Why the Flippening Is Good for Crypto

Dear Bankless Nation,

The Merge was successful as of 12 hours ago. 🐼

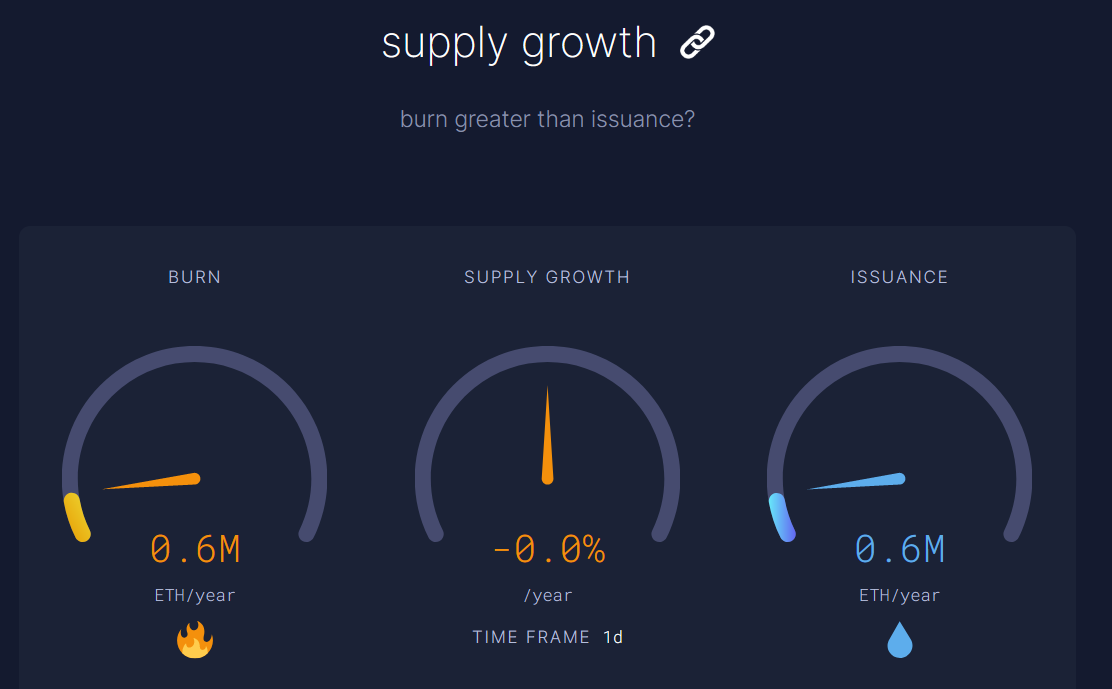

With it, the dynamics of Ethereum’s tokenomics have drastically changed.

Ethereum is issuing a lot less ETH to block validators now.

This drop in ETH supply growth has huge implications.

Ethereum is generating far more revenue and capable of being profitable, vastly improving its competitive standing against the grandaddy asset of the group: Bitcoin.

Could this mean the flippening is coming?

And could it be good for crypto?

Ryan Berckmans makes the case today.

- Bankless team

THOUGHT THURSDAYS

Author: Ryan Berckmans, Ethereum Investor & Community Member

The flippening is the idea that ETH’s market cap will eventually surpass BTC’s market cap.

Of course, ETH people like myself want the flippening to happen. We have bags.

But beyond our own personal financial interest, would the flippening be good for crypto?

What’s wrong with BTC being #1?

Hasn’t this gone fairly well so far?

If the flippening might be good for crypto, why hasn’t it happened already?

These questions are all intertwined and perhaps best examined by diving into the details of how BTC returns work.

Being reliable is not the same as being investable

BTC is the most credibly neutral asset. It’s because the Bitcoin protocol is mature, not expected to change, and proof-of-work is materially de-risked due to its simplicity and proven track record.

It has withstood dozens of failed attempts over the years by organized groups to unilaterally modify Bitcoin’s underlying code and increase its node sizes. Regardless of what Satoshi’s original intentions were, BTC’s reliability has become its core intrinsic value proposition.

Yet, Bitcoin’s reliability doesn’t mean the asset will hold its value or accrue value in purchasing power or fiat terms. On the contrary, Bitcoin’s core design isn’t programmable, has any value accrual to holders, and its mining cost structure causes significant value leaks.

That’s why for Bitcoin, being reliable isn’t the same as being investable.

With this context out of the way, let’s get into how BTC works, starting with a look at historical returns.

What happened around 2016?

From 2013 to 2016, BTC returned ~6x if you bought low and sold high. But, if you bought BTC at 2013 highs and sold in 2016, you made nothing. Zilch.

After 2016, it’s a totally different story: If you bought BTC in 2016 and held until today, you made 20x to 40x.

How about buying BTC at 2016 lows and selling into 2021 ATHs? You did 130x. Not bad.

"But bro", one might protest, "pre-2016 was, like, the crypto dark ages. That’s not relevant. We were just getting started."

Are you sure that sums it up?

What happened around 2016 that caused BTC to do much better in the years since?

How did Bitcoin change before or around 2016 that created vastly superior returns?

Bitcoin itself hasn’t changed. After all, not changing is Bitcoin’s thing, and part of its best-in-class reliability. Sure, the Lightning Network launched after 2016, but it’s hardly popular.

What else might have happened around 2016 to unlock the potential of Bitcoin? Perhaps the world was sleeping on Bitcoin and then woke up for some reason?

Or maybe some intangible element of BTC was baking in the oven, and that milestone finished around 2016?

None of these explanations are plausible. The idea that Bitcoin somehow evolved or unlocked its potential around 2016 isn’t explained at all by the narratives and numbers we’ve seen these past years.

Bitcoin rode on the coattails of web3

So what is going on here?

In my view, the simplest truth that best aligns with historical narratives and data is that since 2016, every major catalyst in the crypto markets has been driven by the promise or realization of web3 apps, which Bitcoin doesn’t support.

In 2016, a little project named Ethereum began having serious success in its effort to make public blockchains exponentially more useful as a computer instead of just an abacus.

The truth is that for approximately the latter half of its life so far, BTC has merely been surfing on the titanic wave of Actually Useful Stuff created by the Ethereum community (along with a few other communities).

At this point, the Bitcoin Maxi or Crypto Basket Investor might reasonably be expected to respond, "Wait, why would investors buy BTC if it's just a sideshow? BTC dominance is ~38% today. Are you kidding? You think ~$400B in market cap is just a mistake?"

Yes, that's exactly what I'm saying and will work to demonstrate below.

This is the story of why BTC is unsustainable as an investment, why the flippening is guaranteed, and thus, why the flippening is good for crypto— because it will remove an uninvestable asset as our industry leader.

His immaculate unsustainability

Bitcoin fits the definition of being an unsustainable investment quite literally. If we earnestly study Bitcoin’s use of proof-of-work, it’s difficult to dispute that Bitcoin is sustainable in terms of value retention or accrual.

Bitcoin’s fees are paid directly to miners, offering no value accrual to BTC holders.

This makes BTC permanently unprofitable, especially given the expensive cost structure of mining.

😰 Note that Bitcoin’s total fees may be too low to support a sustainable security budget, making the 21M BTC supply cap potentially a security issue, but that’s another story entirely.

BTC’s annual inflation until the 2024 halvening is ~2%.

Nominally, that sounds good, right? What’s wrong with a mere 2% inflation?

The problem is that inflation (issuance) in proof-of-work is a direct capital drain on BTC’s valuation because of the economics of mining.

This, when combined with the thin liquidity at the spot price, means that miners dumping BTC hurts the market cap of BTC a lot. Let’s unpack that…

On average and over the medium term, miners must dump most of the BTC they earn because they're willing and able to spend up to $1 in hardware plus energy costs to compete for $1 in BTC.

This is a huge problem for BTC (and also was for ETH before yesterday’s Merge!) because dumping X% of supply hurts market cap way more than X%.

By some estimates, dumping $1 of BTC might hurt market cap by $5 to $20.

The open secret in crypto is that you can't sell more than a sliver of total supply at the spot price. Order books are thin. Liquidity is thin. HODL, bro. And so, if not even close to everyone can sell at today's price, miners are, by definition, consuming a scarce resource by continuously dumping.

That's to say, BTC miners may dump a mere ~2% of total supply per year, but they capture way more than 2% of net fiat inflows per year. And since BTC’s fees will always be low and paid to miners anyway (contributing to dumping), the sum of these facts has two very important implications that might possibly be lost on many BTC holders:

- On average, somebody must buy a great deal of BTC every day to keep the price flat. In 2021, about $46M per day in net fiat inflows was needed to keep BTC flat. In other words, "I have this great investment for you, we just need $46M in other people’s new money every day to avoid losing our principal..."

- When a BTC investor makes 50% returns, or 5x, or 40x, these profits can only come from new entrants. There's no meaningful fee revenue accruing to holders and no meaningful apps on Bitcoin, and the price of BTC can't keep itself flat due to the cost of mining, so, by definition, anyone who buys BTC at ATHs can’t make money on a sustainable basis. There is no hope of returning 0% on average.

The social disequilibrium

Who willfully buys an unsustainable investment for the long term? Who recommends buying it? How did we end up in a situation where, last year, BTC rode ~40% dominance to a total crypto market cap of $3 trillion?

In short— and crypto boomers like me seem to love this reference— nobody got fired for buying IBM.

As far as I can tell, a handful of different kinds of buyers may be responsible for driving capital into BTC, each for their own reasons, and most unaware of the true risk profile of their investment.

- First, new entrants buy BTC. These are, for example, veteran hedgies moving over to web3, long-running institutional investors, ultra high net worth individuals, and retail plebs. These new entrants show up in web3— statistically speaking, during a bull run— they're all excited, they know crypto is novel and complex af, they see we're on a long-term journey to the moon, and they reasonably allocate pro rata into a basket of top crypto assets. Pro rata is an investment term that, in this context, means "No f*ckin' clue so I'm gonna buy everything in proportion with today's market caps." These new entrants are often future lambs to the slaughter of BTC’s unsustainability as an investment.

- Second, long-term basket allocators buy BTC. These may be crypto OGs who have enjoyed being early and are chilling, or crypto VCs with more connections and capital than, say, willingness to cultivate independent investment theses. These folks buy BTC because they genuinely don’t have and/or don’t want to build confidence in where the space is headed, and they wish to avoid getting caught on the wrong side of what they see as a risky thesis. More perniciously, these long-term basket allocators are often authority figures, and they play a significant role in helping to drive new entrants towards BTC.

- Third, reflexive wolves buy BTC. But they may sell it all next ATH, too. These are often the brightest, shrewdest, and/or hungriest of the crypto OGs, VCs, and finance people that pivoted into web3. Reflexive wolves are typically well aware that BTC is not the best performing investment. Yet, they feel that for the Greater Good (i.e., often their good), “we” must avoid rocking the boat and instead work to promote Bitcoin. Reflexive wolves feel that if BTC were to collapse, it’d mean huge losses for some of crypto’s largest and most powerful investors, which may hurt the whole space and their portfolios. And so reflexive wolves kick the can down the road. Some may dispute that they exist at all, or consider them to be mere traders. But I’ve met a few hardened ones.

- Fourth, traders buy BTC and rotate profits into BTC as crypto's de facto reserve currency. Traders are just going with the flow. Literally. They know that during this current era, BTC does better in bad times and worse in good times. Traders' time horizons are extremely short, and they're just riding BTC as a home base for riskier plays. In a way, traders are among the most rational and/or least destructive of all BTC buyers.

- Fifth, BTC truebloods buy BTC. These are hardcore Bitcoin people that genuinely believe that BTC is something approximating the most reliable money in the history of the world. They believe not just that BTC has best-in-class reliability, but also that this reliability will necessarily translate into being an excellent long-term investment and/or by far the best crypto investment on a risk-adjusted basis.

Here's the thing— among these five kinds of BTC buyers, only the truebloods have a hope of most of them sticking around after BTC dominance implodes. Collectively, Bitcoin buyers are playing one of the biggest reflexive games of chicken in modern finance. Among them, only the reflexive wolves have even a slight conception of the nature of this game.

Granted this breakdown of the kinds of BTC buyers is overly simplistic, but I think it’s useful.

Having read this far, BTC maxis and flippening skeptics may have grown in confidence:

"Lol. Ok. Water is wet, the sun rose this morning, and this smooth-brained ETH maxi says we're all wrong and BTC is doomed as an investment vehicle.

So, buddy, why hasn't the flippening already happened?"

Let me explain: numbers, that's why.

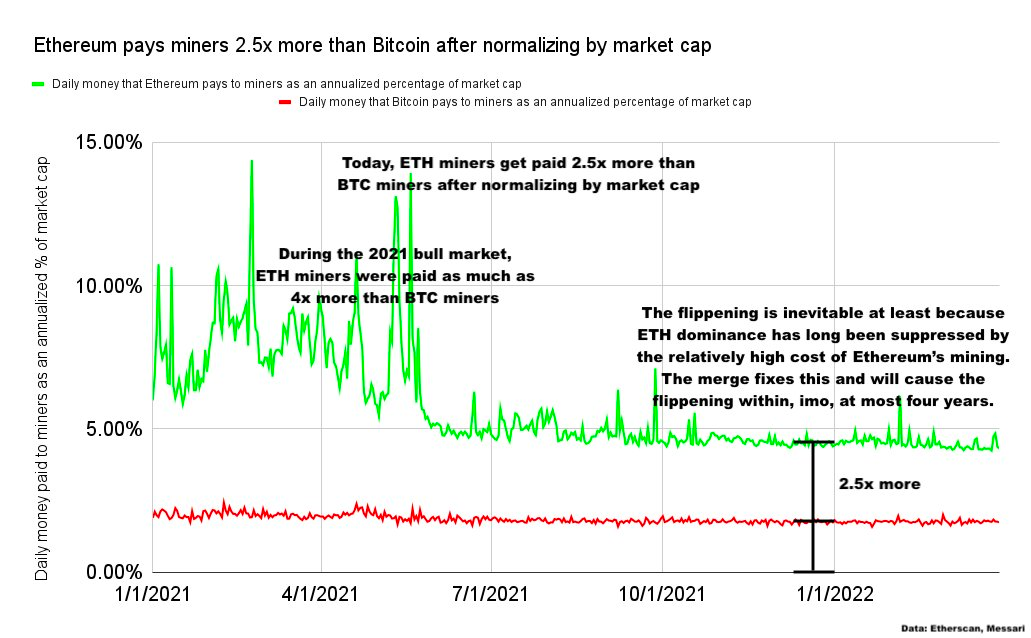

Historically, ETH miners were paid a lot more than Bitcoin miners. If the two chains swapped cost structures, i.e. if BTC miners had made what ETH miners made and vice versa, or if the Merge had been ready two years ago, I think the flippening may already be behind us.

Let’s explore the numbers…

On the encumbered shoulders of giants

If miner dumping matters a lot— and it does, as explained above— then it also matters a lot that ETH miners were paid 2.5x to 4x+ more (after normalizing by market cap) than BTC miners over the past few years:

Last year, BTC miners were paid $16.6B, while ETH miners were paid $18.4B.

If instead, last year, we were to swap Bitcoin and Ethereum's cost structures, then ETH miners would have earned and dumped ~$6B while BTC miners would have earned and dumped ~$50B.

This is a crucial point, so let me make it again: last year, Ethereum miners earned and dumped $1.8B more in ETH than Bitcoin miners dumped in BTC. If we imagine reversing the cost structures between the two chains, BTC miners would have earned and dumped ~$44B ($50B - $6B) more BTC than Ethereum miners dumped ETH in 2021 alone.

To drive this point home: in 2021, Ethereum was so expensive to run vs. Bitcoin that if the situation had been reversed, Bitcoin would have required an additional ~$45.8B in net fiat inflows (i.e. new buyers of BTC) for the two chains’ market caps to remain the same as they actually are today, all other things equal.

We arrive at ~$45.8B by going from the actual ~$1.8B in Bitcoin’s favor to the hypothetical of ~$44B in Ethereum’s favor.

These extremely large numbers — specifically how ETH has had A LOT more sell pressure from miners relative to its market cap— is a key driver for why flippening hasn't happened yet.

The emperor that wasn't

What's going to happen next?

Ethereum has eliminated miner dumping with the shift to proof-of-stake as of the Merge.

We're now on a path to profitability, scaling with Layer 2s, and web3 is growing to global ubiquity.

Ethereum has become a positive-sum, productive economy.

In the years to come, for the above reasons, I think it's 99% guaranteed that ETH flips BTC. The 1% is unknown unknowns. Tail risk. Like if aliens were to show up and force us to use BTC as the only global currency.

ETH's profitability, low cost from validating, great growth from dapps, and good vibes from benevolent credible neutrality are on track to carry our industry through the flippening and into a post-BTC era.

The Fall of Rome

The day of the flippening will be explosive and spectacular.

Sure, we may unflippen for a short while. But on a medium-term time horizon, this is a one-way transition for BTC into the wastebasket of crypto investment antiquity.

Unfortunately, many well-meaning crypto and web3 investors are likely going to lose a lot of money during BTC's slow decline and violent collapse.

In short, Bitcoin's current ~40% dominance seems almost surely to be highly reflexive and circumstantial in ETH's pre-PoS cost structure as well as, to a lesser extent, Ethereum's scaling challenges before our L2 ecosystem really began firing on all cylinders this year.

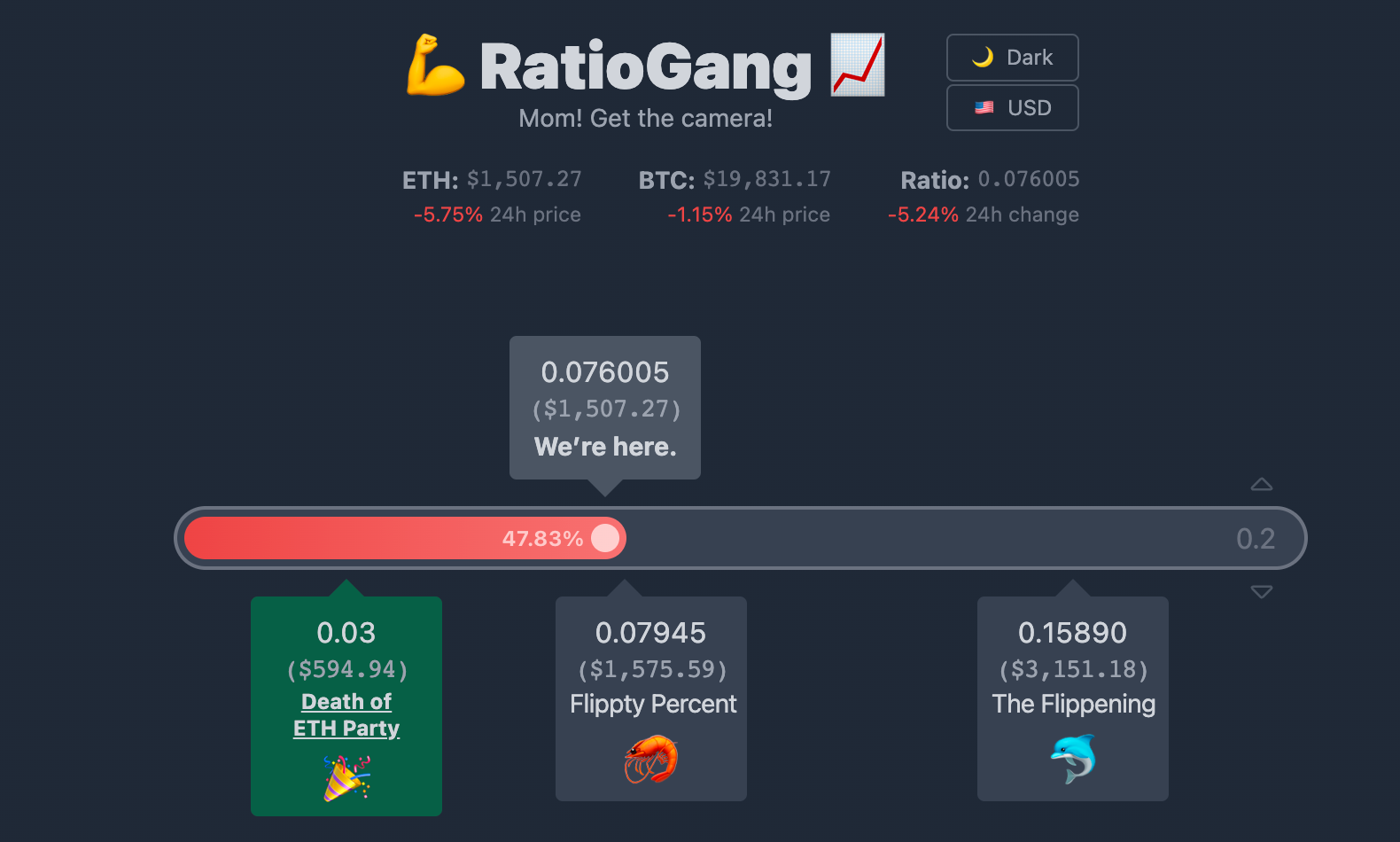

Today, the flippening ratio is just shy of 50%.

As ETH slowly gains on BTC, we'll hit a breaking point where the writing on the wall becomes common knowledge, and then, the flippening ratio will jump in a single day from 70% to 100%, or 80% to 120%, or whatever it ends up being. Farewell to the era of BTC.

Why the flippening is good for crypto: the healthy new era

I suspect that eventually, years from now, all of us, including the majority of today’s BTC owners, will look back and see how intellectually bankrupt of an idea it was that BTC could ever remain #1.

In summary:

- BTC is a naturally unsustainable investment and, with no application layer and significant revenue prospects, always will be.

- BTC’s mining will never be ESG-friendly, even if a large proportion of mining becomes truly green.

- BTC hoovers up capital, attention, and especially monetary premium that could instead go into Ethereum & other ecosystems that are more directly and proactively improving the world.

The flippening is programmed because BTC not only fails to accrue value, it leaks value. And the flippening is good for crypto because having an uninvestable, value-dilutive asset as the industry leader is unstable and unhealthy, and we need web3’s investment landscape to be stable and healthy.

My views on this flippening thesis haven’t changed in two years:

BTC’s destiny is to pass through the flippening and end up as a venerable, affable pet rock.

The original digital collectible. Maybe then I'll buy some for the trophy cabinet.

After the flippening, crypto's truly healthy era will have begun.

An era of ESG friendliness, lean cost structures, profits earned from valuable apps, web3 growing to global ubiquity, and Ethereum becoming a global settlement layer— a level playing field for all of humanity.

Action steps

- 📺 Watch today’s author Ryan Berckman on the podcast Is The Merge Priced In?

- 📚 Revisit Lucas Campbell’s The Flippening Is Inevitable

Author Bio

Ryan Berckmans, Ethereum Investor & Community Member