’s usage in DeFi.

At the beginning of the quarter, 3.284M ether was locked in DeFi protocols, roughly ~3% of the total supply. In September, this number rose to 8.481M, soaking up over 7.5% of all ETH in circulation. This increase was primarily driven by Uniswap as the protocol strictly featured ETH pairs for UNI yield farming. Prior to launching its native token, there was ~1M ETH locked in the liquidity protocol. Almost immediately after launching UNI farming, ETH locked surged to 3.5M ETH.

The other driver was Maker which soaked in another 1M ETH in Q3 as the protocol effectively offered free leverage on ETH for the most part of the quarter.

(Above) ETH locked in DeFi as calculated by DeFi Pulse.

All in all, Q3 was a notable quarter for ETH as revenue and demand for the asset as trustless collateral simultaneously hit new highs all while ETH performed rather positively.

Looking forward, expect the launch of Eth2 Phase 0 and EIP1559 to make significant progress over the coming months (if not weeks)!

DeFi Sector Overview

Decentralized Exchanges

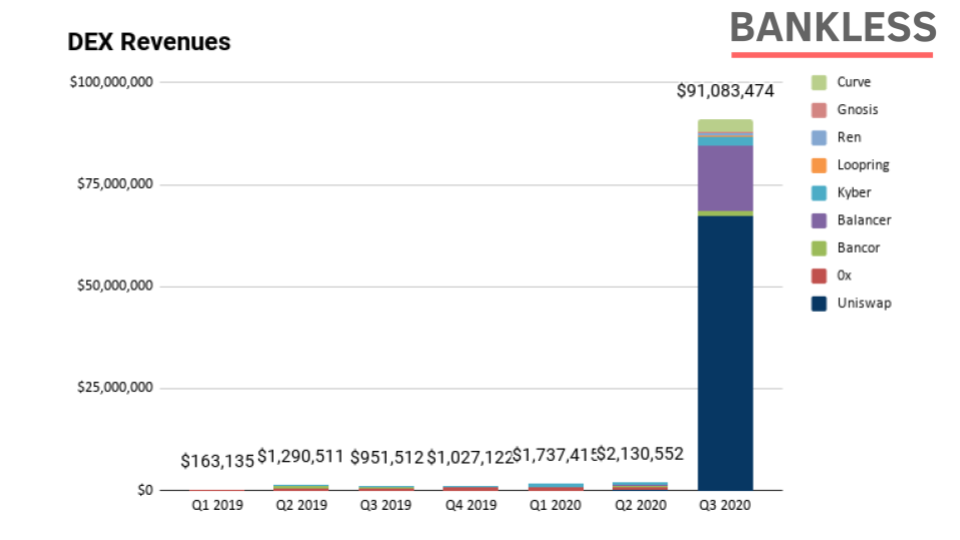

DEXs took the cake for Q3 as the sector raked in over $91M in total revenue.

Uniswap dominated the field, representing roughly 73% of the aggregate revenue among all other liquidity protocols. While the protocol somewhat struggled to compete in total liquidity with SushiSwap’s attempted vampire attack, Uniswap fought back by introducing UNI tokens in early September along with the now-famous retroactive UNI airdrop to all users.

(Above) DEX quarterly revenue. Data via Token Terminal

The other major contributor to the DEX sector was Balancer, the adaptable asset management and liquidity protocol. On an annualized basis, Balancer is on track to earn $64M to its liquidity providers - an impressive accomplishment given it only launched on mainnet in the Spring of 2020.

The only other liquidity protocols to generate a 7-figure return in Q3 were Curve, Kyber and Bancor who inched into the rankings with $1.1M. On that, Curve’s hyper-efficient AMM was able to bring in $3M in quarterly revenue to LPs with Kyber generating $2.2M.

While Kyber ranked 4th in the standings, it’s the highest earning protocol distributing a portion of its revenue to KNC holders. Those that stake their KNC and participate in governance on a weekly basis currently have the right to 67.3% of all revenue. Interestingly, participants earn those rewards in ETH - the only protocol in DeFi structuring rewards this way.

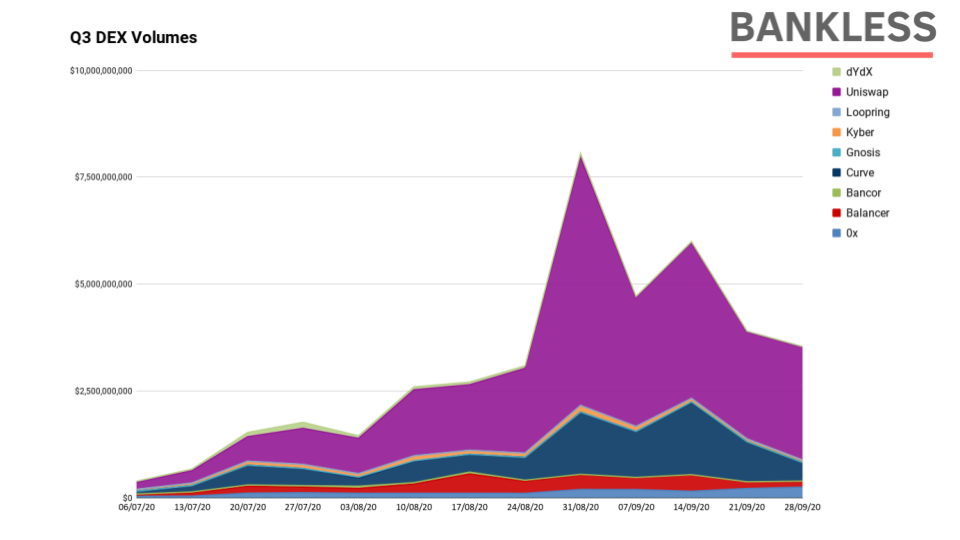

(Above) Weekly DEX volumes in Q3. Data via Dune Analytics.

While SushiSwap surpassed Uniswap in terms of total liquidity for a brief moment, Uniswap continues to act as the home for Ethereum-based DEX trades. In Q3, Uniswap processed over $25B in total volume with an average of nearly $2B per week. The next closest competitor was Curve which facilitated over $8.3B in the quarter while averaging $639M per week followed by Balancer with $2.7B in total and $210M per week.

The only other protocols to amass over $1B in quarterly volume was 0x and Kyber with $1.7B and $1.1B, respectively.

Uniswap

With Uniswap dominating the DEX sector in terms of volumes and earnings along with the recent introduction of the UNI token, it’s interesting to consider the potential earnings for the protocol.

For those that remember, the launch of Uniswap v2 introduced a protocol charge with an on/off switch (governed by UNI holders). If the protocol charge is switched on, the trading fee allocates 0.05% of the 0.30% swap fee towards a treasury to be directed by a decentralized governance process. The remaining 0.25% is allocated to liquidity providers. At today’s revenue projections of $268M per annum, this represents roughly $44.6M in capital available to be governed by UNI holders.

It’s important to note that this treasury is largely meant to fund and incentivize community contributions and the long term development and growth of the Uniswap protocol. This could be to pay developers, marketing teams, community managers, and whatever else UNI holds believe is necessary.

That said, there’s nothing stopping UNI holders from voting in some sort of profit distribution in the form of dividends or burns. Let’s imagine that Uniswap governance elected to distribute 20% of the treasury at today’s rate in the form of ETH dividends (similar to its competitor Kyber), this in turn would generate $8.9M to UNI holders, giving Uniswap a lofty PE ratio of 374 at its $3.33B fully diluted valuation.

Increase this to 50% of the treasury’s annualized allocation, and UNI’s PE ratio drops to 147.

Obviously this is just a simple thought experiment and should be taken with a grain of salt, but it’s interesting to consider given the current market dynamics.

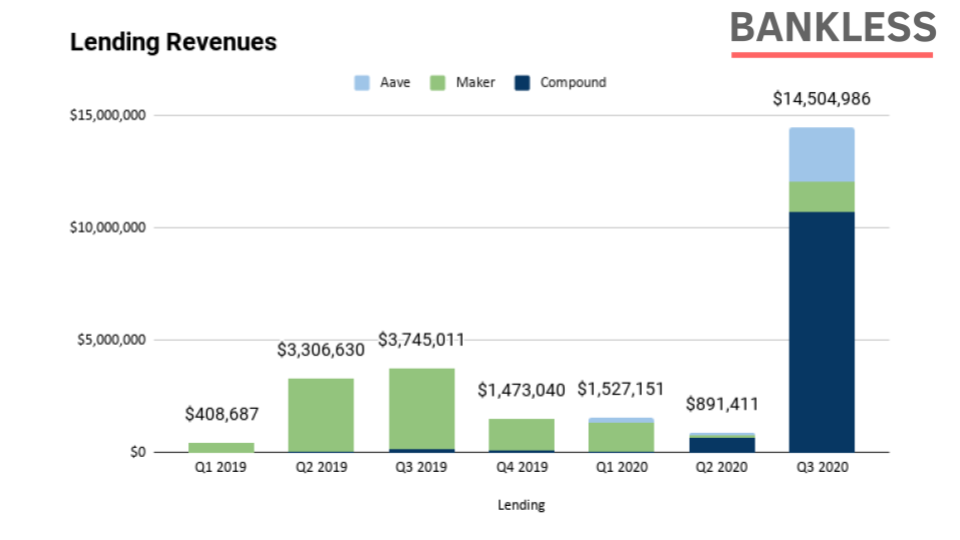

Lending

After seeing a steep decline from Q1 to Q2 earlier this year, the lending sector bounced back as all three major protocols saw an increase in revenue from the previous quarter. Compound launched COMP liquidity mining back in mid-to-late June and effectively kickstarted the yield farming mania.

As a result, both value locked and revenue rose as DeFi investors swamped the interest rate protocol with capital in an effort to scoop up some COMP tokens. Compound generated over $10M in interest to the protocol’s suppliers along with tucking a way of portion of it into each market’s insurance reserve.

Compound’s main competitor, Aave, is also coming off a strong quarter beyond price performance. The money markets protocol multiplied its revenue by over 20x in the quarter, and interestingly enough, has yet to launch yield farming. However, the recent launch of Aavenomics will change this with the introduction of Ecosystem Incentives. While the exact numbers have yet to be set in stone, you can follow the discussion here and learn more about the token economics & governance upgrade here.

(Above) Lending quarterly revenues. Data via Token Terminal

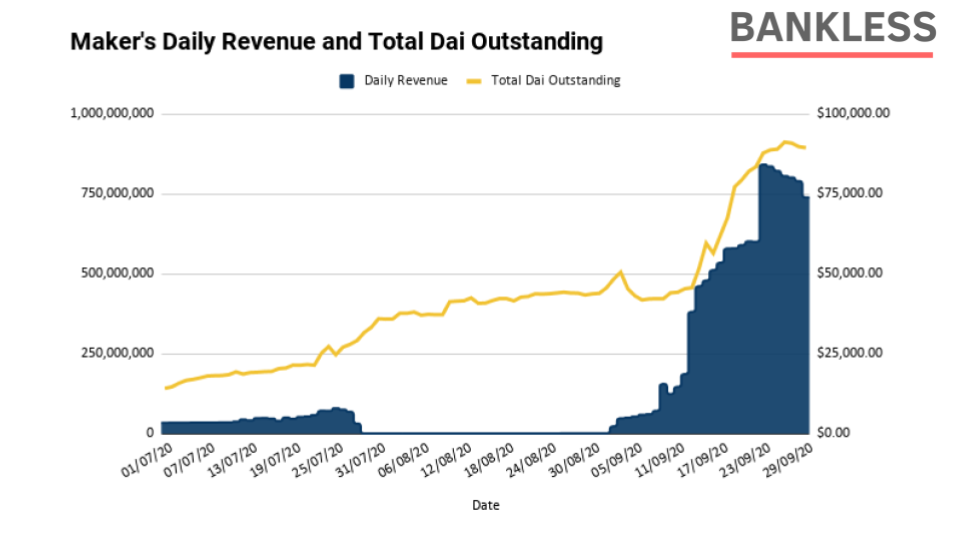

Finally, let’s talk about MakerDAO. After months of no stability fee and effectively offering free leverage on ETH (as well as cheap leverage on other assets), the lending protocol behind Dai is now back online in full force.

With most borrow rates sitting around 2 - 4% and nearly $1B in Dai circulating Ethereum, the protocol is on track to generate nearly $20M in annualized revenue. Importantly, with the Dai Savings Rate (DSR) still sitting at 0%, the entirety of those revenues will accrue to MKR via token burns. At the current rates, Maker is on track to burn 3.7% of the token supply per annum - assuming all else constant.

Notably, the demand for Dai has seen a substantial increase since the yield farming mania. In Q3 alone, the amount of Dai in circulation increased from 141M to 894M, a gain of 533% in a few short months. Naturally, the increase in circulation Dai has led to an increase in daily revenue from stability fees. After re-introducing the stability fee in September, Maker was earning $80,000 per day in earnings for MKR holders, driving the token’s PE ratio to new lows of ~30 as the price of MKR continues to stagnate at around ~$540M.

(Above) Maker’s daily revenue compared to total Dai supply. Revenue data via Token Terminal, Dai data via Dune Analytics.

The governance community is also working on a handful of new improvements to the protocol in discussions, some of which are worth keeping an eye on. These include the Flash Mint Module, improving SourceCred Funding, introducing Strategic Reserve Funds, Governance Contract Redesign, the Debt Ceiling Instant Access Module, and more.

They’ve also opened up a few governance polls to gauge the community’s sentiment on BAL and YFI collateral as well as integrating real world assets into the protocol.

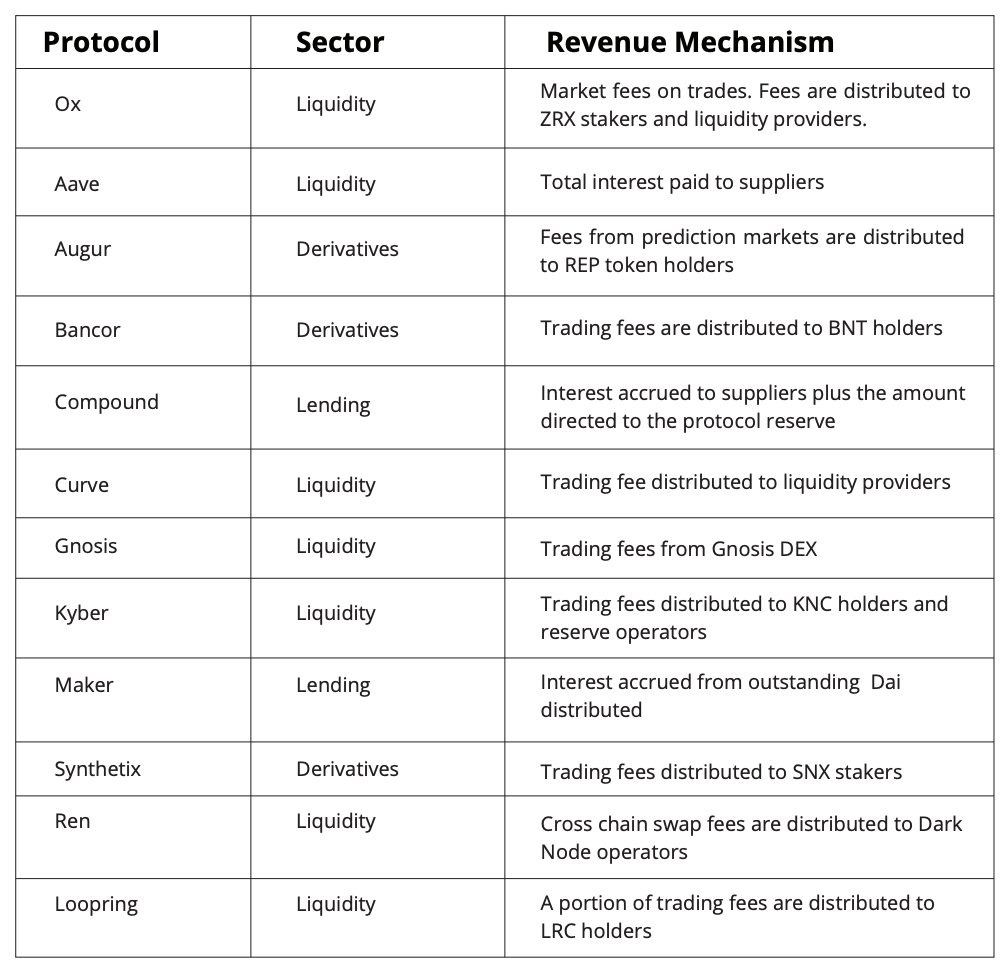

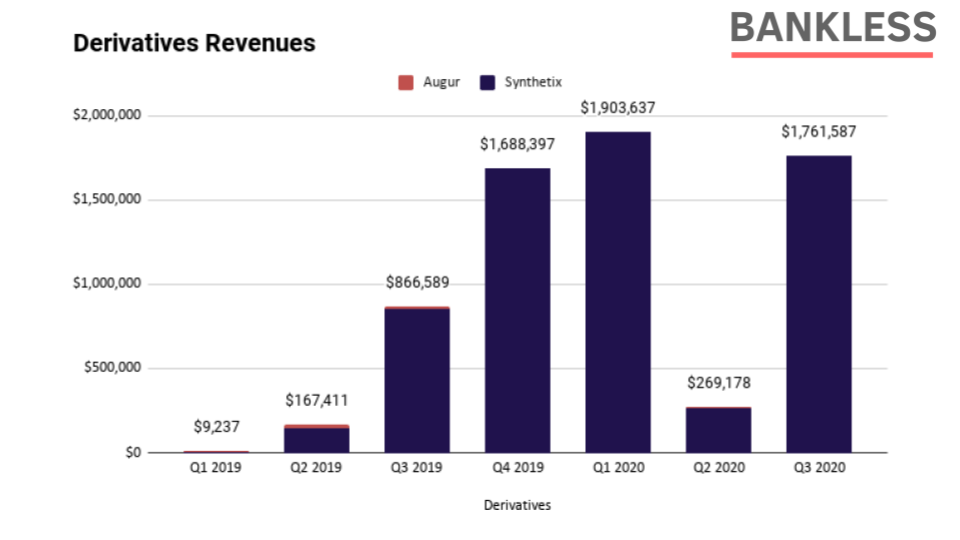

Derivatives

The derivatives sector is also making a comeback. While not depicted in the graph below, the launch of Augur v2 along with UMA gaining momentum, the derivatives market is starting to shape up nicely.

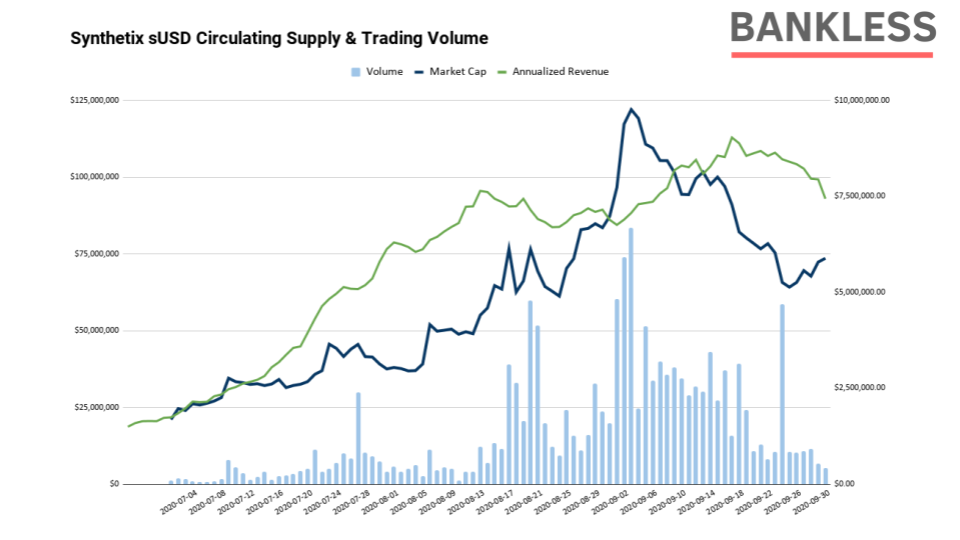

However today, the sector continues to be dominated by Synthetix, the permissionless derivatives protocol powered by SNX. After fixing its front-running issue in Q1/Q2 which disproportionately skewed earnings, the protocol was setback as revenues closed out to only $269,000 in Q2. Fortunately, the protocol bounced back in Q3 after seeing a strong demand for its crypto-native stablecoin, sUSD. In total, the protocol generated $1.76M in Q3 revenue alone, nearly surpassing its previous ATHs even with the disproportionate earnings.

(Above) Derivatives quarterly revenue. Data via Token Terminal

The increase was apparent when looking at the total outstanding sUSD and volumes on the stablecoin. Synthetix closed out September with $73M sUSD in circulation, an increase of 266% since the beginning of the quarter. Despite peaking at $122M outstanding sUSD, the protocol still lags behind its stablecoin competitors, like Dai with nearly $1B in circulation and USDC with $2.8B.

(Above) Synthetix’s sUSD market cap and trading volume compared to revenue. sUSD data via CoinGecko, revenue data via Token Terminal.

Regardless, Synthetix features more than just a crypto-native stablecoin. The protocol supports dozens of synths like crypto assets and indexes for investors to speculate on, binary options, and the highly anticipated Synthetix Futures which is set to launch later this year. We’ll also see the launch of Kwenta, a new exchange built on Synthetix where users will be able to trade the full suite of Synths as well as a range of charting and performance tools to empower traders.

Emerging Sectors

Yield Aggregators and YFI

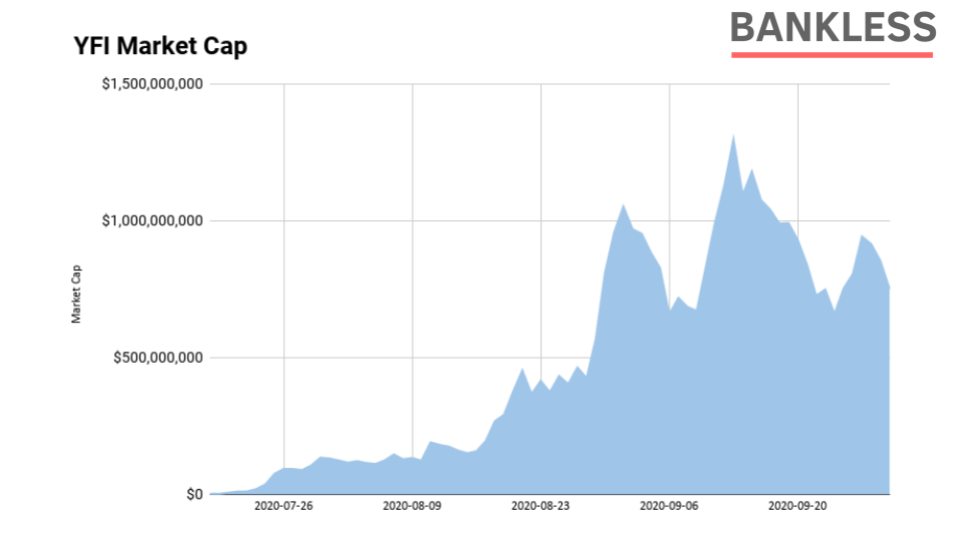

It would be a disservice to the DeFi community if we didn’t mention yEarn and the YFI token. Even though the protocol generates earnings for the YFI token via the governance module, our friends over at Token Terminal are still working on supporting the protocol.

While Compound was the forefather of the yield farming mania, YFI kickstarted the Fair Launch Movement - a token distribution mechanism building off the altruism of Satoshi Nakomoto and BTC where everyone has the same opportunity to access the tokens. No VCs, no founders allocation, no vesting schedules, simply equal opportunity for everyone.

And this distribution schedule resulted in YFI’s meteoric rise into DeFi. After distributing the entirety of the token's supply over two short weeks, the yield aggregator went from 0 to $1.2B at its peak in less than 2 months. yEarn became a unicorn in less than two months since distributing its token to the public, something unprecedented even in the world of DeFi.

(Above) YFI market cap. Data via CoinGecko

What started as a yield aggregator expanded into credit, insurance, venture capital, and more. Founder Andre Cronje simply does not stop building. Now, with a viral community supporting the protocol and a paid team through decentralized means, yEarn is set for another exciting quarter. Be on the lookout for the new vault design, new yield optimization strategies, the potential for Vaults to act as privacy mixers as well as any other products Andre crafts up in his head.

Insurance and NXM

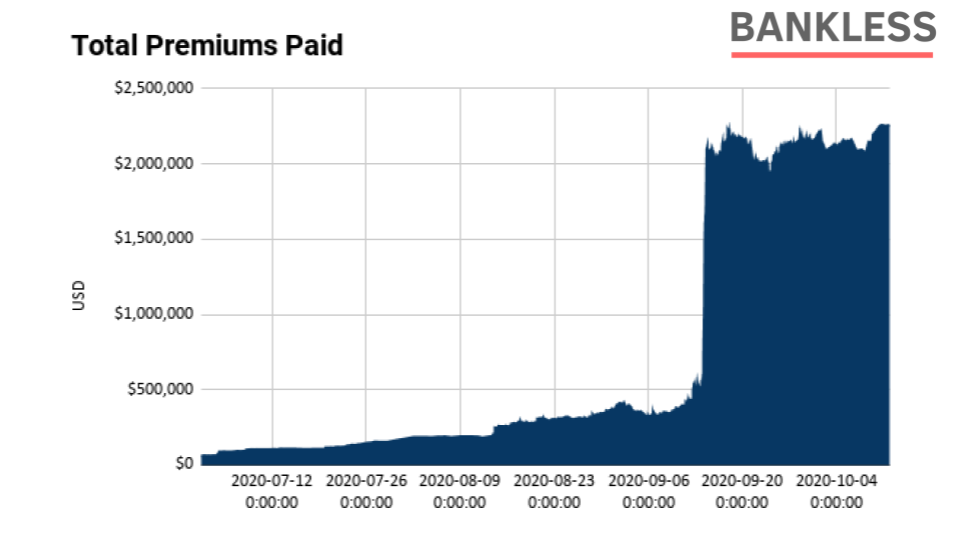

Nexus Mutual also broke out in Q3. After implementing pooled staking, the insurance alternative skyrocketed to new highs in virtually every metric. The yield farming mania also aided in its growth as investors looked to protect their capital from any potential smart contract bugs while they earned high double digit, triple digit, and even four digit APYs.

In Q3, Nexus Mutual expanded total active covers from $5.2M to $239M. The mutual is now responsible for insuring ~2% of all value locked in DeFi, a substantial increase from previous periods. As a result of the increase in active covers, Nexus Mutual has now collected over $2M in premiums from covers while having only paid out less than $35K in valid claims.

Despite the protocol covering hundreds of millions in capital, earning millions for NXM stakers and holders, the mutual has only paid out a low five figure sum in claims.

(Above) Total premiums paid for Nexus Mutual covers. Data via NexusTracker.

For reference, the capital pool currently holds over $80M in ETH and DAI, up from $4M at the beginning of July. With that, the NXM token has performed substantially well as the active covers, premiums, and the capital pool surged to new highs. After boasting a mere $17M market capitalization at the beginning of the quarter, NXM grew to a sizable $262M, an increase of 1,441% in a few short months.

Looking forward: Untokenized Protocols & Applications

With tokens resurging back into the crypto narrative, it may be wise to identify some of the remaining untokenized protocols and applications with strong product market fit that haven’t yet released a token:

- dYdX

- InstaDapp

- Opyn

- Set

- Zapper

- Zerion

It will be no surprise if any of these products look to tokenize in some way as they all have investors who will eventually look for an exit. Given the success of Q3, we should expect a handful of future token launches in the coming months.

Conclusion

With DeFi revenue up 26x from the previous quarter and token prices appreciating rapidly, it’s safe to say that anyone invested in DeFi this past summer is in a good mood. Despite the drawback in September, almost every fundamental metric surged to new highs over the course of Q3. Whether they sustain these numbers into the next quarter is another question, but the long term looks bright for our bankless financial system.

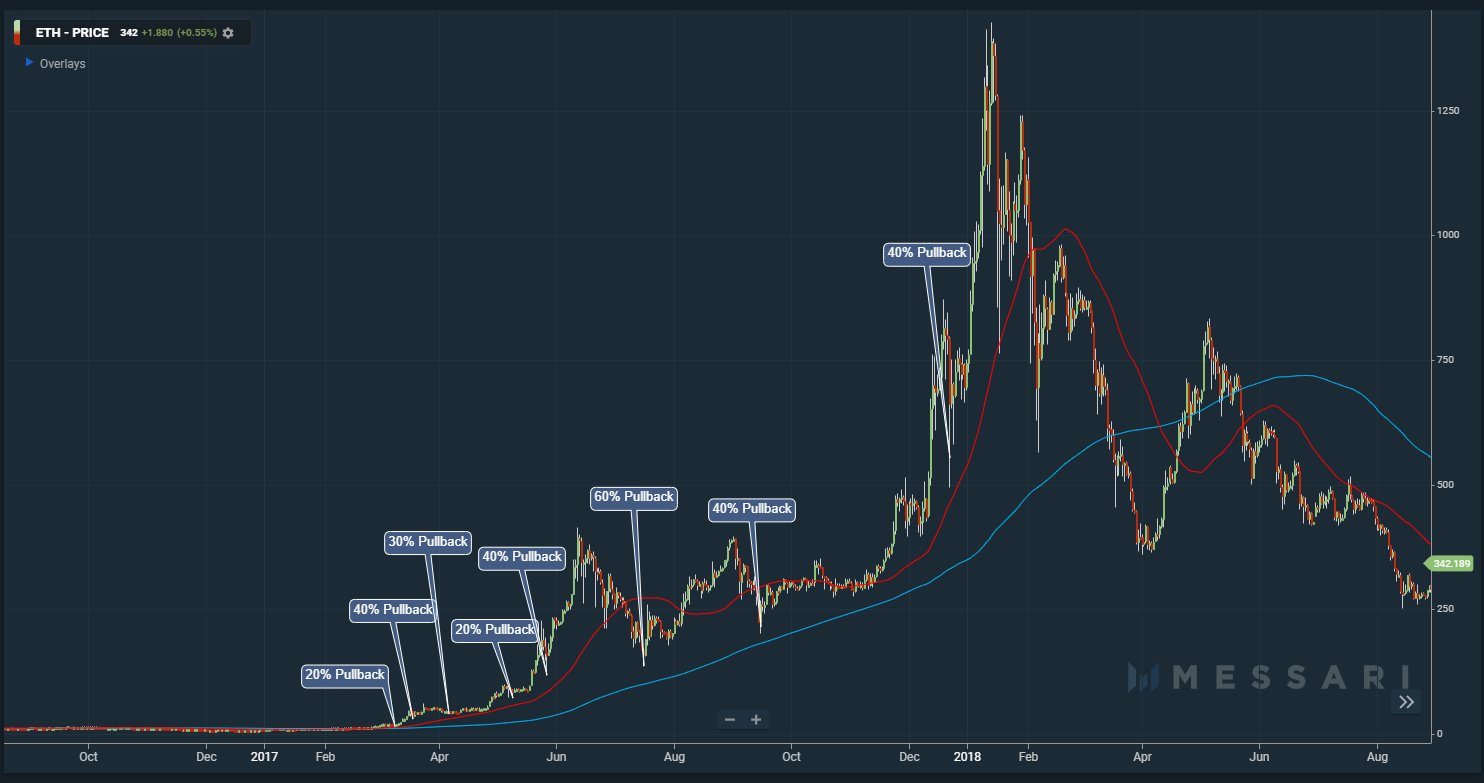

While many may be somewhat concerned about the current downturn with some DeFi tokens down over 50%, this is healthy given the massive runup that lasted for months. For reference, in the 2016-2017 bull cycle, Ethereum experienced over half a dozen -30% drawdowns.

(Above) ETH price pullbacks during 2017 bull run. Source: Messari Twitter

This is only the first one for DeFi.

We believe we’re in the early innings of a multi-year bull cycle. However, the gains will not be distributed evenly across tokens. It’s important for savvy investors to analyze this report to see which protocols are generating substantial revenues, where they extract value to token holders (and where they could if they don’t), and how they compare to the relevant fundamental metrics within each sector (i.e.Volumes for DEXs or Dai outstanding for Maker).

In Q3, we saw the rise of the ownership economy in DeFi and the massive growth that came with it. Each quarter brings new opportunities to this emerging asset class.

You just have to find it.

This paradigm shift in finance is full steam ahead.

Special thanks to Ryan Sean Adams, David Hoffman, Henri Hyvärinen, and the Token Terminal team for all the help on this report and the fantastic support from DeversiFi!

DISCLOSURE

The author of this report owns the following tokens: ETH, YFI, UNI, MKR, SNX, REN, BAL, COMP, CRV, AAVE, NXM

The author does not own the following: ZRX, KNC, BNT, LRC, GNO, SUSHI, NEC

Action steps

Evaluate how your favorite DeFi tokens stack up to their peers

Try out DeversiFi exchange and thank them for sponsoring this quarter’s report!

Read previous Bankless pieces on crypto capital assets & valuation frameworks

How to think about crypto PE - January 2020

Are DeFi tokens worth buying - February 2020

How to value crypto capital assets - May 2020

A framework for token value flows - August 2020

Author Bio

Lucas Campbell is an Analyst for Bankless and leads growth at DeFi Rate. He also engages with teams on token economic & governance design through 🔥_🔥 (Fire Eyes DAO), working with industry-leading projects like Aave, Rocket Pool and others.

Subscribe to Bankless. $12 per mo. Includes archive access, Inner Circle & Badge.

🙏Thanks to our sponsor

Zerion

Zerion is the easiest way to manage your DeFi portfolio. Explore market trends, invest in 170+ tokens, view returns across wallets and see your full transaction history on one sleek interface. They’re also fully bankless, which means they don’t own your private keys and can’t ever access your funds. I use this app daily! Start exploring DeFi with Zerion on web, iOS or Android. 🔥

- RSA

P.S. Don’t forget to get check out Zerion’s new Uniswap integration. 🦄

Not financial or tax advice. This newsletter is strictly educational and is not investment advice or a solicitation to buy or sell any assets or to make any financial decisions. This newsletter is not tax advice. Talk to your accountant. Do your own research.

Disclosure. From time-to-time I may add links in this newsletter to products I use. I may receive commission if you make a purchase through one of these links. I’ll always disclose when this is the case.