ETH: The World's Most Capital Efficient Asset

Dear Bankless Nation,

When Ethereum launched, there was nothing to do with ETH.

But then DeFi was born. MakerDAO launched in 2018 and allowed ETH holders to take out a loans using their ETH as collateral.

The more ETH you had, the more power you had.

Then Compound launched with lower collateralization ratios and liquidation penalties. Same thing—more ETH meant more power, more capital efficiency.

Then Uniswap launched and all liquidity was built using ETH pairs. Now you could provide liquidity and earn trading fees with ETH. More capital efficiency.

Today there’s thousands of ways to use ETH in DeFi applications—with more launching every day.

So what’s the throughline?

DeFi is a global competition to make ETH the most useful asset in the world.

David explains.

- RSA

ETH: The World's Most Capital Efficient Asset

The March for Capital Efficiency

If you haven’t heard, Ether is ultra sound money.

Ethereum 2.0 isn’t just a scalability upgrade to the Ethereum network, but it’s also an economic upgrade to Ether—the money that powers and protects the Ethereum economy

The combination of Proof of Stake, a consensus mechanism that minimizes the need to issue ETH, and EIP1559, a mechanism that burns ETH as a function of the magnitude of the Ethereum economy, turns ETH into a monetary unit with what can only be described as having ‘Sci-Fi’ economic fundamentals behind the currency unit. Ethereum 2.0 is the protocol upgrade that makes ETH “ultra sound money”.

But this article is not about ETH as ultra sound money.

Instead, this article is about how DeFi is a crucible of competition for capital efficiency, and how ETH is the asset that benefits the most from this competition.

DeFi’s is on a relentless march towards capital efficiency.

Every new protocol that finds success, finds it because it was more capital efficient than its competition. Every protocol upgrade that any DeFi application has gone through has been in an effort to become more capital efficient. in DeFi, capital efficiency is the name of the game.

Ether, as the native asset to Ethereum, and therefore DeFi, is the asset that receives all of the tailwinds of this competition. When DeFi becomes more capital efficient, Ether becomes a more efficient asset.

DeFi is on a march towards capital efficiency, and ETH will receive all of it.

In the Beginning…

At genesis, Ethereum was formless and empty; there was only ETH.

Distributed to 8893 different addresses in the genesis block in what can only be called as “Ethereum’s big bang”, ETH exploded into existence on July 30, 2015.

What to do?

What is Ethereum?

What is Ether?

What next?

Much like the internet, a small group of nerds could see that Ethereum was going to be big. But how Ethereum would actually impact the world was still just speculation.

What does it mean to have a singular world computer, accessible to everyone? What does it mean to have a native asset, ETH, that powers it?

The early days of Ethereum were filled with early concepts of what could be. We had no models of successful applications to use as examples, so early Ethereum builders emulated what was working in the Web2 world.

Peepeth was a version of Twitter, except built on Ethereum. The idea is that, with a censorship-resistant computer, we could build censorship-resistant Twitter, where no one could be de-platformed or silenced.

It seemed like a logical first step for Ethereum: Take the existing Web 2 applications, and put them on Ethereum! Of course! It was so simple!

It was theorized that Twitter users would migrate over to Peepeth to access the benefits of decentralization and censorship resistance! People would purchase ETH from Coinbase or Gemini, so that they could write Tweets to the Ethereum blockchain, and Ethereum’s decentralization would protect users from de-platforming!

“Yes, of course... this is how Ethereum will change the world….this is why we needed ETH!”.

These early ideas of what Ethereum was optimized for were wrong.

These thoughts of re-building Web2 apps on main-chain Ethereum were common in the early days of Ethereum. It makes virtually zero sense now. Gas fees back in the day were less than 1 gwei, while ETH was under $10… you could basically write a tweet to Ethereum for free.

What to do with your ETH?

Imagine you participated in the Ethereum presale and you are the owner of 1,000 ETH. How does an application like Peepeth (decentralized Twitter) benefit you? At the cost of 0.00001 ETH per tweet, you can tweet 100,000 tweets and still have 999.999 ETH leftover.

Peepeth didn’t solve the problem of how to effectively leverage the full balance of ETH you own.

Ethereum needed applications that leveraged the amount of ETH that ETH holders had. In the beginning, Ether was bored and was looking for things to do. As it turns out, applications that copied Web2 platforms were completely skeuomorphic and antithetical to the properties that public, permissionless crypto-economic optimize for: money and value.

Rather, the common denominator for applications that saw success was applications that used ETH as money. Applications that use ETH as money allowed users to use the full balance of the ETH they owned and made owning more ETH more useful.

Applications that make Ether more useful were more used by ETH holders, and created a virtuous cycle: Users that owned ETH could benefit from the Ethereum apps that let users leverage the balance of their ETH. Because there was a population of ETH holders that needed reasons to use their ETH, applications that used ETH as a capital asset received outsized adoption from the specific cohort of people that were interested in Ethereum survival and ETH value:

ETH holders.

And so Ethereum rejected ETH as simply “the asset that lets you use dApps”, and instead took its first step of a long march of making ETH the most capital efficient asset the world has ever seen.

DeFi isn’t De without ETH

Because it’s Ethereum’s native asset, ETH has a privileged position inside Ethereum’s economy.

- It is the only asset on Ethereum that wasn’t issued by a smart-contract, and therefore has no smart-contract risk.

- It’s native to the Ethereum protocol, so it has no counter-party risk.

- It has assurances towards its scarcity, because any monetary policy failure is a risk to the Ethereum network, not just the DeFi apps on top of it (aka, we’ll have bigger things to worry about).

ETH is the most trustless asset on Ethereum because every asset other than ETH has some compromise to its trustlessness.

Even highly decentralized assets like UNI, AAVE, and MKR have governance and contract risks associated with them. Governance could become corrupt… or just be bad… and destroy the value proposition of the asset.

But more importantly, DeFi tokens largely capture value by leveraging ETH’s properties of permissionless and trustlessnesss. Without ETH, what would DeFi apps capture value in?

All DeFi Roads Lead to ETH

DeFi tokens like UNI, AAVE, and MKR capture value from the surrounding Ethereum ecosystem. Each protocol captures fees using different mechanisms, but they all generally capture value by taking a fee on the economic activity that passes through their platform.

There are three main types of tokens that apps denominate their value-capture in:

- Other DeFi tokens (Compound captures UNI borrowing fees, for example)

- Stablecoins (USDC, USDT, DAI)

- ETH

But really, it boils down to capturing value in either centralized stablecoins or ETH.

If a protocol captures value by earning fees in other DeFi tokens, that’s just another intermediary step between capturing value in either stablecoins or ETH, because other DeFi protocols are also capturing value in either ETH or stablecoins…or other DeFi apps.

Capturing value by earning fees denominated in DeFi app tokens like UNI or COMP ultimately leads back to capturing fees in money, which is either ETH or stablecoins.

Additionally, any fees captured in DAI is just a hybrid of capturing value in other stablecoins and ETH, as DAI is a claim on MakerDAOs balance sheet, which is largely comprised of stablecoins and ETH.

Without ETH, DeFi apps would be forced to capture value in tokens that have centralization risk dependencies.

DeFi tokens, as capital assets with the potential to issue cash flows to token owners, need a trustless, decentralized asset to issue the captured value by. If Uniswap was only able to capture protocol feels in USDC or USDT, then this wouldn’t really be ‘DeFi’ would it?

Without ETH, Uniswap transferring value to UNI holders would be dependent on whether Circle or Tether allows it.

DeFi protocols need a trustless asset that is a fundamental part of the protocol, or else it’s reintroducing the centralization risks that we’ve been trying to avoid in the first place.

ETH is unencumbered from centralization risk and therefore is a favorable asset to capture value in.

Each asset comes with its own risk parameters (volatility, liquidity, centralization risks, bugs & exploits, etc), and each DeFi app that runs on collateral (spoiler; they all run on collateral) sets different parameters for each asset, according to what the protocol feels is safe.

No asset is perfectly optimized for all risk parameters; all assets have risk. But Ether, as the native asset to Ethereum, fills a privileged position in DeFi as the only asset with all counter-party and contract-risk eliminated. It is the single asset on Ethereum with the strongest settlement assurances, and therefore the least settlement risk.

All roads on Ethereum lead to ETH.

The March Towards Capital Efficiency

Every DeFi app that has seen success has been one that uses ETH as capital. Each successive application only sees success if it’s able to leverage the capital stored in ETH more efficiently than its competition.

Starting in December 2017, ETH had a collateralization ratio of 150%, variable interest rates, and a 13% liquidation fee (via Maker). Now it has progressed to 110% collateralization ratio, 0% interest fee, and competitive collateral liquidation auctions.

And DeFi is just 3 years old.

The March of 2018-2019

MakerDAO: The Birth of DeFi

MakerDAO launched in December 2017, at the height of the ICO mania. MakerDAO was the first application on Ethereum that allowed users to leverage the full balance of their ETH.

The more ETH you have, the more you could do with MakerDAO. More ETH meant you could mint more DAI, or have larger collateral buffering your DAI loan. More ETH was more power. MakerDAO allowed ETH to be used as capital.

And DeFi was born. DeFi is defined as applications that take deposits of trustless capital assets (ETH) and allows you to do things.

Compound: ETH as Collateral

Compound V1 launched September 26, 2018. Similar to Maker, Compound allowed for ETH to be deposited into its application in order to borrow against the value of the deposits.

Meaningfully different from Maker, Compound allowed for the depositing of many assets, and also the borrowing of many assets. Also different from Maker, instead of the 150% over-collateralization ratio and 13% liquidation penalty, Compound allowed for a lower 133% collateralization ratio and 8% liquidation fee.

Seven months after the launch of MakerDAO, ETH received its first major upgrade in capital efficiency. Compound became very competitive with Maker as an attractive place to deposit your ETH, in order to leverage the value of the capital.

Uniswap: ETH as the trading pair

In November of 2018, Uniswap V1 was launched.

Uniswap used ETH as the trading pair for every single token on its exchange. Every token received liquidity by being paired with ETH. Uniswap’s main innovation was allowing ERC20 tokens on Ethereum to tap into the liquidity of ETH as an asset, in order to bestow ETH’s liquidity upon the token.

Simultaneously, Uniswap also gave ETH a diverse number of options for capturing value, as each Uniswap market allowed ETH to capture 50% of the fees of any given trading pair (the other token in the pair accounting for the other 50%).

Like MakerDAO, Uniswap allowed ETH holders to tap into the full balance of ETH that they held. The more ETH you had, the more power Uniswap gave you. The more ETH you had, the more fees you could earn. It gave ETH holders further optionality with how to leverage their capital, so long as their capital was ETH.

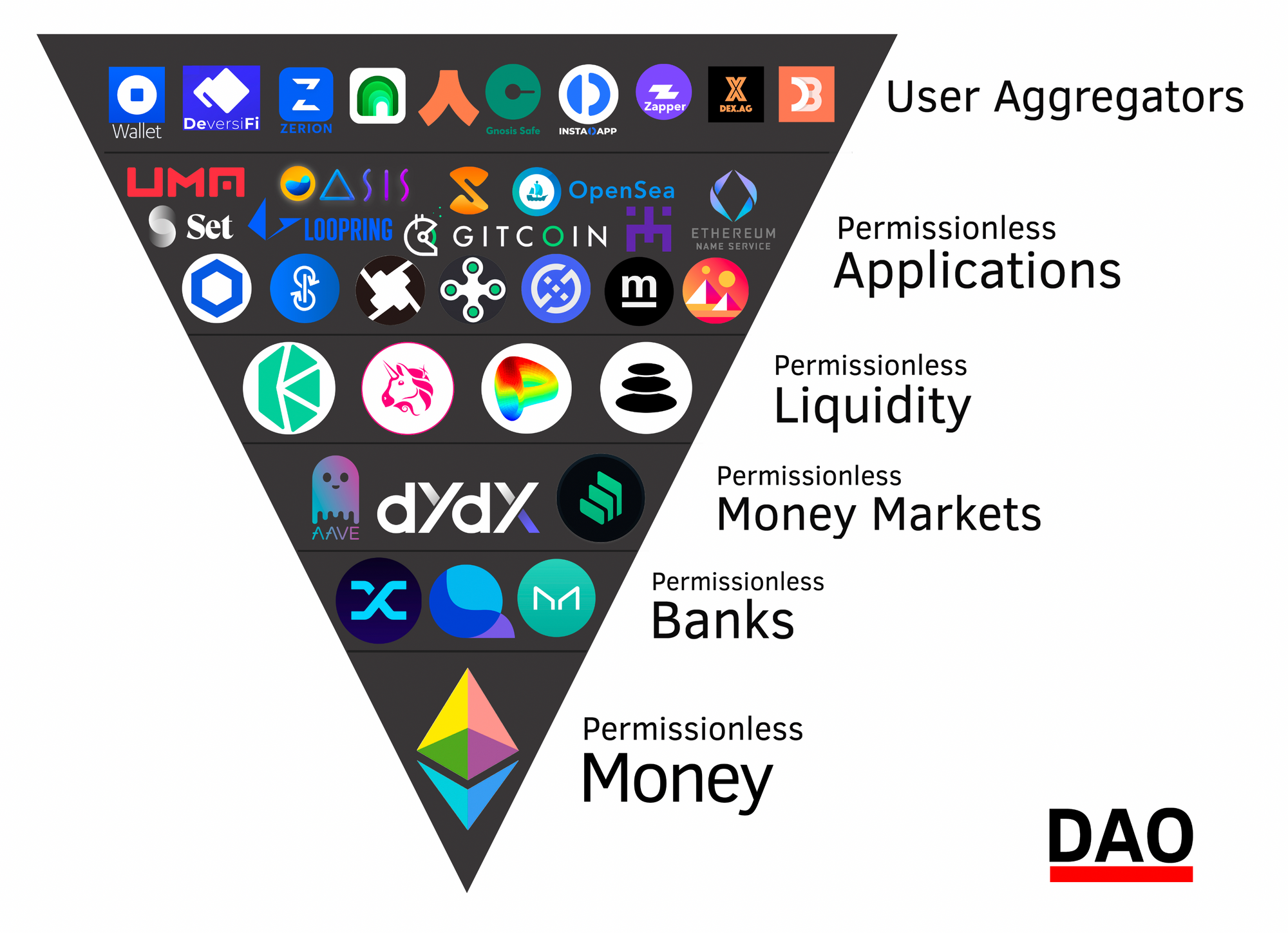

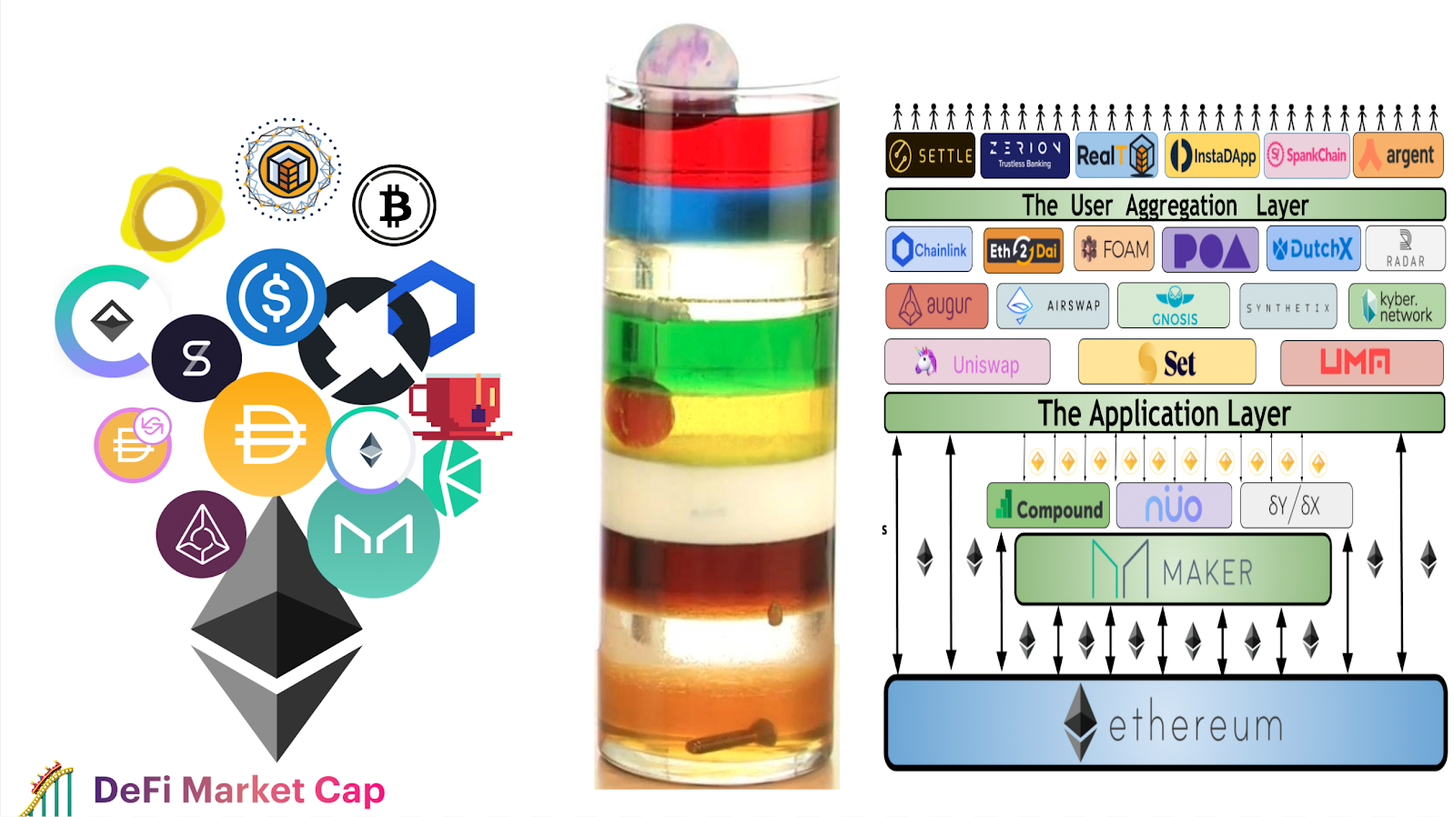

The Ethereum application layer is a crucible of competition for capital efficiency.

In November of 2019, I wrote Ethereum: The Money-Game Landscape, with the subtitle: Ethereum is a place to build things that compete for value. The tl;dr: of the piece is that Ethereum’s application layer is a diverse set of financial applications that are all trying to convince you to deposit your assets into them.

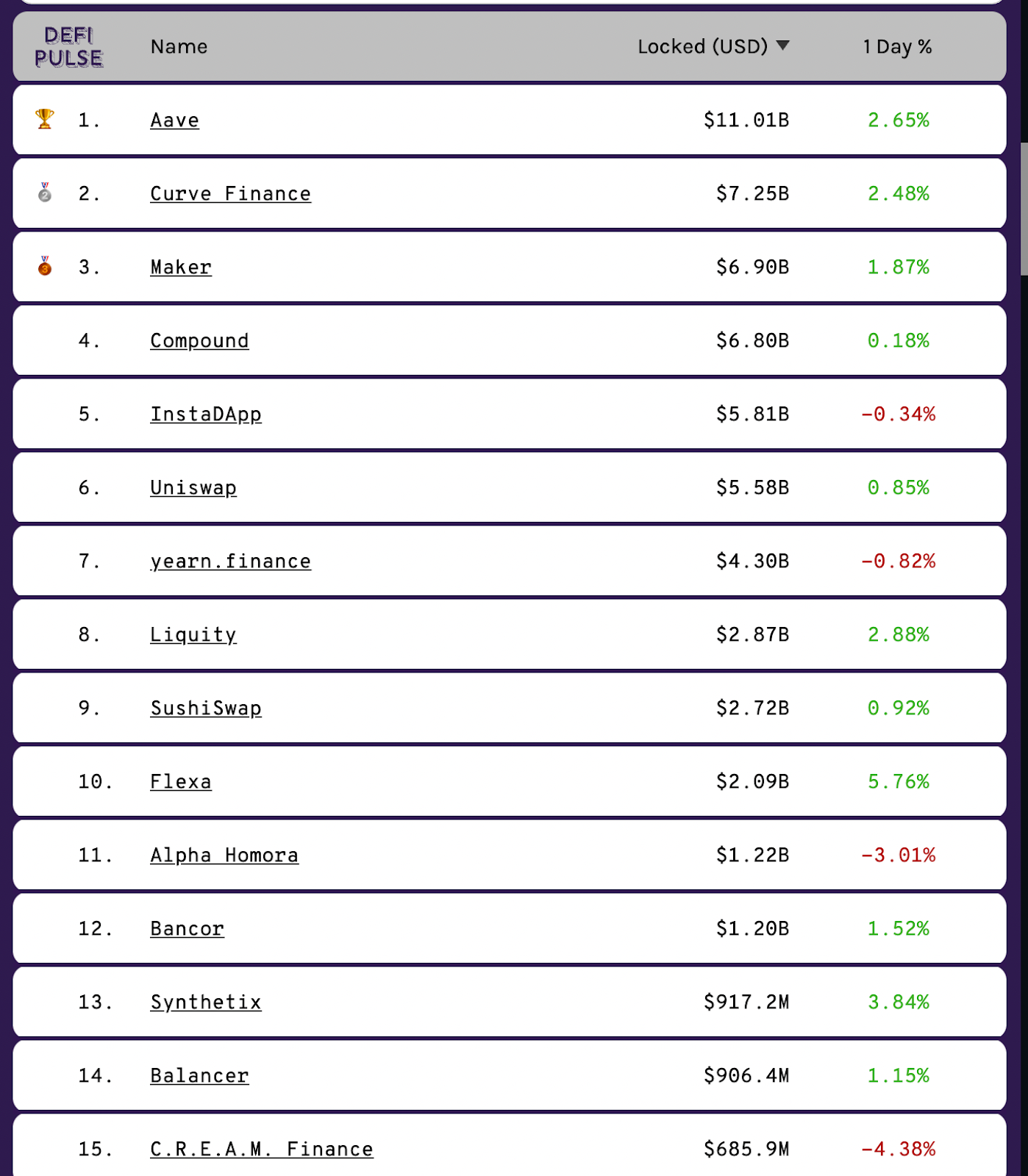

The reason we all go to DeFiPulse.com is because it’s the leaderboard for deposits. We go there to check the score of the big game!

The big game: Value locked.

Except $1 of ETH lockup is arguably worth more than $1 of crypto-dollar lockup because ETH is actually scarce, trustless, decentralized, and resistant to printing.

Good Collateral

Ethereum applications owe nothing to ETH. Ethereum applications are maximalists-of-themselves. Good Ethereum applications are always application-first. They do what’s best for themselves and the users. This is why Ethereum is so powerful: it’s an open platform that enables applications to become the best versions of themselves.

It just so happens that ETH is a fantastic collateral asset that basically every Ethereum application wants, for its own sake.

It just so happens that Decentralized Financial applications need maximally trustless collateral to function.

It just so happens that the more trustless and distributed an asset is, the better risk-parameters DeFi apps can offer the asset.

Lower fees, lower collateralization ratios… better👏capital👏efficiency👏👏👏

Good Collateral…but at the protocol level

Did I mention Ether is ultra-sound money.

The combination of EIP1559 and The Merge makes ETH the asset with the lowest possible issuance, and a burn rate that is a function of the volume inside the Ethereum economy.

While this reality doesn’t necessarily influence the parameters that DeFi apps bestow upon ETH, it does influence people’s disposition towards ETH as an asset. After all, money is a meme, and the best money is the one that has the best meme. Ultra Sound Money is a pretty damn good meme, and that statement is backed up by how, in reality, ETH is actually ultra sound money.

The monetization of ETH as an asset is one of the primary drivers to the increasingly favorable risk parameters bestowed upon ETH by both native DeFi apps and CeFi companies. The more liquidity, distribution, holders, and overall believers behind ETH as a monetary asset are all risk-reduction forces behind ETH that allow DeFi apps to do more with less.

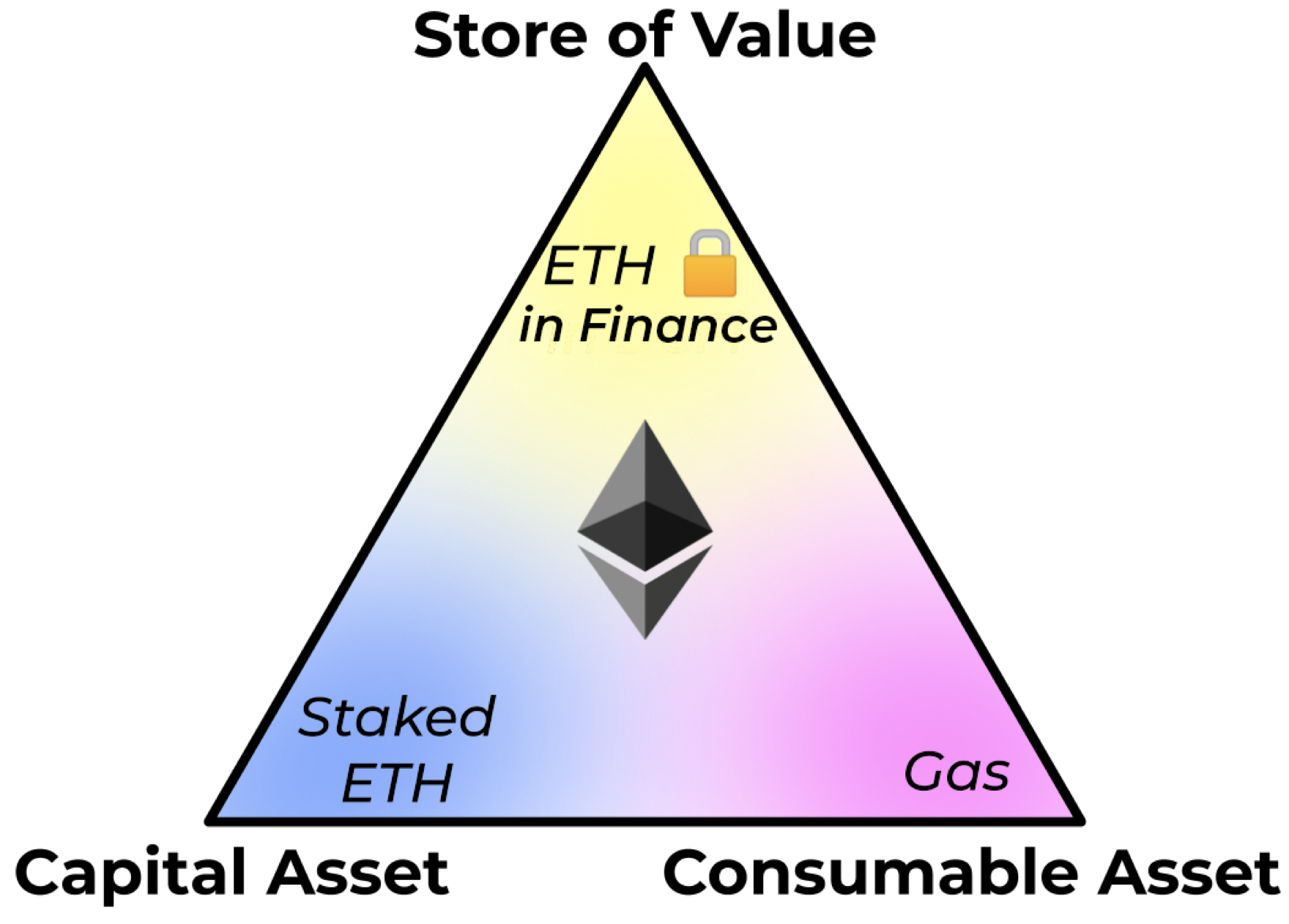

And, of course, one of the main drivers behind why people are putting so much conviction behind Ether is because it’s also a triple point asset. There are three compelling reasons to own ETH: it pays you dividends, it’s a store-of-value, and you need it to buy Ethereum block space from validators.

As a Schelling-point for money, ETH has the most surface area for convincing the most people of its money-ness.

But what’s missing from the Triple Point Asset thesis, and the Ultra Sound Money model, is how DeFi is a crucible of competition for capital efficiency, and it’s on a march to produce DeFi apps that allow ETH to become the most capital efficient asset of all time.

Not only is ETH ultra sound money, but DeFi is making ETH the most capital efficient asset in the world.

Next-Gen DeFi Apps: 2020 and Beyond

We’ve recently seen a new generation of DeFi applications that are all adding to the steep competition of capital efficiency for DeFi apps.

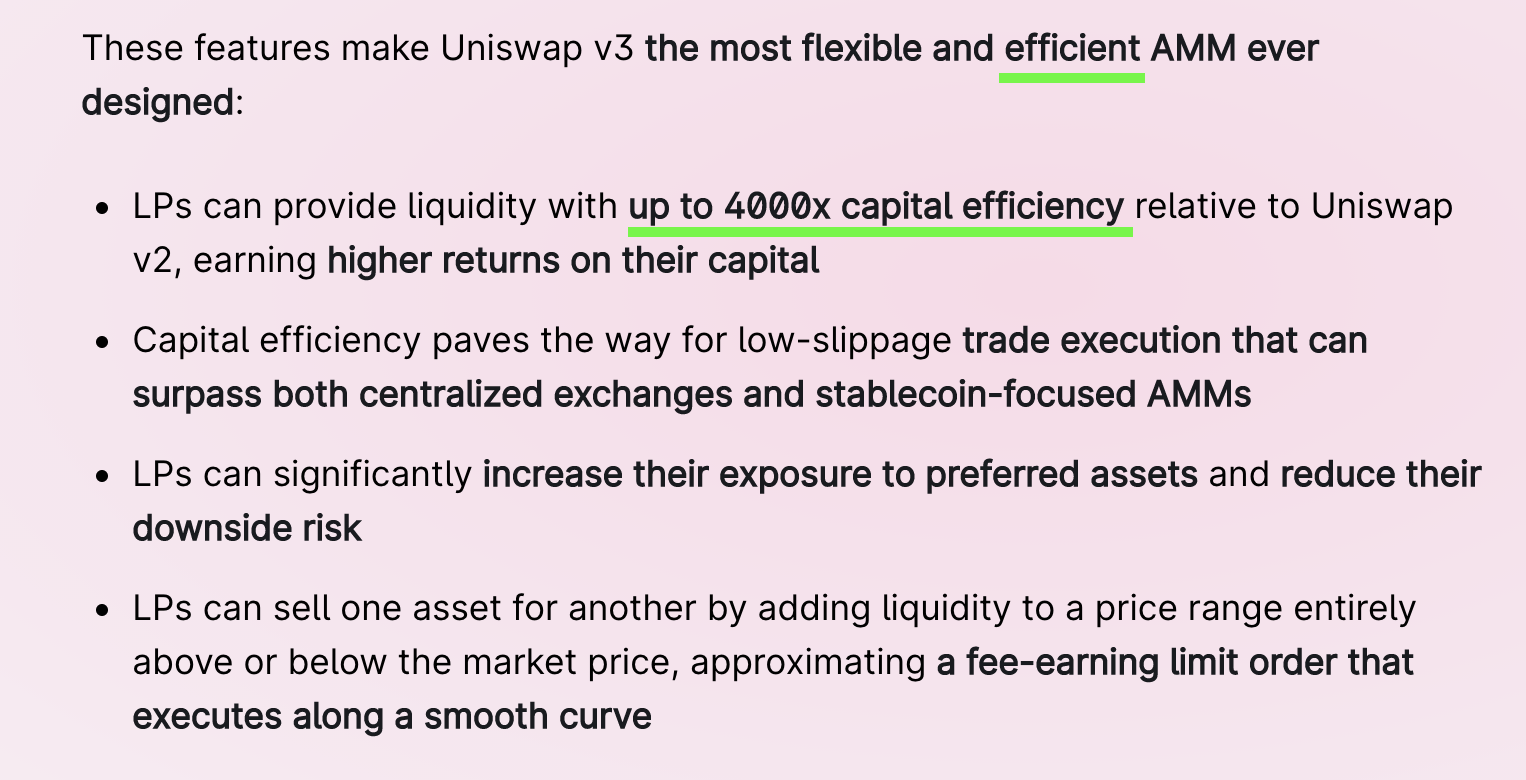

Uniswap V3

Uniswap V3’s capital efficiency boasts a 4,000x increase in capital efficiency for those who provide liquidity.

Balancer V2

Balancer V2 allows you to provide liquidity and lend out assets in Aave simultaneously.

Liquity

Liquity gives you a 0% interest rate and a 110% collateralization ratio on your ETH deposits. It could be argued that these are some of the best rates in DeFi, and answers why Liquity is already #8 in TVL at such a young age.

Also, the protocol is ETH-only.

Aave AMM Token Collateral

Aave allows you to borrow against your Uniswap and Balancer LP Tokens, allowing you to draw debt against an asset that spreads exposure across two different assets, while collecting exchange fees at the same time.

ETH: DeFi’s Best Multi-App Collateral

When two applications like Aave and Uniswap stack on top of each other, the risks of each application compound. Aave’s risks are now also Uniswap’s risks, and Uniswap’s risks are now Aaves. Additionally, other applications that impact Uniswap can also, therefore, impact Aave, and visa versa.

The surface area of risk grows exponentially.

DeFi black swan events have varying epicenters and magnitudes. Most hacks, bugs, or exploits only impact a local part of the overall body of DeFi. Fortunately, the holistic body of DeFi has never seen signs of any ill symptoms from any hack since the 2016 DAO hack; each incident is largely contained to the local environment around the hack.

DeFi application composability is the reason why we’re all here. It is the magical force that absorbs every bit of useful software into the overall DeFi structure and makes DeFi itself more and more useful over time. If it is useful, DeFi will integrate it.

Yet it is also it is our Achilles heel. DeFi composability is how cancer can come to affect the whole body. Complex bodies have complex interactions, and at some point, DeFi’s level of composability and self-integration will grow beyond our ability to reason about.

In order to control for that compounding risk and exponentially increasing complexity, ETH will likely be the asset that operates as multi-app collateral. Every single integration of DeFi apps into a new product or service needs to control for the risks they introduce when they add complexity and surface area into their product. These applications can control for this risk by focusing on low-risk collaterals in their app. As stated above, ETH is the only asset in DeFi with all counter-party and contract-risks eliminated. Any application that needs to find ways to reduce risks will naturally favor using ETH as collateral.

ETH LP Positions

Applications that already allow ETH and tokens as collateral will likely also allow LP positions of ETH + the same tokens they already use as collateral. In theory, there is little to no risk in allowing an LP position of ETH + an-already-approved-collateral-token as collateral for your app.

This could even be better risk management practice for borrowing/lending protocols like Aave and Compound, as the LP tokens increase in nominal value over time and offer diversification across two assets instead of one without any added risk, because they were already accepting both tokens as collateral anyways.

If ETH LP Positions become a favorable form of collateral for DeFi Apps, this benefits ETH in an outsized manner, as ETH is half of every LP position.

As DeFi Complexity Grows, ETH Utilization Will Follow

DeFi applications that have outsized composability risk will control it by focusing on the most risk-free asset on Ethereum. Therefore, ETH will discover outsized utilization from financial products that leverage high amounts of composability.

I would expect the amount of total composability (however you want to measure this) would only increase as DeFi matures and there are money total money legos available to chose from. As the measure of the magnitude of the total compatibility of DeFi increases, I would expect ETH utilization in DeFi would also increase commensurately.

As the DeFi structure grows larger, ETH will be the asset that holds it together.

Where is this going?

All roads on Ethereum lead to Ether.

In addition to the ultra sound properties of ETH found at the protocol level, DeFi is in relentless competition to make ETH the most capital-efficient asset possible. These applications need to win this competition to stay relevant. As we know, competition is good for the consumer… and the way it becomes good for the consumer is by making the assets they hold more capital efficient.

Every asset is different, and each one captures these positive externalities of DeFi’s competition in varying amounts. The measure of how well different assets on Ethereum are capable of capturing these capital efficiency tailwinds is likely synonymous with the Protocol Sink Thesis (👈this is required reading if you haven’t yet)

Assets that are deep in the protocol sink benefit more from the progress of capital efficiency of DeFi. Assets that have less risk and more credible nuetrality are better collateral for apps. The better an asset can be collateral, the more it can capture the tailwinds of DeFi capital efficiency.

Guess what asset is deepest down in the protocol sink?

ETH. Ether sets the floor for the protocol sink. The most risk-free, trust-free asset on Ethereum captures DeFi’s tailwinds the most, and that asset is ETH.

The trend is clear

DeFi is on an unstoppable march with its eyes are on capital efficiency, and Ether is the best asset available for DeFi to achieve its goals.

While the Ethereum protocol is busy turning ETH into ultra sound money, Ethereum’s application layer is simultaneously trying to make it the most capital efficient asset in the world.

Capital Efficiency Attracts Capital

When you can achieve the same financial results with less capital, capital will flow into the asset that enabled the capital efficiency. If it takes $10 USD to achieve the same outcome that $1 of ETH can provide, it is simply smart capital management to purchase and hold the asset that allows you to achieve your goals with the least amount of capital. The optionality that ETH can offer you will be overwhelming from a capital efficiency standpoint.

Over time, the path towards achieving specific financial goals will be increasingly routed through using ETH as capital. At this point, ETH will become the internets reserve currency, and its economic bandwidth will be massive.

DeFi is turning ETH into the best Store of Value inside of its internal ecosystem. If ‘DeFi’ ever just becomes ‘Fi’, then ETH will therefore also become the world’s best Store of Value.

If DeFi does become just ‘Fi’, then we can only assume that the rate of ETH burn from EIP1559 would be large, which in turn makes the incentive to stake ETH even higher (to capture MEV fees).

All of these properties create a virtuous loop of positive tailwinds for ETH; strength in one feeds into strengths for others.

ETH is ultra sound, hyper-efficient money

- David

P.S.

At this point, I’ve written so much about Ethereum and ETH that my articles are themselves compositions of my previous articles. If you want further reading material to bolster your understanding of ETH, Ethereum, and DeFi, these three articles are precursors to this one:

- Ethereum is an Emergent Structure - DeFi is a single structure of many modular applications. The structure is self-organizing and self-building.

- Ether is Equity - The price of ETH is a direct reflection of the value of Ethereum.

- Global Public Goods and the Protocol Sink Thesis - Ethereum is a platform for hosting and propagating global public goods in money and finance. The deeper down the protocol sink, the more of a public good.

Action steps

Use ETH :)

Read David’s previous bull case for ETH articles: