DeFi will do to banks what the Internet did to newspapers

Listen to ETH is undervalued the Bonus Bankless Podcast episode that just dropped…

Dear Crypto Natives,

Newspapers are mostly dead. Those that survived are transformed.

But we still get news.

Banks?

We still need banking—but do we need banks?

Sure…but not in their current form. Some will die in the DeFi revolution—and those that survive will be utterly transformed.

That’s the argument Nemil makes today.

That DeFi is about to do to banks what the Internet did to newspapers. 🔥

- RSA

🙏Sponsor: Aave—earn high yields on deposits & borrow at the best possible rate!

WRITERS CORNER

Post by: Nemil Dalal, Product at Coinbase and former Y Combinator Alum

DeFi will do to banks what the Internet did to newspapers

The early days of the World Wide Web were a heady time for newspapers.

In the preceding years, newspapers had been fantastically profitable with monopolistic local markets, vertical integration, and wide readership.

Then the Internet hit with gale force. First, Craigslist disrupted the classified model, sapping a reliable moneymaker. Then ad platforms and search engines started siphoning off ad revenue, and later stole the content. Social media accelerated the trend, leading to competition for breaking news. Newspaper’s “album model” broke down, with single articles—clickbait—dominating.

It took till almost 2020 for the carnage to stabilize. Monthly subscription services slowly took hold, but only for the most respected national newspapers. By the time it was done, 60% of newspaper jobs were gone and the process of news-making was transformed.

In 2020, the target is no less a critical backbone of our daily life: the banks.

The humble bank in the age of crypto

American banks have changed dramatically in the age of the Internet.

Mobile banking has become the norm. Checks are now scanned, instead of physically deposited. The Neo banks—Monzo, Chime, Revolut—are ascendant, with a mobile banking focus and continuing innovations (paychecks two days early! free money exchange! fee-free ATMs!). In certain payments networks, bank transfers can happen in realtime. And yet some curious characteristics persist.

")

(Above) Run-on the American Union Bank (1931) (Source: Wikimedia)

{kind=link}

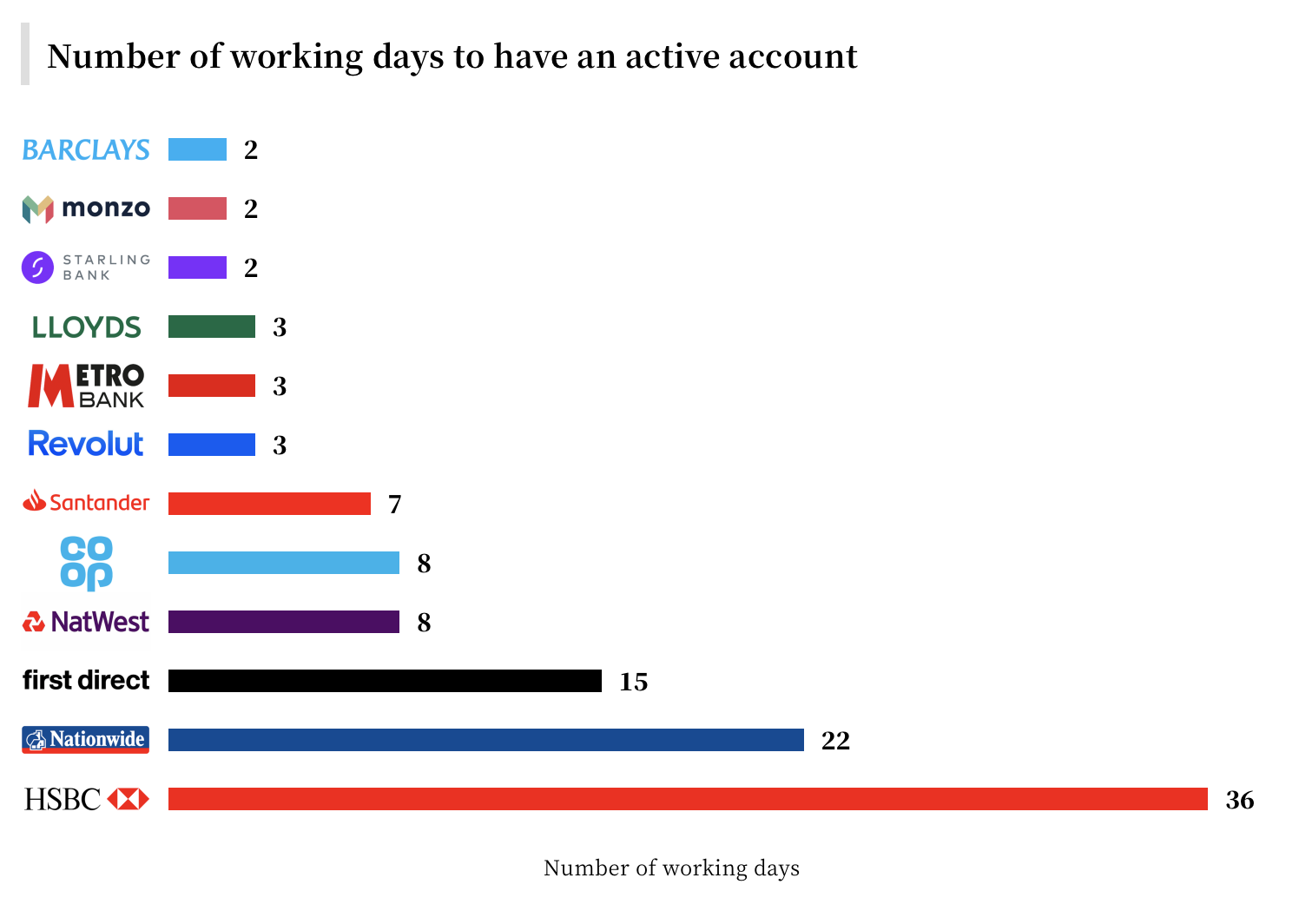

Banking hours are still 9 to 5 on weekdays. Physical bank branches—83,000+ in the US at last count—are still critical for collecting retail deposits. Bank transfers still take days (in the US anyway). Regulations protect user funds, but also make it difficult for anyone to start a bank. Wire transfers still have high fees and a cumbersome process to send funds (routing? account? receiver name? address? bank address?).

Even simply opening a bank account takes anywhere from 2 days to 36 days:

Source: Built for Mars, “Opening an Account”

Enter Compound.

Compound: The Anti-Bank

With just $117 MM in deposits (JP Morgan has $1 TN+), Compound seems to be a curious bank challenger.

The protocol lives exclusively in smart contract code on the Ethereum blockchain:

pragma solidity ^0.5.16;pragma experimental ABIEncoderV2;contract Comp { /// @notice EIP-20 token name for this token string public constant name = "Compound"; /// @notice EIP-20 token symbol for this token string public constant symbol = "COMP"; /// @notice EIP-20 token decimals for this token uint8 public constant decimals = 18;

At last count, just a few million users in the world have figured out how to access to blockchain networks. But Compound augurs a seismic shift for banking.

At its core, a bank is a surprisingly simple beast. Savers deposit funds at a low rate. Borrowers borrow them at a higher rate.

The bank makes money on the spread or net interest margin and ensures that borrowers pay it back. Both the bank and government aim to make sure that borrowers don’t all come calling at once, preventing a liquidity crisis.

By that definition, Compound is a bank. Savers deposit crypto assets to earn a yield. Borrowers borrow these tokens, but also offer collateral. Compound makes money off the spread. But Compound has a few superpowers that banks don’t.

Let’s talk three:

1. Compound is global

Anyone in the world can access it. Before the Glass-Steagall legislation was repealed in 1999, banks weren’t allowed to cross state boundaries. Today, there are few worldwide banks.

Smart contracts and the blockchain make worldwide banks not just possible, but trivial.

2. Compound is regulated by code, not people

Banks are highly regulated because they control your money, and can run away with it or poorly lend it. Regular bank examinations protect user funds, but also limit who can start banks, reducing the competition.

Compound enacts its own regulation: their developers write the protocol — the smart contract programmer’s version of a constitution — and reserve most rights for their users or voters. Not being burdened by traditional regulation is a fantastic power for a bank challenger. It doesn’t mean that Compound comes without risk — borrowers can still default and the code can have bugs — but Compound’s owner can’t run away with the funds.

3. The blockchain—like the Internet—is 24/7 and lightning-fast

Compound can take advantage of global transfers that move in a matter of minutes or even seconds. A billion dollars can be sent for $0.50. By comparison, the US banking system is cobbled together from 1970s COBOL mainframes, stitched together in the aftermath of Glass-Steagall consolidation.

The future of financial services

Instead of going bankless, I’ll argue that we are simply redefining the bank. After all, we redefined how we got news in the 21st century through realtime reporting, social media, and news aggregators.

The bank won’t be reinvented overnight. It took 20 years for the full force of the Internet to be felt on newspapers. Users will need to be able to access the blockchain. Smart contracts will have to be debated the way constitutions or bank charters once were. Risk management will need to become the norm. But the future is already here.

The dislocation won’t stop at banks but hit much of Wall Street. Since the launch of Bitcoin in 2009, cryptocurrency exchanges have proliferated, creating a veritable alternate financial system with 24/7 asset trading around the world. Smart contract projects like dYdX make shorting trivial and liquid. Exchanges like Uniswap and Kyber allow worldwide trading of any asset at any volume.

Though fintech innovation has accelerated in the last decade, real financial disruption is just starting.

Author bio

Post by: Nemil Dalal, Product at Coinbase and former Y Combinator Alum

Action steps

- Recap—what’s the difference between DeFi protocols vs legacy banks?

- Will crypto disrupt banks the way the Internet disrupted newspapers?

Subscribe to Bankless. $12 per mo. Includes archive access, Inner Circle & Deal Sheet.

🙏Thanks to our sponsor

Aave

Aave is an open source and non-custodial protocol for money market creation. Originally launched with the Aave Market, it now supports Uniswap and TokenSet markets and enables users and developers to earn interest and leverage their assets. Aave also pioneered Flash Loans, an innovative DeFi building block for developers to build self-liquidations, collateral swaps, and more. Check it out here.

Not financial or tax advice. This newsletter is strictly educational and is not investment advice or a solicitation to buy or sell any assets or to make any financial decisions. This newsletter is not tax advice. Talk to your accountant. Do your own research.

Disclosure. From time-to-time I may add links in this newsletter to products I use. I may receive commission if you make a purchase through one of these links. I’ll always disclose when this is the case.