Dear Crypto Natives,

You know all the DeFi voting tokens popping up?

I think the successful ones will all become cash-flow tokens.

I’ll explain why. But first let’s recap:

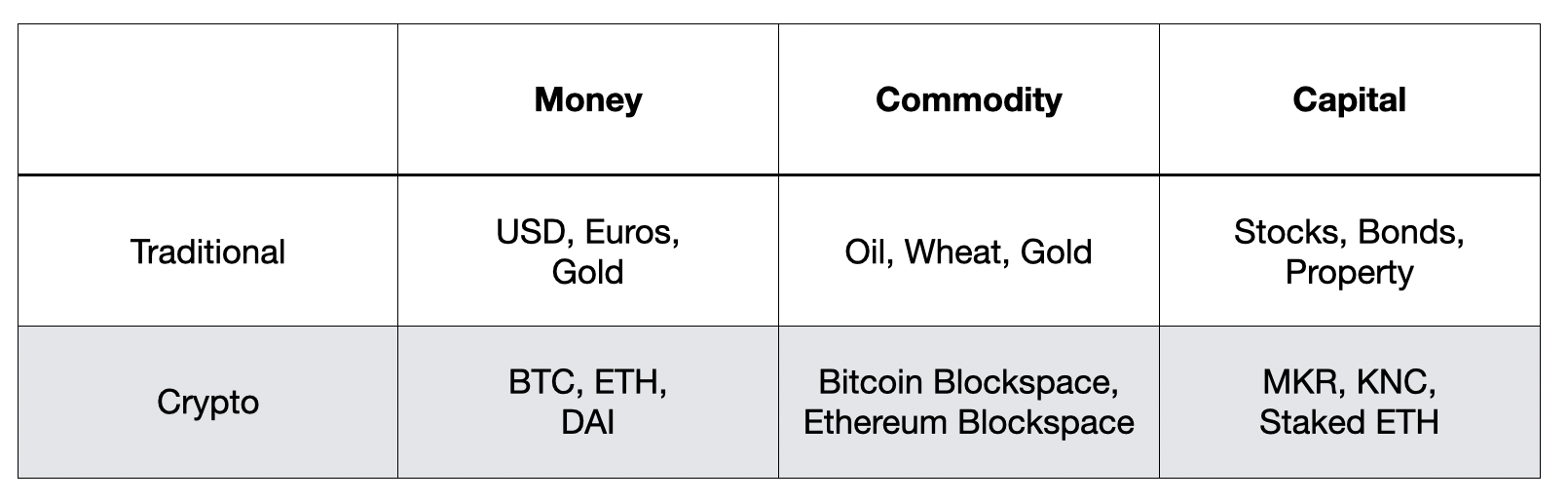

I’ve said that crypto didn’t give birth to one new asset class—it gave birth to three:

- Crypto monies - assets valued as money—store value, exchange, unit of account

- Crypto commodities - assets valued as ingredients in other products

- Crypto capital assets - assets valued based on cash flows

These three asset classes exist in traditional finance too:

But in crypto these asset types are issued and settled on trustless public chains. That’s the difference between crypto & traditional. (BTW, understanding where each crypto asset fits and how it should be valued as a result is half the battle in crypto investing.)

Off-chain and on-chain cash flows

Crypto tokens that provide cash flows to holders fit squarely in the capital assets class. But we can further evaluate these capital asset tokens based on their cash flows:

- Off-chain—capital asset tokens w/ cash flows settled offchain

- On-chain—capital asset tokens tokens w/ cash flows settled onchain

The BNB Binance token? That’s an example of an off-chain capital asset (albeit one without the legal protections of traditional equities). A portion of profits generated by the Binance exchange is used to burn tokens. These cash flows aren’t autonomously driven by protocol code—humans are involved. Revenues aren’t onchain and transparent, you have to trust the numbers from a crypto bank.

(Above) Binance token burn as reported by Binance—cash-flows require trust in Binance

Off-chain cash flow tokens like BNB are a form of psudeo-equity. They’re like securities, but without legal protections. Crypto bank assets like LEO and HT fit this mold too. They combine cash flows with in-economy discounts and loyalty incentives—almost like a grey market version of airline miles meets stocks.

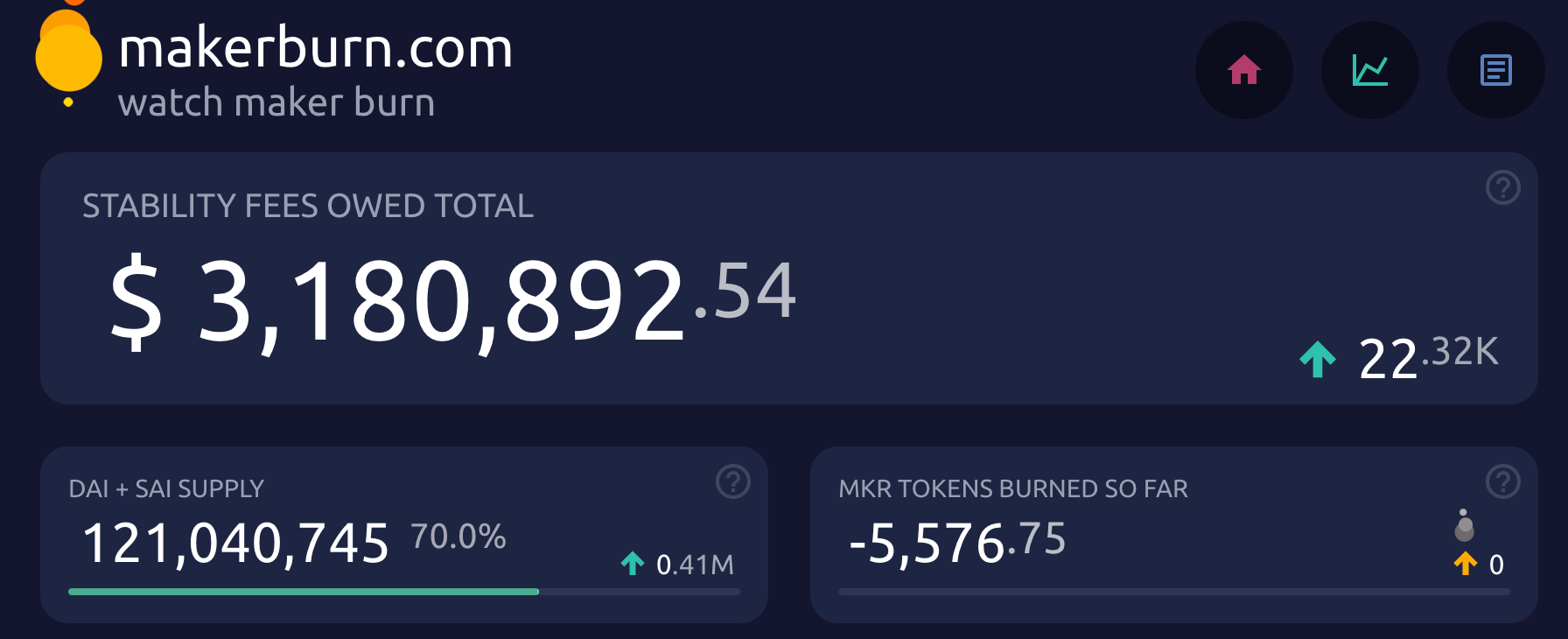

On-chain cash flows assets are the second type. MKR is an example. These are novel, crypto native capital assets. All cash flows for these tokens settle on-chain and are executed via autonomous code. Asset revenue is transparent. These capital assets are permissionless and accessible to anyone with an internet connection.

(Above) Watch cash flows burnt in real-time for MKR onchain—trust in code

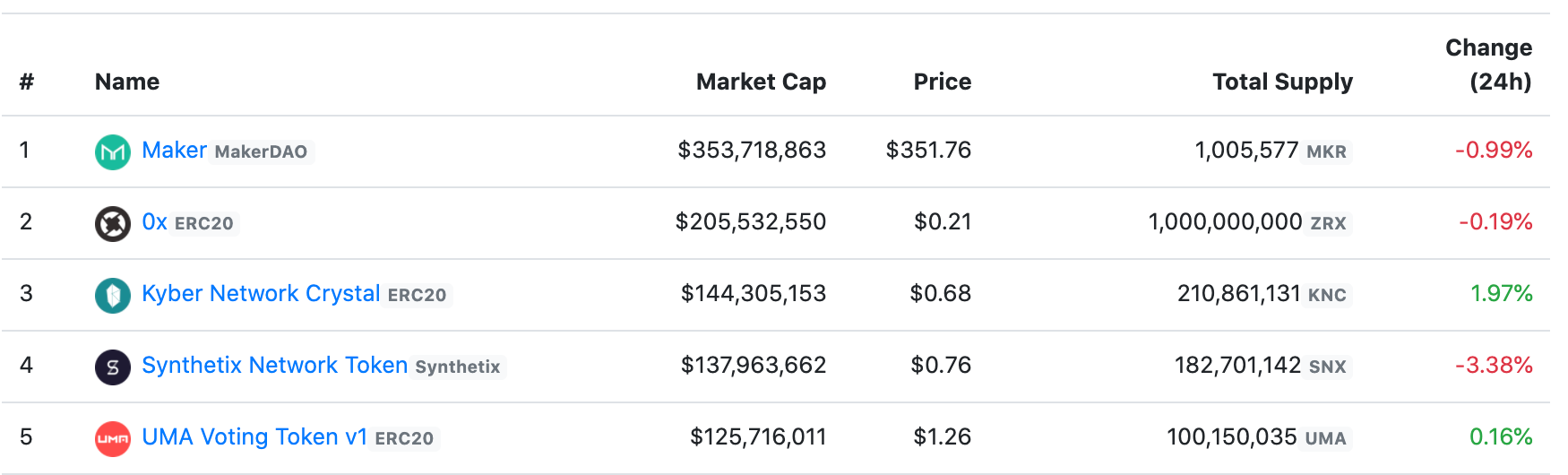

On-chain voting tokens

Crypto native capital assets can decide things onchain too.

In MKR, protocol voting rights (e.g. governance) and cash flows rights are bundled inside the same asset. 1 MKR token = 1 share of cash flows = 1 governance vote. Bundling these rights makes sense—decision makers should have skin in game. Bad decisions should cost them and good decisions should give them some reward. This structure produces better outcomes over time. It’s no accident that traditional assets evolved this way too—voting and cash rights are almost always imbued in the same equity asset.

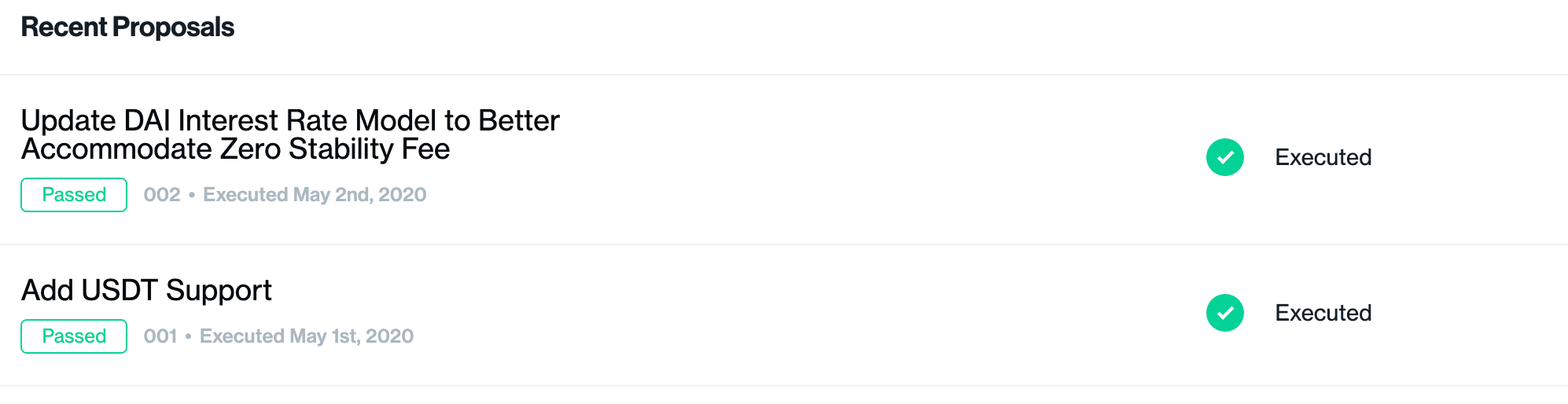

But a newer set of protocol tokens are entering the landscape as voting-only tokens. I talked about some of these yesterday—tokens like COMP and UMA. These are used for governance only, there’s no access to protocol cash flows. At least, not yet.

(Above) Compound governance proposals executed by COMP vote

Voting Tokens will become Cash Flow Tokens

While some DeFi tokens start as voting tokens only, in the long-term I expect most to become more like MKR—that is, they’ll become cash flow tokens too.

Why? Incentives.

COMP holders for example are incentivized to support proposals that add a fee structure to Compound that’s allocated partially to themselves as profit and partially to further growth of the protocol. They can’t add too many fees or they’ll lose users, so they’ll add just enough to fund Compound growth while extracting some profit. Fees will rest at a price equilibrium driven by market forces.

Over time, this will give rise to a large assortment of on-chain capital assets, each backed by protocol cash flows. An S&P500 of protocol assets.

The Opportunity to Govern

DeFi governance tokens becoming cash-flow tokens.

Are you seeing why I think there’s a massive opportunity for the bankless community in the area of DeFi governance? Every DeFi protocol needs engagement from a community of knowledgable DeFi users to help them successfully govern their protocols and cross the chasm—to transform from governance to cash-flow assets through permissionless governance.

They can’t do this alone.

If their governance is centralized and decided off-chain with a permissioned group of decision makers then DeFi protocols won’t cross the chasm. They need groups of DeFi users to step up and govern. I think that’s what Compound wants. That’s what UMA team is asking for. And that’s what mature protocols like MKR have put in place.

The protocols need the bankless community to step up and govern.

That why I sent you the message yesterday.

We have the opportunity to govern. To help tokens cross the chasm.

And if we do it well, some of the protocol tokens we help govern may one day form the S&P500 of our new bankless money system. Wouldn’t that be cool?

- RSA