Dear Bankless Nation,

The past few months have been turbulent for the crypto industry.

Multi-billion dollar crypto banks are going bankrupt.

The biggest hedge funds are dumping their jpegs to cover liquidations.

It’s not pretty. The centralized crypto institutions are crumbling.

But you know what didn’t break? DeFi.

They continue to process liquidations as expected. No funny business, no handshakes behind closed doors, just complete transparency at all times.

This is what we’ve been preaching: Open, public, accessible financial software for the world.

Because of this, DeFi will never die.

Resident Bankless Editor Donovan Choy explains more.

- Bankless Team

Resiliency, antifragility, transparency.

Here’s a non-controversial premise: People are often ignorant, greedy, and hopelessly unequipped to navigate a complex world.

How then should we design economic systems around that fact?

The mark of a resilient economic system is one that accepts those sober realities and builds itself around these unideal, but real circumstances, rather than over them.

Resiliency does not depend on bull prices, but rather on the ability to adapt to changing market conditions without the need for external interventions from regulators or benevolent billionaires.

In the world of finance, resilient systems need to answer a few key questions affirmatively:

- Can the system expel bad debt effectively?

- Does it disincentivize and weed out unsustainable business models, or does it prop them up?

- Can it do both of the above before systemic risk accumulates?

- When systemic risk presents itself, can it resolve the problem with minimal active management and negative spillovers?

The case for decentralized finance is strongly linked to how it achieves these objectives better than its centralized counterparts.

From the design of a protocol’s token economics, to its day-to-day treasury management, and the health of its balance sheets: everything in DeFi is transparently observable on the blockchain and monitorable in real-time.

It lets us see where big players have placed their bets, and where there’s a concentration of risk.

The mainstream media frequently paints DeFi as a “wild west of finance,” but the reality is far less lawless than the metaphor suggests. DeFi is replete with self-regulatory mechanisms.

Self-regulation in decentralized finance

Let’s take recent self-regulatory attempts of Lido Finance and Solend for example:

Lido controls ~⅓ of ETH’s circulating supply. Its concentrated ETH holdings prompted researchers from the Ethereum foundation and Vitalik himself to sound the alarm bells of a possible centralization threat to Ethereum. What followed was a lot of debate, then a governance proposal to self-limit the amount of ETH deposits into the liquid staking protocol. That governance proposal failed, but a further decentralization of Lido’s validator set was installed by adding eight new validators.

Solend — Solana’s top lending protocol — faced a more imminent threat. It was discovered that one whale had a disproportionately large margin position ($170M) that might trigger a catastrophic liquidation event and impact the entire chain if SOL’s price continued to drop.

In response, Solend developers introduced a series of governance proposals to the community, first proposing to takeover the whale’s account and execute a safe liquidation, but eventually landed on a solution to introduce a new constitutional rule that capped borrow limits to $50M (the whale borrowed $108M).

It may well be that Lido and Solend are not out of the woods yet, but both episodes of governance illustrate something unique about DeFi.

Transparency over the rules of the blockchain network and on-chain activity enabled a community of internal and external stakeholders to rally over a common cause of concern and reach a solution collectively. Both cases saw stakeholders waving red flags and engaging each other in deeply technical discussions before—not after—it was too late.

People make stupid risks, systems are maliciously attacked and things go wrong. The question is what rules of the game best deal with that. TradFi’s answer to that is, “The government will pass a law”.

DeFi’s answer to that is, “We’ll let the code decide”.

The Fall of Centralized Finance

In contrast, consider the domino of crypto banks toppling over in the past month.

At the center of this fiasco is too-big-to-fail venture fund Three Arrows Capital. The earliest signs of 3AC’s liquidity problems came into light when they faced high volumes of liquidations ($400M) in OTC trades during the mid-June market crash that couldn’t be kept under wraps.

3AC’s instability quickly brought to light a series of risky shadow trades that crypto banks were making to one another behind closed doors with their depositor’s money. BlockFi made an overcollaterized loan of $1B to 3AC while Voyager Digital loaned a further ~670M.

Despite the latter’s relatively safe capital ratio level of 4.3%, what led to its current predicament was the risky decision of making one concentrated loan of more than twice its total capital to one hedge fund.

Of course, risky trading takes place all across finance, not just crypto banks. The existence of risk is not the main point here, but rather how the system governs and deals with risk.

Unlike DeFi, the centralized balance sheets of crypto banks excluded the ability of netizens to independently investigate.

These overleveraged and risky trades were only made known when the boiling water was spilling out the pot — after it was too late. That a liquidity crisis was going on among crypto banks was made public knowledge only because doing so was legally necessary to get the money back.

The troubles of centralized crypto banks lie chiefly in the fact that much of its trades were made bilateral OTC trades behind closed doors that were privy only to insiders.

The DeFi aspects of centralized players

An apt way to illustrate the comparative advantage of DeFi is to look at the median: centralized players making decentralized trades.

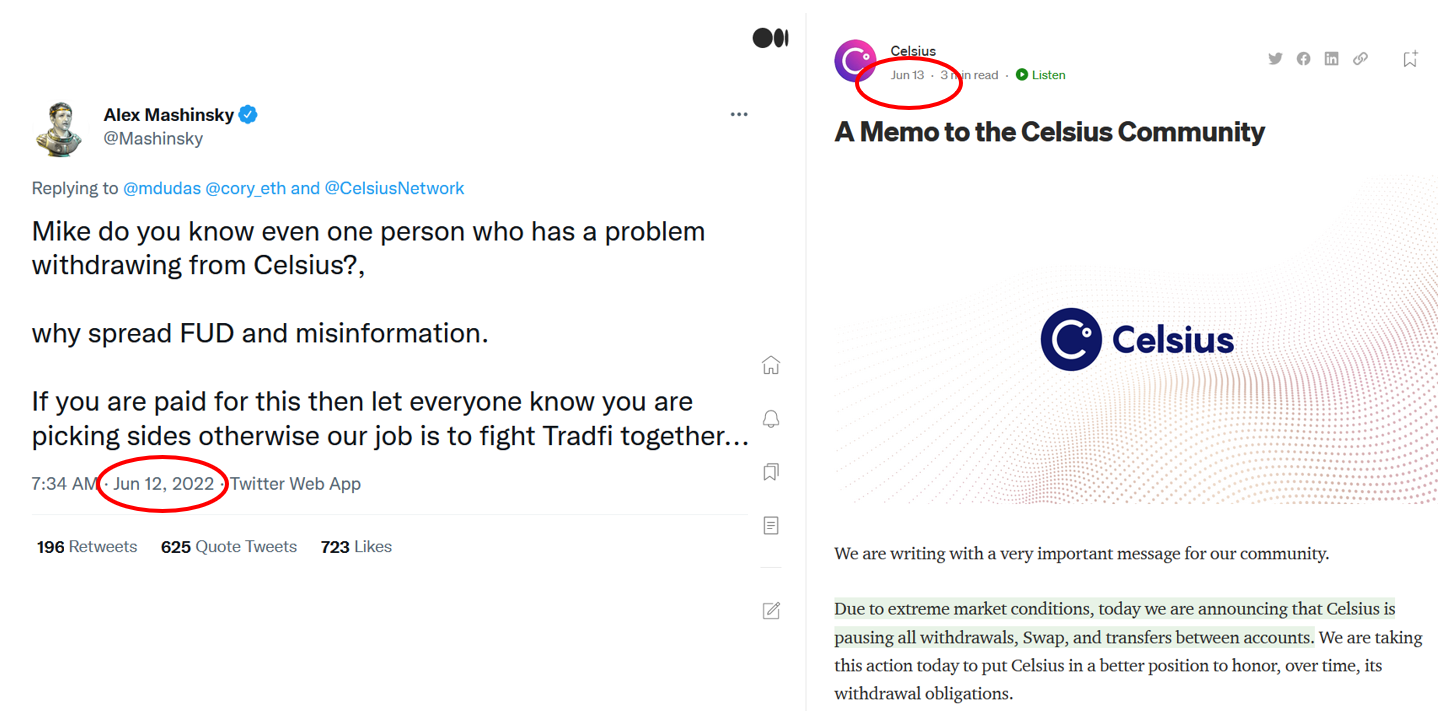

For example, Celsius’ troubles were first exposed when there were clues of its insolvency in a range of on-chain loans. These included a stake of 17,900 WBTC in a Maker vault that Celsius rushed to top up to avoid liquidation from a fall in Bitcoin prices (the loan was fully paid on 7th July), a stake of 458K stETH on Aave (as that price was deviating from ETH), and more on Compound and Oasis.

Thanks to its on-chain exposure, crypto observers were able to partially examine the weather forecast for an impending storm.

Sure enough, Celsius halted withdrawals just a day after its CEO rebuked speculative accusations that Celsius was nearing insolvency. The alarm bells rang a little too late, but the silver lining is that the damage could’ve gone on for longer.

Another illustrative example on the median is the Terra blowup in May. The signs of that catastrophe were completely transparent from the get-go, as liquidity first starting drying up quickly on Curve. As my colleague Ben puts it:

“UST’s peg first came under duress on Saturday, May 7, as a result of an $85 million swap from UST to USDC in the USTw-3CRV Curve pool… This large trade wound up shaking confidence in the pool’s liquidity providers, who quickly withdrew their 3CRV, causing the pool's balance to dip as low as 77% UST and 23% 3CRV on May 8.”

What followed was the most centralized and definitively anti-DeFi aspect of the saga.

As millions of Terra investors began to panic, Do Kwon famously tweeted out “Deploying more capital - steady lads,” while Terra’s centralized entity Luna Foundation Guard began offloading $1.5B in Bitcoin to defend the peg of its algorithmic stablecoin.

None of this was bound by smart contract rules and was in effect a promise. By that time, Anchor outflows went out in a flood and Terra was already done for.

In the case of 3AC, analysts knew its balance sheets were unhealthy due to on-chain evidence exposing its previous losses of $560M in locked LUNA from May, as well as evidence of them offing their stETH positions in June. The puzzle of 3AC’s insolvency wasn’t complete, but partial pieces enabled credible speculation.

Finally, as these companies were fast approaching insolvency, DeFi loans were predominantly the ones being paid down because that was the only option, while the risky and leveraged closed-door bilateral trades between CeFi platforms were relegated to the legal system.

Why? You can argue for a better deal in a court of law, but you can’t argue with a smart contract.

All of these examples illustrate a cogent point: Celsius, Terra and 3AC had one foot in the on-chain world, which was the key to detecting possible exposure of their unsustainability before the end was nigh. That didn’t completely avert or deter a crisis like in the case of Lido and Solend — but it would have if they were fully DeFi-native.

Closing

To reiterate an earlier point, the rightful starting point of the social sciences is that people are often greedy, stupid knaves. The Scottish Enlightenment philosopher David Hume argued that truly resilient political-economic systems should be built around that fundamental fact of human nature:

…every man ought to be supposed a knave, and to have no other end, in all his actions, than private interest. By this interest we must govern him, and, by means of it, make him, notwithstanding his insatiable avarice and ambition, co-operate to public good.

DeFi’s strengths come from making no naive assumptions around that simple reality. It takes the flaws of humans, and designs cold, heartless smart contracts around it. Ryan puts it nicely in last week’s rollup: the code is the liquidator and the settlement engine in DeFi.

In the midst of the 3AC fallout, major DeFi protocols like Aave, Compound and Maker functioned smoothly by executing liquidations and expelling bad debt. In the month of June 2022 alone, 9-figure liquidations took place across Compound ($9.9M), Aave ($2.6M) and Maker ($49M) without a hitch.

When shit hits the fan, that means no closed-door bargaining, no deferring of the problem to the courts, no lobbying of regulators, just the simple rules of immutable smart contracts by which we agree to abide by.

Now, that’s what a resilient economic system looks like.

That’s DeFi.

Action steps

- 🤔 Consider the benefits of DeFi vs. CeFi

- 📖 Read CeFi broke. DeFi didn’t