What Do Investors See in Ethena?

Ethena Labs opened deposits into its synthetic dollar stablecoin to the public on February 19, injecting itself into the mind space of practically everyone on Crypto Twitter in the process.

By offering double-digit yields and points for an upcoming airdrop, Ethena’s USDe stablecoin has quickly ballooned to over $770M in supply to become the 6th largest dollar-pegged stablecoin!

Although Ethena’s rise to prominence has certainly been impressive, the project does not come without its critics, who are skeptical of Ethena’s high yields and believe its design leaves it liable to implode like the Terra/Luna ecosystem.

Today, we’re discussing what Ethena does and dissecting the protocol’s risks to help you make an informed decision about whether aping this opportunity is the right play for you!

🧐 What is Ethena?

First off, basis trades have a long-established history, both within crypto and traditional financial markets, and involve arbitraging the differences in pricing between spot assets and futures instruments.

Most commonly, these trades are expressed by going long on a spot asset and shorting its futures, as futures instruments often trade in contango (i.e., at a higher price than the underlying) due to demand for leverage and carry costs associated with holding spot assets.

Historically, crypto markets have also operated in contango, meaning the prices of perpetual futures typically exceed the prices of spot assets, resulting in net positive funding rate environments in which longs pay shorts for the ability to hold their positions.

In this situation, one can easily deploy a lucrative delta-neutral basis trade by holding spot crypto assets and hedging against the notional value of their holdings through perps, allowing the utilizer of this strategy to eliminate their exposure to fluctuations in crypto prices while simultaneously enabling them to earn yield from funding payments.

Ethena is essentially an open-ended hedge fund deploying the above strategy to earn yield and tokenizing their trading collateral as a stablecoin!

Using liquid staked ETH tokens as collateral, Ethena shorts an equivalent notional amount of ETH to create a portfolio with a delta of 0, a configuration that ensures that the net value of Ethena’s holdings fluctuates $0 for every $1 change in the underlying value of its assets, while collecting yield from ETH staking and the funding payments on its short positions.

Previous cap was filled, fast.

— Pendle (@pendle_fi) March 3, 2024

The @ethena_labs' flow continues.

USDe caps on Pendle have been raised to 200M. https://t.co/OOR3neqizY pic.twitter.com/7Gp8VxgQtm

Multiple protocols have previously employed similar strategies to Ethena, but prior iterations have struggled to scale due to a reliance on decentralized trading venues. Ethena circumvents this liquidity ceiling by tapping into centralized exchanges like Binance.

To protect users’ collateral, Ethena makes use of off-exchange settlement (OES) solutions that hold funds with reputable third-party custodians, with only the account balances mirrored into CEXs to provide trading margin, ensuring funds are never deposited to centralized exchanges.

Because staked ETH can be perfectly hedged with a short position of equivalent notional value, USDe can be minted at a 1:1 collateralization ratio, putting Ethena’s capital efficiency on par with that of dollar-asset backed stablecoins, like USDC and USDT, while circumventing the need to source assets from traditional financial markets that makes their issuers comply with meatspace regulations.

Although Ethena’s current model only uses staked ETH as collateral, the protocol may move to incorporate BTC as collateral to achieve even greater scale, but doing so could dilute the return profile of USDe as the BTC collateral would not generate staking yield.

Research recap below on the first two weeks of public mainnet: pic.twitter.com/9E1uoDVMwE

— Ethena Labs (@ethena_labs) March 1, 2024

📉 What’s Ethena’s Worst Case Scenario?

In crypto, financial rewards do not come without commensurate risks; participants in the Ethena Opportunity should not expect to find otherwise.

While juicy funding rates compounded on staking yield certainly make for attractive APYs, these returns are not generated free of risk…

Beyond the standard crypto risks that DeFi users have come to expect, Ethena comes with a few atypical risk vectors that have caused alarm and fueled comparisons with Terra/Luna algorithmic UST stablecoin.

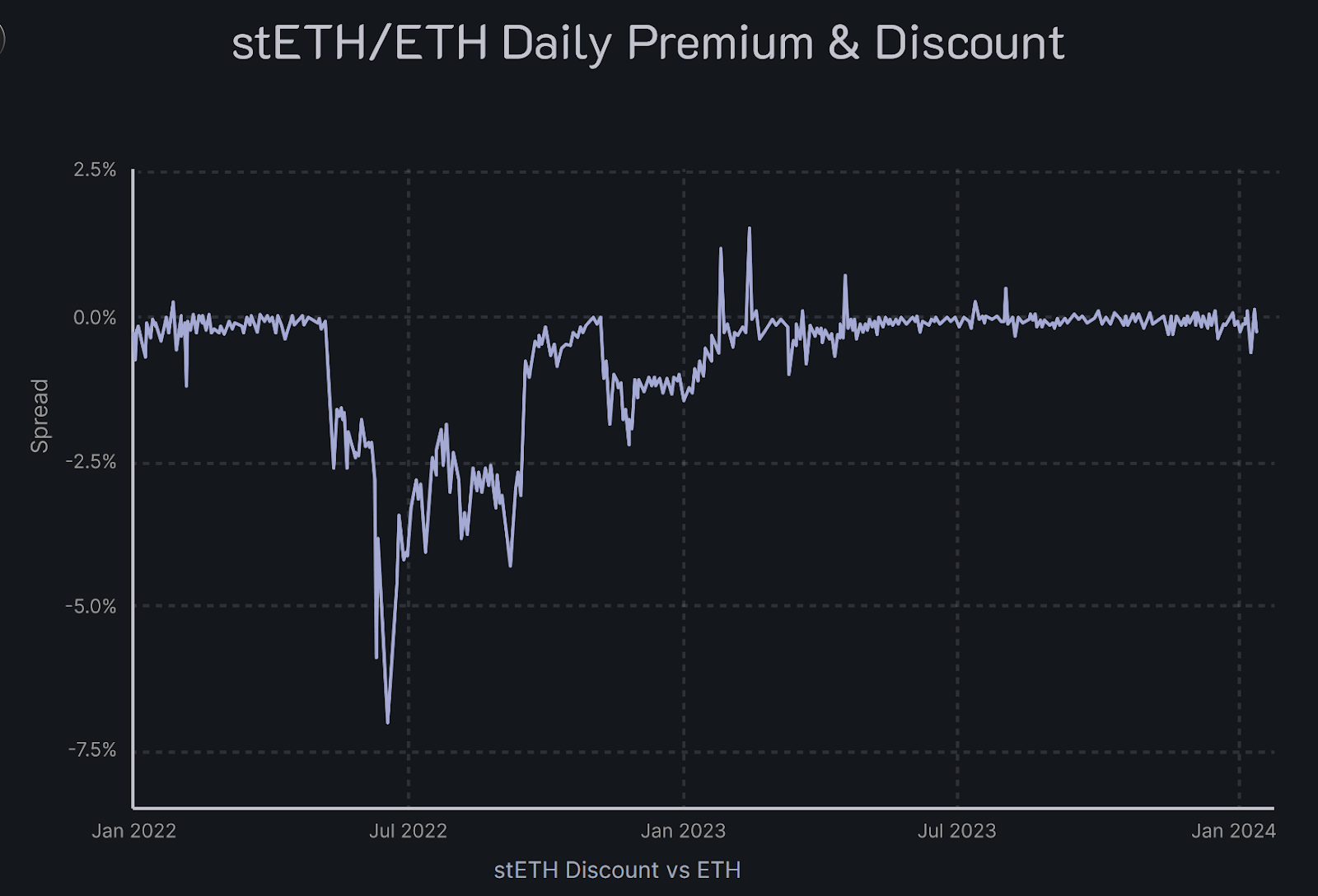

Collateral Depeg Risk

Ethena’s chief risk is its usage of LST collateral matched with vanilla Ether shorts. While this optimization to the ETH basis trade helps the protocol maximize its yield generational capabilities, it adds risk!

In the event Ethena’s LST collateral depegs from ETH, Ethena’s ETH shorts will not capture the fluctuation, leaving the protocol with losses on paper.

While LSTs typically trade close to their pegs, we’ve seen multiple scenarios where these tokens can depeg, such as the discount on Lido’s stETH reaching nearly 8% during the black swan liquidation of 3AC in mid-2022!

Shapella enabled Ethereum staking withdrawals in April 2023, making it possible that the 3AC liquidation may have created the widest depeg we’ll ever see from a blue chip LST, but the fact remains that any future depeg events will pressure Ethena’s margin requirements (the amount of funds it must have deployed to exchanges to hold its hedges open to avoid liquidation of its positions).

In the event that liquidation thresholds are reached, Ethena would be forced to realize a loss.

Funding Rate Risk

As spectacular as Ethena’s yields may appear from the outset, it is important to note that two protocols have previously tried to scale synthetic dollar stablecoins and have each failed due to yields inverting.

i dont get why so many people are focused on ethena's high yield (its a basis trade) instead of the fact that there's been 2 projects that tried this before and both gave up because they lost money due to yields inverting

— 0xngmi (@0xngmi) February 20, 2024

To combat negative yields from funding, Ethena uses staked ETH as collateral, a strategy that reduced the number of days USDe produced negative yields from 20.5% to 10.8% during backtests dating back three years.

While there is 100% certainty that funding rates will flip negative at some point, the natural state of the crypto market is contango, placing upward pressure on funding rates and providing a conducive environment for Ethena to conduct its basis trade.

Counterparty Risk

Many unfamiliar with Ethena’s design cite its deployment of user collateral to centralized exchanges as a major risk, but this has been greatly mitigated by usage of the aforementioned OES custody accounts.

While unsettled profit from a hedge on a bankrupt exchange could result in losses, Ethena settles PnL at least daily to reduce their capital exposure to exchanges.

If one of Ethena’s exchanges goes under, the protocol may be forced to use leverage against positions on other venues to neutralize their portfolio’s delta until settlement can occur on outstanding positions and the custodian of an affected OES account can release funds.

Further, should one of the custodians on Ethena’s OES accounts go bankrupt, access to funds may be delayed, necessitating the use of leverage on other accounts to hedge the portfolio.

Generic Crypto Risks

As is the case with many early stage crypto protocols, it is important to keep in mind that depositors to Ethena face the risk that the protocol’s team could rug its users funds, as ownership over the Project’s keys is not currently decentralized.

While the vast majority of crypto projects face a large amount of exploit risks with respect to potential vulnerabilities in their smart contracts, Ethena’s usage of OES custody accounts mitigates this risk vector by eliminating the need to use complex smart contract logic.

Takeaways

Ethena has protected their assets for the bankruptcy of their exchanges or custodians, putting in place contingency plans to neutralize the delta of their portfolio in the event that assets are frozen and unavailable for trading!

With many exchanges applying a 0% haircut to the value of stETH collateral and offering 50% maintenance margin requirement for accounts of Ethena’s size, the protocol can likely incur up to a 65% loss of the market value of its collateral before approaching liquidation!

Negative funding rates could lead towards yield compression, potentially causing TVL to bleed, but they alone would not cause an implosion of USDe; with maximum -100% annualized funding rates, the loss to Ethena’s notional is only 0.091% per 8 hour funding period!

To top it all off, Ethena also has an insurance fund that can be deployed to top off margin accounts to stave off liquidation, offset negative funding yields for a prolonged period of time, or act as the buyer of last resort for USDe on the open market!

While Ethena can absorb some degree of losses with the insurance fund, it is important to recall Murphy’s Law, which reminds us that anything that can go wrong will go wrong, and at the absolute worst time.

Imagine a situation where LSTs begin to depeg.

Centralized exchanges respond by lowering the collateral weight of liquid staked ETH tokens, reducing the maximum loss on the market value of collateral Ethena could incur before hitting liquidation.

Assuming the general market is also selling off during this period, funding rates would go negative, placing further pressure on Ethena’s collateral and pushing the protocol even closer towards liquidation and having to realize losses!

Ethena may not use leverage during the course of normal operations, but the unexpected bankruptcy of an exchange or custodian could temporarily freeze funds, necessitating its usage to neutralize portfolio delta.

A steepening discount combined with a levered account and reduced collateral weights on liquid staked ETH could theoretically put Ethena’s collateral within reach of liquidation.

With the basis trades now accessible to anyone in crypto, Ethena could easily balloon to billions of dollars under management, meaning liquidations of its massive portfolio of staked ETH could further suppress market values for LSTs, exacerbating Ethena’s paper losses and opening the floodgates for a death spiral to ensue!

Undoubtedly, the above series of events could only be the result of a catastrophic black swan event, but it is important to keep in mind all of the potential risks that you face when participating in crypto.

🪂 How To Get Started With Ethena?

As with any project on the frontier of crypto, Ethena comes with its risks, but for those early to the opportunity, participating could yield fantastic upside…

Whether you’re looking to earn the double digit APYs that sUSDe offers or want to farm Shards to maximize your potential Ethena airdrop allocation, there is no better place to begin your journey than the Bankless Airdrop Hunter!