Dear Bankless Nation,

Valueless governance tokens.

That’s what most DeFi protocols used to rise to prominence in 2020.

Token holders strictly have governance rights. Nothing else.

The giants like Uniswap and Compound used this model to fuel their growth to billions. But COMP and UNI are “valueless” governance tokens. There’s no direct economic benefit—like a right to cash flows—for holding them.

The model isn’t ideal, but was necessary to avoid regulatory scrutiny. And it allowed these protocols to tokenize faster. Of course, most valuation models assume token holders will eventually vote in cash flows. We still subscribe to this thesis.

But even so, the valueless governance model has diminishing returns. It lacks fundamental demand drivers. Worse, valueless governance tokens paired with large token emissions are a recipe for disaster for stakeholders.

Price will go down. 📉

This is playing out now. Despite the continued growth for these protocols over the past year, major DeFi 1.0 tokens who have the valueless governance token model didn’t perform well.

But there’s a new token model in town: veTokens.

Pioneered by Curve’s CRV, veToken model is instilling value into valueless governance tokens.

Is this the future of DeFi token design?

Have bad token designs suppressed DeFi prices and is this the fix?

You need to level up on this new mechanism.

Ben dives into everything you need to know about veTokens.

- RSA

Why Traditional DeFi Token Models Are Flawed

Despite 2021 being a banner year for crypto markets, with continued parabolic growth in TVL across multiple ecosystems, most DeFi tokens underperformed relative to benchmarks like ETH.

This may seem puzzling at first glance, as many DeFi protocols have generated millions in revenue and seen tremendous growth in usage and adoption of their products.

However, it’s my opinion that the main driver of the sector’s underperformance has been tokenomics. The early models of DeFi token design are fatally flawed and have led to a massive destruction of value that has come at the expense of retail investors.

Let’s unpack this by looking at the supply and demand dynamics of the “TradToken” design.

Demand-Side Dynamics for DeFi Tokens

A common pattern we saw in DeFi token design for projects that launched before mid-to-late 2021 was the “valueless governance token” model.

With this model, token holders are solely entitled to governance rights. While this may have been a way to avert regulatory scrutiny, and governance is certainly an incredibly valuable right, this meant that holders have no claim on cash flows, and the token provides no utility or perks to any stakeholders within the protocol; meaning that aside from speculation, there is no underlying demand for the token.

Supply-Side Dynamics for DeFi Tokens

As we know, much of DeFi’s growth over the past year and a half has been fueled by liquidity mining. While it’s often done at the product level, such as with a DEX or money market, many protocols have also incentivized liquidity for their native token through token emissions. While it’s important for a token to have deep liquidity, these programs have often been taken to the extreme to attract yield farmers, resulting in inflation rates that would make Jay Powell blush, and leading to perpetual sell-pressure on the underlying token.

It doesn’t take a PhD in economics to see why DeFi tokens would underperform: They have a massively inflating supply with no demand to help offset this.

However, there is hope on the horizon as alternative token models have begun to gain traction and acceptance among DeFi communities.

The Rise of the veToken Model

One such model has been the “ve (vote-escrowed) model. Pioneered by Michael Egorov of Curve Finance, the ve-model involves token-holders taking on the risk of locking their tokens in exchange for specific rights, such as governance power, within a protocol.

Fueled in large part by the “Curve Wars” and despite being a “DeFi 1.0” coin, the price of CRV, and its largest holder, CVX, bucked the broader sector trend and outperformed in Q3 and Q4 2021, returning 265.4% and 1085.7% respectively, relative to a 12.2% gain for DPI.

As a result of this outperformance, DAOs across DeFi already have or are planning to, overhaul their tokenomics to pivot to a veModel.

This begs the question:

- Why has this model been so successful?

- What benefits does it provide to a protocol?

- What are some of the drawbacks of ve-tokenomics?

- Does a project switching to ve-tokenomics mean it’s number will go up?

Let’s find out.

The First veToken – veCRV

At a high level the ve-model is relatively simple: Holders are trading short-term liquidity in exchange for benefits within a protocol.

Let’s explore this in practice by looking at the pioneer of the model, Curve.

Curve is a decentralized exchange that is optimized for swapping between “like-assets,” which are assets that are intended to have the same, or similar, price. This includes facilitating trades between stablecoins, such as USDC and USDT, or a token and a derivative, such as ETH and stETH (ETH staked in Lido).

Like peers Uniswap and SushiSwap, Curve is governed by its own native token, CRV. However, where the protocol differentiates itself from the former two is through its token model. To participate in governance and to attain the full benefits of holding CRV, Curve holders are required to lock their tokens. Each holder can determine how long they’d wish to lock, which could be as short as one week or as long as four years, with governance power proportional to the length of time they choose.

Lockers are issued veCRV (vote-escrowed CRV) which represents a non-transferrable claim on CRV, meaning their holdings are illiquid for the locking period.

Although holders are giving up liquidity, they are being compensated for this risk by being awarded special privileges within the protocol, as veCRV holders are entitled to a share of the fees generated from swaps made on Curve, boosted CRV emissions when providing liquidity, and as previously mentioned, governance rights.

This last perk is particularly important as emissions to Curve pools (known as gauges) are determined through a veCRV holder vote.

As seen by the “Curve Wars” control over emissions can incredibly be valuable to protocols like stablecoin issuers, as it determines the yields, and therefore liquidity (and peg stability in the case of stablecoin protocols), of a given pool.

The Benefits of This Model

Now that we have a high-level understanding of the ve-model through Curve, let’s dive into some of the reasons as to why this model can be beneficial for protocols.

1. Encouraging Long Term Oriented Decision Making

A primary benefit of the ve-model is that it incentivizes long-term-oriented decision-making. This is because by locking their tokens for a certain period of time (typically 1 - 4 years), a holder is making a long-term commitment to the protocol.

In doing so, this provides them with an incentive to make decisions that are in the long-term, best interests of the protocol, rather than in their own immediate, short-term interest.

In a space as fast-moving and fomo-inducing as DeFi, the ability to foster a holder base that is long-term oriented is incredibly valuable. Given the level of noise and the pressure during a bull market to increase the price of the token by any means necessary, creating an environment in which a community can resist these temptations can help a protocol make clear, rational decisions that put them on a more sustained path to success.

2. Greater Incentive Alignment Across Protocol Participants

A second way in which the ve-model has proven to be beneficial is that it can align incentives across a wide swath of protocol participants and stakeholders.

Let’s explore this idea by again using Curve as an example.

Curve is like other DEXs in that it uses third-party providers as its source of liquidity. Like its competitors with active liquidity mining programs, Curve LPs face indirect exposure to the CRV token, as CRV emissions make a portion of the yield for each pool.

However, where Curve differentiates itself, and where the ve-model shines, is that Curve LPs are incentivized to hold their CRV tokens, rather than sell them into the open market. That’s because, as previously mentioned, if Curve LPs lock their CRV, they’ll receive a boosted CRV yield that is up to 2.5x greater than LPs who do not lock.

Although this mechanism is reflexive, as LPs are essentially locking a token to earn more of that same token, it serves a valuable role in that it has the potential to place a greater amount of CRV in the hands of liquidity providers than if the boost were not to exist. In doing so, it helps to align incentives between tokenholders and liquidity providers by increasing the overlap between the two groups.

This incentive alignment between a protocol’s users and its tokenholders can be incredibly valuable because the two groups often have competing interests.

For instance, in the case of a DEX, both liquidity providers and tokenholders generate income by taking a share of the same swap fee. This can create conflict within a DEXs community, as they risk losing liquidity, and damaging the quality of their product, by redirecting a portion of said fees to tokenholders.

In not directing fees back to their native token, a project runs the risk of upsetting and disengaging their core supporters who want to see a direct benefit in their project’s success. Given the intense competition within DeFi, it’s incredibly unlikely that any DEX can raise prices by increasing the fee they charge traders, meaning that these two stakeholders are competing for a slice of an ever-decreasing pie.

3. Improved Supply & Demand Dynamics

A final reason as to why the ve-model is powerful is through improving the supply and demand dynamics of a project’s token, i.e. helping number go up.

While it can be dangerous to a community’s long-term health to place too much of an emphasis on token price, a token is a gateway into the community. Buying a token is how people participate, support, and share in the upside of a project. Because of this, to attract and retain talented, value-add community members, it’s important for a protocol to have sound, or at least “non-down only,” tokenomics.

As previously discussed, the first iteration of DeFi tokens, the “valuelesss governance token” model, creates perpetual sell pressure with no underlying demand to help stem the downward tide.

Although ve-tokens, as seen from their current performance, are not immune from market weakness, they still help to do something to address both the supply and demand problem. It provides an economically-sound foundation for these protocol tokens.

For supply, vote-locking serves as a mechanism to remove tokens from the open market. This helps to offset the high emissions that some protocol’s produce, and we’ve seen existing ve-tokens be locked at very high rates.

As seen above, between the three largest ve-tokens by market cap, CRV, CVX, and FXS, on average 54.1% of these tokens circulating supplies are vote-locked.

Although reflexive to an extent, the ve-model has also shown to generate demand for the underlying token. Due to the utility necessary for vote-locking to provide holders to compensate them for the risk of their illiquidity, whether it be cash flow from fees or bribes, increased yields, discounts, or governance rights, ve-tokens have managed to create some demand for their underlying token in that these are valuable rights that holders want.

As discussed earlier in the piece, this has also been the driving force behind the Curve Wars.

A rabbit hole that extends far beyond the scope of this article, the Curve Wars have been fueled by the demand among DAOs to control that governance rights that can only be utilized with vote-locking. This not only creates demand CRV and CVX, but entrenches DAOs as longer term stakeholders within the protocol.

But veTokens aren’t a panacea. They have drawbacks.

Drawbacks to veTokens

While protocols may implement the veToken model hoping to instill perpetual “numba go up”, there are things worth considering.

1. Lack of Liquidity

Although removing liquidity from tokenholders provides an incentive for them to make long-term-oriented decisions, it can also pose challenges for a protocol.

For example, it runs the risk of concentrating ownership in apathetic stakeholders.

Were a locker to lose faith in the direction of the protocol, something that is not impossible given the fast-moving, and oftentimes years-long potential lock periods, they would have no way to exit their investment. This could cause an incentive misalignment, as apathetic stakeholders would be able to wield governance power. This could lead to incentive misalignment, as said locker would be incentivized to make decisions centered around extracting as much value from the protocol as quickly as possible, rather than emphasizing long-term value maximization.

2. Vote-Selling (For Specific Protocols)

A second challenge posed by the ve-model is that of vote-selling, or bribes.

Bribes have exploded in popularity across DeFi, with platforms such as Votium and Hidden Hand (formerly Votemak) facilitating tens of millions in bribes from various protocols for the Curve, Convex and Tokemak ecosystems respectively.

Although they have proven useful in that they have provided a cheaper way for protocols to attract liquidity than through traditional emissions-based programs and increased the attractiveness of vote-locking by providing holders with a somewhat steady stream of cash flow, bribes have the potential to introduce new systemic risks for a protocol that undermine the long-term oriented incentives that come with vote-locking.

For instance, while less of an issue for Curve and Convex in that they merely direct the flow of liquidity and do not manage risk, bribes have the potential to destabilize protocols that do require active risk management to operate properly.

For example, were a monolithic lending market such as Compound to switch to a ve-model that enabled bribery, it would be possible for a project to buy their way into becoming collateral on the platform.

Given that money markets are only as safe as their weakest collateral, this could lead to a scenario in which an exotic, or dangerously illiquid token becomes listed, increasing the chance of an insolvency event and undermining the protocol’s safety, stability, as well as trust among users.

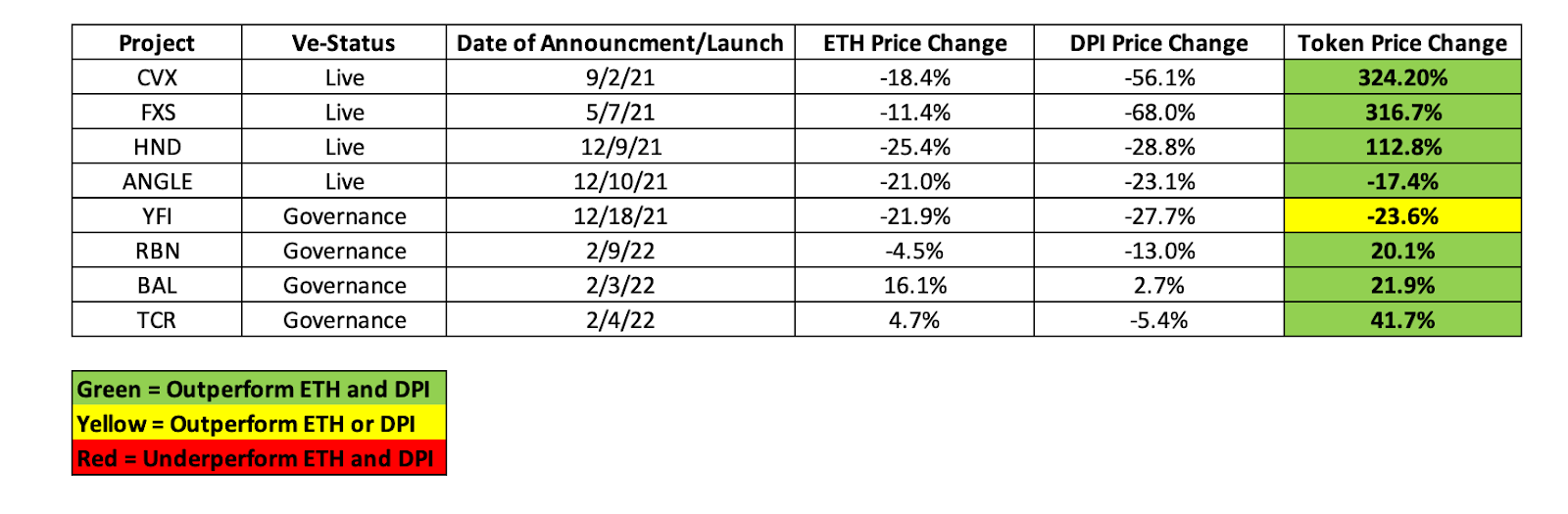

Price Performance Among ve-tokens

While it’s one thing to examine the theory behind the ve-model, it’s another to see whether it results in outperformance for tokens that are, or or are planning to, utilize a ve-model.

In the table below we measure the price performance of each token since either the launch date of the implementation of their ve-token, or the date of a public announcement stating their intentions to switch to the model. We also measure the price performance of two benchmarks, ETH and DPI, during that same period.

As we can see, seven of the eight tokens have outperformed both ETH and DPI since their launch or announcement date. Although this data may be skewed in some respects, as many of the launch announcements have come in recent weeks, and it’s easier to outperform a benchmark in over shorter time frames, it does suggest that there is validation for the ve-model among the market and investors.

The Future of ve-tokenomics

The ve-token model has emerged as a popular alternative among DAOs to the valueless governance token regime by encouraging long-term-oriented decision making, aligning incentives across protocol stakeholders, and creating more favorable the supply and demand dynamics for price appreciation.

Despite coming with clear tradeoffs which we’ve yet to see the full extent of, such as illiquidity and vote-selling, the ve-model feels like a step in the right direction for DeFi token design.

We’re also continuing to see attempts to improve the model, such as with Andre Cronje’s ve(3,3) Solidly exchange on Fantom, which utilizes an iteration on ve-tokenomics that includes elements similar to Olympus DAOs staking and rebasing mechanisms.

While we’ve yet to see how ve(3,3) will play out, it’s highly encouraging to see some of the spaces brightest minds tinkering with these tokenomics ideas.

Yes—DeFi tokenomics have stunk. But while ve-tokenomics are no silver bullet, it seems to be a step in the right direction for DeFi protocols.

Action steps

🔎 Explore veToken models from CRV, CVX, and others

⬆️ Level up on the Curve Wars