Why Circle's IPO Popped Off

View in Browser

Sponsor: Mantle — Mantle is building the largest sustainable hub for on-chain finance.

- 💰 Gemini Crypto Exchange Confidentially Files for IPO. The Winklevoss-founded entity's filing comes after a blockbuster debut for Circle.

- 📊 Polymarket Launches Partnership with Musk's xAI. The crypto-enabled platform will integrate Grok and serve as the official prediction market partner of xAI.

- 🦍 Yuga Labs Proposes Dismantling ApeCoin DAO. Calling the DAO plagued by 'unserious governance theater,' Yuga CEO Greg Solano is proposing its shutdown and transfer to a new entity established by Yuga.

| Prices as of 6pm ET | 24hr | 7d |

|

Crypto $3.25T | ↗ 3.1% | ↘ 0.9% |

|

BTC $104,494 | ↗ 3.1% | ↘ 0.2% |

|

ETH $2,494 | ↗ 2.7% | ↘ 3.1% |

Circle stunned crypto and TradFi observers alike on June 5 as the stock ripped to a day-one high of $103 within 15 minutes of its New York Stock Exchange debut, three times the price paid by buyers of its “25x oversubscribed and upsized” CRCL initial public offering.

Is Circle’s IPO the ultimate opportunity to ride the stablecoin surge, or is this high-flying stock priced for perfection and ignoring risks lurking beneath the surface?

Today, we’re breaking down the CRCL investment opportunity! 👇

🔵 Outlining the CRCL Opportunity

After years of rumor and anticipation, USDC stablecoin issuer Circle Internet Group finally confirmed its IPO desires when it filed documents with the SEC this spring. These filings also gave investors an unprecedented look under the hood of the stablecoin business.

Those documents revealed a revenue powerhouse in a high-growth industry – one which generated over a billion dollars of interest off stablecoin reserves in 2024. Unfortunately, the financials also displayed a business centered around trade-offs – one which teetered on the edge of profitability after accounting for billion-dollar partner payments, hefty compensation incentives, and burdensome compliance costs.

Circle backs USDC with over $60B of cash bank deposits and short-term U.S. Treasuries, and while managing the no-yield stablecoin produced an impressive $1.7B of top line revenue for Circle in 2024, the associated operational expenses paid to attract these reserves also ran quite high.

In 2024, Circle outlaid $1B for “distribution and transaction costs;” this was the Company’s largest expense category and funded partners (primarily Coinbase) for paying USDC users. Circle also incurred substantial payroll expenses – totaling $263M in 2024 – and shelled out $137M on “general and administrative costs” for items including: travel, office space, insurance, legal counsel, and tax services.

Circle enjoyed its second consecutive profitable year in 2024 (an important accounting distinction that could enable the firm’s stock to eventually be included in the S&P 500 broad-market index), but its $155M bottom line paled in comparison to the enormity of chief rival Tether’s reported $13B of net profits for 2024.

🚨 Circle Files for IPO

— matthew sigel, recovering CFA (@matthew_sigel) April 1, 2025

$1.7B revenues (+16% y/y)

$285M EBIDTA (-29% y/y)

$155M Net Income (-42%) pic.twitter.com/qHldPakfRr

📈 Catalysts Pumping the Narrative

Even though Circle’s present $20B+ valuation may appear aggressive relative to initial estimates, the key metric remains tame in comparison to the valuation applied to moonshot crypto-native competitors, such as Ondo. The RWA platform managed to obtain a similar $20B FDV in late January 2025 despite having less than 1% of Circle’s AUM at that time.

Circle profit has fallen during periods of market turmoil when capital allocators retreat from the crypto industry, but this aspect of Circle's business should become insignificant if USDC achieves real-world payments adoption. The same cannot be as easily said for alternative TradFi crypto plays like Coinbase (which is largely dependent on trading activity), BTC/ETH crypto ETFs (which represent direct crypto exposure), or crypto treasury companies (which are highly exposed to the fluctuations in crypto prices).

For regulated financial institutions and more conservative investor types that are confined to traditional market offerings, CRCL may serve as a valuable portfolio diversifier that provides practical blockchain-adjacent exposure while being somewhat removed from the crypto industry’s speculative nature.

Definitely not a supporter of Bitcoin..

— PK (@paul_k_0907) June 5, 2025

But the $CRCL IPO is intriguing..

The problem with Bitcoin is that it isn’t backed by anything of value..

While Circle is an issuer of stable coin.. backed by the US dollar.

So this provides all the benefits of a crypto, with public…

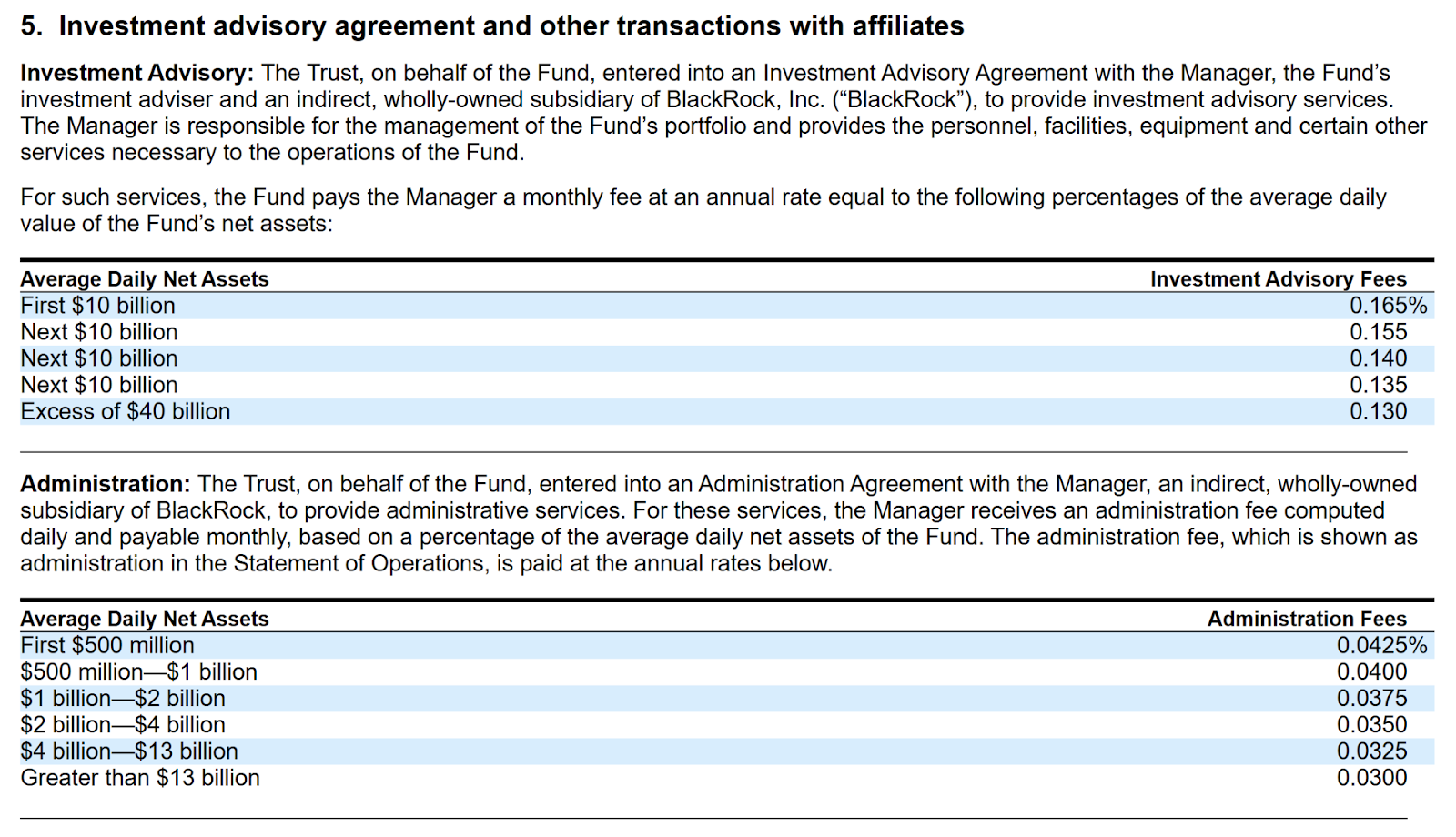

Perhaps the biggest growth catalyst for CRCL is its BlackRock relationship, which practically enshrines Circle as the stablecoin arm of the world’s largest asset manager.

In March 2025, Circle and BlackRock signed a renewed MOU, which is valid for the next four years and increases BlackRock’s share of Circle reserves to 90%. Importantly, the deal requires BlackRock to prioritize Circle stablecoins for all U.S. dollar payment stablecoin-related use cases and prohibits it from launching a competitive payment stablecoin.

Circle’s IPO filing also unveiled the fee schedule for their BlackRock partnership, which includes both “investment advisory” and “administration” fees and creates a direct financial incentive for BlackRock to promote USDC adoption.

📉 Signals Giving Pause

Although many on Crypto Twitter have taken to criticising Circle’s underwriters having the stock IPO at a valuation three times lower than it was trading immediately following listing, in all fairness to them, achieving even the initial $31 offering price initially appeared to many as a tall order.

With Circle holding above the $20B valuation threshold, the stock is now trading at over 130 times its 2024 earnings, a high multiplier typically only found among bubble stocks; to justify such a P/E ratio, Circle must either grow earnings tremendously or invariably face a future stock price slide.

Blockchain-based technologies have high-growth potential, but in a world where stablecoins become the default payment medium, regulation could clear the way for larger entrants (i.e.; banks) to enter the stablecoin space. These established players have the potential to achieve more efficient cost structures than smaller crypto-native players in the face of burdensome regulation, which might enable them to outcompete Circle.

🚨BREAKING: Big banks including JPMorgan Chase, Bank of America, Citigroup, and Wells Fargo are teaming up to launch a shared crypto stablecoin, per WSJ.

— Coin Bureau (@coinbureau) May 23, 2025

TradFi wants a piece of our industry! 👊 pic.twitter.com/LP7MrC1WN4

As an investor in short-term debts that must be constantly rolled to market yields, the single greatest profit risk to Circle is that interest rates fall.

It is no secret that the Federal Reserve is looking to slice interest rates in the near future, and if Circle is unable to aggressively grow USDC supply before this happens, CRCL holders may find themselves in a tough position.

Although the revenue hit of falling interest rates will be somewhat offset by declining distribution expenses, according to Circle’s interest rate sensitivity projections (which held the supply of USDC constant), the company stands to lose $207M of profit for every 1% decrease in short-term interest rates.

Should the Fed cut interest rates by 1% or more before real-world stablecoin payments arrive, Circle will venture into “unprofitable” territory, and its stock price will almost certainly suffer.

🧐 Conclusion

Few crypto observers or traditional finance professionals anticipated the CRCL IPO would blow expectations out of the water to this degree, and while the market is never “wrong,” it is clear that Circle has big shoes to fill if it hopes to live up to a $20B valuation.

Critics may argue that Circle is less profitable than Tether and diverts too much revenue to Coinbase, but it is still the early days for stablecoin experimentation, and CRCL stands out as the clear best choice for equity investors seeking pure exposure to the stablecoin sector.

BlackRock’s MOU requiring prioritization of Circle stablecoins should help to provide a formidable edge once regulatory clarity clears the way for major financial institutions to use stablecoins in everyday operations, yet the entrance of traditional banks into the stablecoin sector also presents a formidable challenge.

These institutions are better positioned to absorb enhanced compliance burdens and could easily undercut the high cost structures of crypto-native players, like Circle.

Moreover, Circle’s bottom line is highly sensitive to macroeconomic conditions. Should recessionary pressures mount and interest rates further decline, the company’s profitability would likely suffer, even if outstanding USDC circulating supply remains flat (an unlikely scenario in a truly risk-off market barring mass stablecoin adoption).

CRCL is certainly an NYSE high-flyer with lofty growth prospects that offers exposure to the institutional embrace of stablecoins, but it is still worth carefully considering core business risks related to increased competition and interest rate uncertainty before aping the stock fresh out of the gate.

Experience the next generation of on-chain finance with Mantle—where blockchain meets everyday banking. Powered by a $4B treasury, Mantle Network and mETH Protocol, Mantle is launching three innovation pillars: Enhanced Index Fund for optimized crypto exposure, Mantle Banking for blockchain-powered banking, and MantleX for AI-driven innovation. Stay tuned and enter the future of on-chain finance with Mantle.