Why DAOs need to diversify

Dear Bankless Nation,

DAO treasuries are worth billions.

The problem is that almost all of that value is held in the DAO’s native token.

And as Hasu elegantly outlined in this article, these tokens aren’t assets. They are the equivalent of authorized un-issued shares for the treasury.

DAOs can’t easily sell them.

But they need to.

These organizations shouldn’t be relying solely on their native treasuries for support. What happens if another bear market happens and the value drops by -70%, -80%, or -90%?

They need to have a couple of years of runway for operating expenses— ideally in stablecoins.

But it’s no easy task. DAOs can’t just sell their tokens on a DEX as that would cause significant price impacts.

They need to get creative.

Shreyas shows us 5 ways on how DAOs can diversify their treasuries.

- RSA

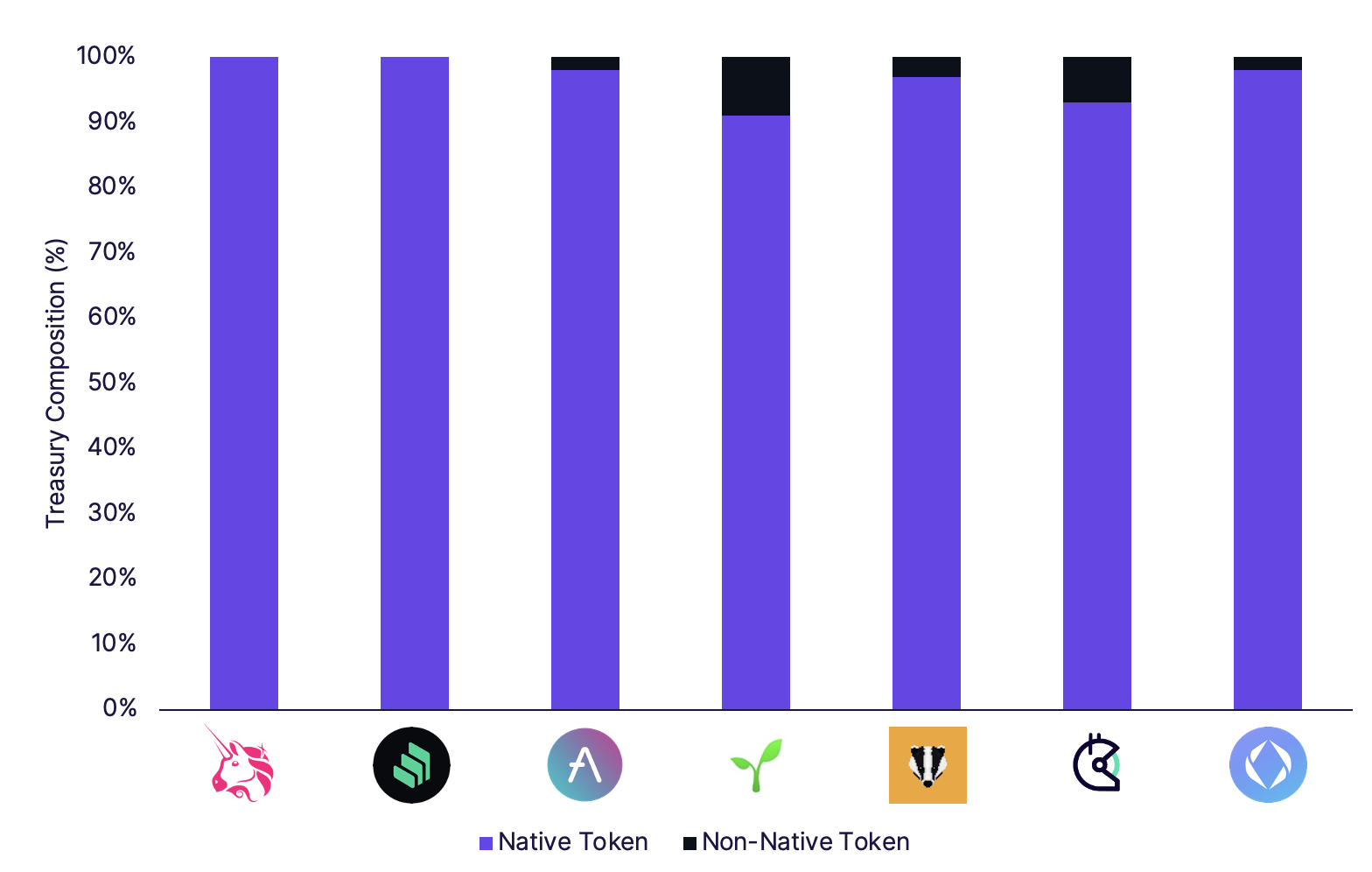

DAO treasuries have grown significantly over the past two years. Even after the recent market drawdown, the top 50 treasuries (fully vested) are worth close to $15 billion. However, a majority still hold over 90% of their treasuries in native tokens.

As this post outlines, native tokens should be thought of as the crypto-equivalent of authorized but unissued shares. If Uniswap tried to liquidate 1% of its liquid treasury from UNI to DAI on 1Inch today, the slippage would be over 95%.

DAO spending is increasing

Over the past year, Uniswap, Aave, Compound, dYdX, and PoolTogether have launched grants programs funded by the treasury. Index Coop, Yearn, Gitcoin, and Maker have formed internal working groups and pay contributors from the treasury. By rough estimates, these DAOs alone are spending over $100 million combined per year in native tokens, and this excludes spending on liquidity mining campaigns.

Spending is still extremely low relative to what is optimal at the growth stage of many DAOs.

However, spending is significant enough to justify having stablecoins in the treasury to cover 2-3 years of operating expenses.

Why DAOs should diversify into stablecoins

“When the tissue box is full, you take two tissues. When it is nearly empty, you take half a tissue.”

DAOs should ensure that their treasuries have stablecoins that cover at least 2-3 years of operating expenses.

This prevents painful budget cuts during a bear market.

Here are the main reasons for stablecoin diversification:

Reason 1: De-risk the treasury

Native tokens are highly volatile; it is not unusual for token prices to fall over 70%.

Stablecoin diversification enables the DAO to operate from a position of strength in the event of a market drawdown. Spending can be maintained or increased during a bear market—whether it is core development, M&A, token buybacks, or LP subsidies.

Reason 2: Manage a predictable budget

Working groups and grants committees are allocated a certain amount of native tokens every quarter to spend. It is difficult for them to budget their expenses for the next quarter or year if they have to account for native token volatility, making working capital forecasting and management challenging.

Stablecoins held in the main treasury reduce the treasury management burden for working groups. For example, Gitcoin has several working groups including the Public Goods Workstream, Moonshot Collective, Fraud Detection and Defense, DAO Operations, etc.

Every quarter, these working groups are allocated GTC tokens after governance approval. Working groups have to manage a quarterly budget with tokens that are volatile and may need to diversify into stablecoins. To reduce the treasury management burden on working groups, the Gitcoin treasury can hold stablecoins and allocate them to working groups as needed.

Reason 3: Pay contributors

Governance contributors, grant recipients, and security bounty recipients can have the option to be remunerated partly in stablecoins along with vested native tokens.

This can be particularly useful for full-time contributors who need to take care of their personal fiat denominated expenses.

Reason 4: Other benefits

Treasuries with stablecoins will have a higher credit rating and potentially get more favorable terms when they borrow using their native tokens as collateral.

DAOs can utilize stablecoins in a way that is specific to their needs. For example, Uniswap can provide liquidity on v3 stablecoin pools to deepen liquidity and earn transaction fees.

Stablecoins can be deposited to earn yield using Aave, Compound, or Yearn. They can also be used to buy on-chain money market fund products.

How DAOs can diversify into stablecoins

There are several ways that DAOs can accumulate stablecoins. Each of them come with trade-offs, and more DeFi-native diversification methods will continue to be built.

1. Earn revenue in stablecoins

Earning revenue in stablecoins is the least controversial way to accrue stablecoins. It does not involve selling native tokens so is non-dilutive.

Lending protocols like Aave are well suited to the stablecoin revenue model. In V2, Aave introduced a reserve factor that directs a share of the interest paid by borrowers to the ecosystem collector. To date, close to $28 million in aTokens have accrued to the v2 revenue collector contract. Since aTokens earn interest, they are productive by default.

If Uniswap’s governance decided to turn on fees for v2 or v3, Uniswap will accrue earnings in a long tail of tokens. A decent portion of this revenue would be in stablecoins like USDC and DAI.

2. Sell native tokens for stablecoins

Selling native tokens for stablecoins seems like a simple action, but there are several ways this action can be done. Each form of selling native tokens comes with its own trade-offs.

Decentralized exchanges

A DAO could sell native tokens can be sold on a decentralized exchange like Uniswap, Sushiswap, or Cowswap, or on a DEX aggregator like 1Inch.

While the sale can be done on-chain and trustlessly, slippage can be quite high. Even if the sale is executed over several weeks or months, it needs to be done in public, which means there is a chance of getting front-run or sandwiched due to MEV.

OTC & market makers

Market makers like Wintermute and Alameda Research can help execute large token sales. In April 2021, Vitalik Buterin donated $1 billion worth of SHIB (Shiba Inu) tokens to Crypto Relief, a community-run COVID relief fund in India. SHIB tokens were relatively illiquid given the size of Vitalik’s donation. However, through a combination of on-chain and off-chain methods, Wintermute was able to convert a sizable amount of SHIB to USDC.

While execution can be better with market makers, it is not as transparent and DAO-native. The DAO needs to transfer tokens to the market maker and trust them on implementation.

Batch auctions

Rather than selling tokens on the open market, they can be sold via batch auctions by Gnosis. Batch auctions help match the limit orders of buyers and sellers with the same clearing price for all participants. If the DAO wishes, they can have the option to whitelist / KYC participants of the batch auction by partnering with a group like Fireblocks.

Batch auctions can be executed entirely on-chain and reduce the risk of getting front-run or sandwiched. However, they do take slightly longer to set up and execute, and require sufficient demand to be generated to bid for the native token.

Bonding curves

A bonding curve describes the relationship between the price of the token and its supply. The more tokens that have been distributed, the higher the price.

They enable a fixed price discovery mechanism that is transparent to market participants and cannot be manipulated. A native token-to-stablecoin bonding curve on a Balancer pool can be used to diversify a treasury into stablecoins.

3. Form Strategic Partnerships

Selling native tokens for stablecoins in the open market might lead to native tokens held by short-term holders. Instead, DAOs can exchange native tokens for stablecoins with long-term strategic partners, which can include VCs, DAOs, and value-additive individuals.

Llama is currently working on a treasury diversification proposal for GitcoinDAO. It is important that a strategic partnership process should be community-first. The process should be agile, efficient, and transparent.

Treasury diversifications via strategic partnerships have also been done by Lido (lead by Paradigm). PoolTogether: (ParaFi, Galaxy Digital. etc.), FWB (lead by a16z), Forefront (lead by 1kx), among others. In these partnerships, native tokens typically have a lock up period and are sold at a discount.

Communities like Sushi have questioned whether native tokens should be sold to VCs at a discount. To solve this problem, UMA Protocol built range tokens, a treasury primitive that resembles convertible debt without liquidation risk. One of the problems with range tokens is that VCs primarily want pure upside exposure rather than yield that comes from a debt-like product. To address this, UMA built success tokens, which are two tokens wrapped into one—the DAO’s native token and a call option on that token.

While strategic partnerships help get native tokens in the hands of long-term holders, they are time-intensive and require a lot of off-chain coordination to find the right partners. It is also a discrete action rather than a continuous one. After getting 2-3 years of operating expenses in stablecoins, the DAO has to take this action again.

4. Borrow against native tokens

Debt is a largely unutilized part of DAO capital structures. Accruing stablecoins in the treasury via borrowing does not fully de-risk the treasury because of liquidation risk. However, the advantages are that it is a simpler action than a strategic partnership (less off-chain coordination) and it is a continuous action rather than a discrete one.

Variable rate debt

Treasuries can deposit native tokens on lending protocols like Aave and Compound to borrow stablecoins at a variable rate. Since Aave and Compound have a governance and risk management process to add collateral types, there are a limited number of tokens that can borrow from them. As an alternative, DAOs can create a Fuse pool on Rari, deposit their native tokens, and borrow stablecoins against them.

Variable rate borrowing comes with risks. Rates may spike up depending on market conditions and the DAO has to manage liquidation risk.

Fixed rate debt

Fixed rate debt allows DAOs to model out their cost of capital more easily. It can help fund operations, protocol acquisitions, and potentially yield farming (via debt rather than tokens).

DAOs can deposit their collateral in Element or Yield and borrow stablecoins against them. Alternatively, DAOs can access a secured line of credit that can help fund operations. DebtDAO is also working on a few interesting solutions for DAOs to borrow stablecoins.

Bond issuance

While under-collateralized debt for individuals is more difficult to underwrite on-chain, it is easier to do so for DAOs.

There would likely be demand for bonds issued by the top 10 DeFi protocols. It would let them raise capital without diluting token ownership or even putting up too much collateral. Porter is an example of an under-collateralized bond protocol for DAOs; more might follow.

5. Collaborate with stablecoin issuers

Collaborating with stablecoin issuers like Fei, Frax, Maker, Rai, and others to accrue a stream of stablecoins is a DeFi native solution to the stablecoin problem.

For example, Tribe’s Turbo product, which is built on top of Rari’s Fuse pool, lets DAOs borrow FEI after depositing their native tokens. The borrowed FEI is then deposited in a yield strategy of the DAO’s choosing to pay back the interest on the borrowed FEI.

DAOs Need to Diversify

Stablecoin diversification is one out of many actions that a DAO should take with their treasury. It helps ensure that the DAO can maintain or ramp up spending even when there is a downturn.

Treasuries should be used to increase revenue, build thriving communities, and grow the GDP of the DAO. Stablecoin diversification can serve as a starting point for DAOs to spend more on growth.

At the end of the day, DAOs need to diversify.

This article is their guide on how.

Action steps

- 🔍 Explore different ways to diversify a DAOs treasury

- 📖 Read A New Mental Model for DeFi Treasuries by Hasu

Author Bio

Shreyas Hariharan is the co-founder of Llama, which is building economic infrastructure for DAOs. Llama has a community of 35+ contributors and has worked with Aave, Uniswap, Gitcoin, Fei Protocol, PoolTogether, FWB, Harvest Finance, among others. If you are interested in contributing to Llama, apply here.