Whop's Crypto Play

View in Browser

Sponsor: MegaETH — Crypto has new apps, finally.

- 🦄 Uniswap Foundation Projects 9 Months of Runway in Treasury Bombshell. The unaudited financials recorded $85.8M of total assets at year-end 2025, with revisions likely for Q1 2026 to include the impacts of UNIfication.

- 🟠 Strategy's STRC Perpetual Holds Above Key $100 Threshold. Another Strategy BTC buy is likely already underway, with confirmation expected in next Monday’s announcement.

- 💸 Citadel Securities-Backed Crypto Exchange Applies for National Trust Bank Charter. Citadel's "EDX Markets" is vying to become crypto’s next regulated powerhouse.

| Prices as of 1:30pm ET | 24hr | 7d |

|

Crypto $2.37T | ↗ 1.3% | ↘ 2.0% |

|

BTC $68,515 | ↗ 0.3% | ↘ 3.6% |

|

ETH $2,141 | ↗ 1.6% | ↘ 1.4% |

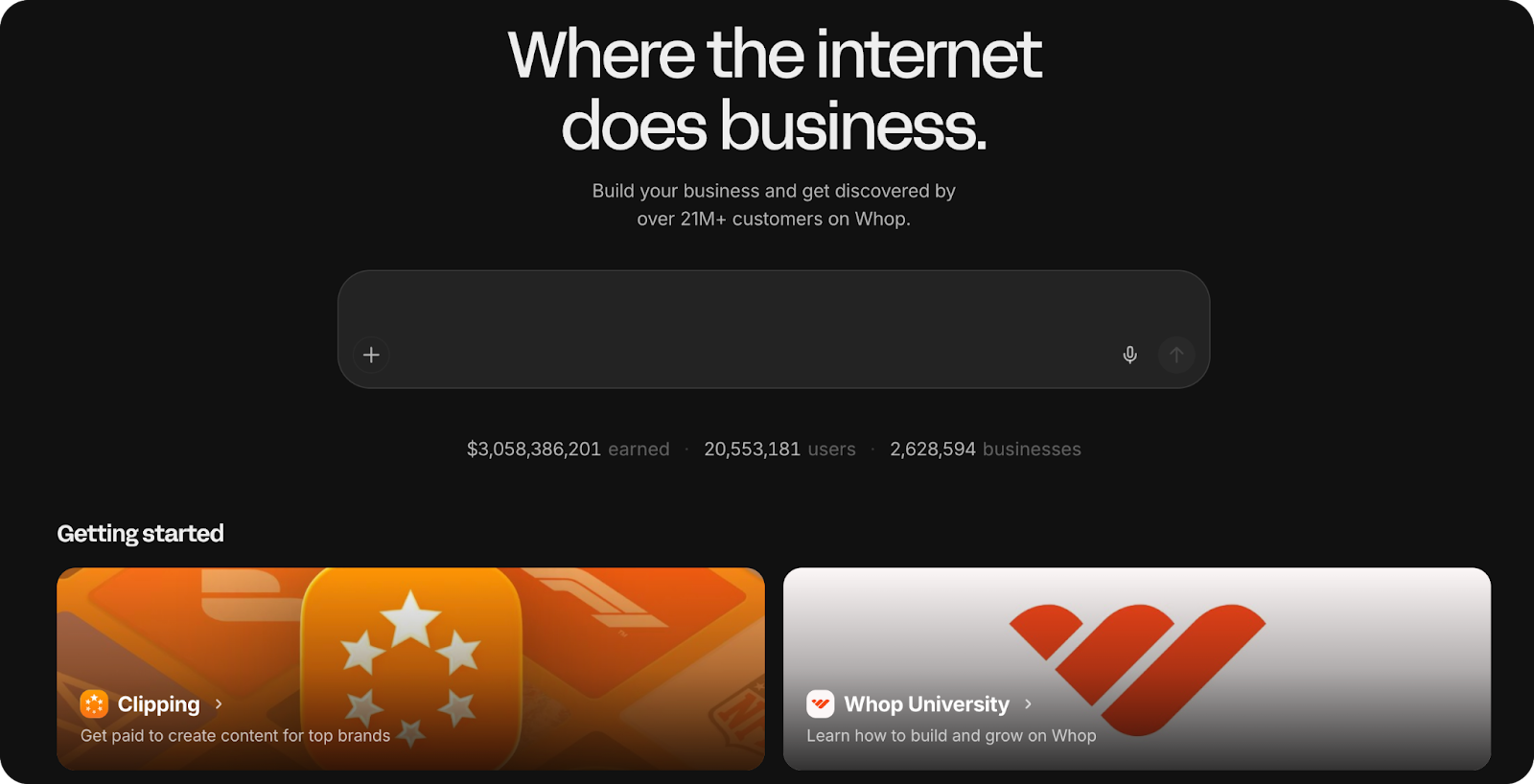

A name floating around Crypto Twitter that, at first glance, feels slightly out of place is Whop.

Whop is an online marketplace for digital entrepreneurship: while not "crypto-native," Whop operates in the same cultural air given what activities are most prominently featured: ways to make money quickly, exploit short-lived edges, arbitrage attention, or package know-how into subscriptions. This is the same emotional register as the more mercenary corners of crypto speculation that have appeared in recent years (trading bots, "paid" groups, etc.). Digital products optimized around speed, leverage, and asymmetric upside.

Founded in 2021, Whop has scaled rapidly since its launch. Last year alone, it claims, the platform’s users earned about $3 billion, across a reported 18.4 million accounts, with transaction volume increasing about 25% month-over-month.

The Marketplace Layer

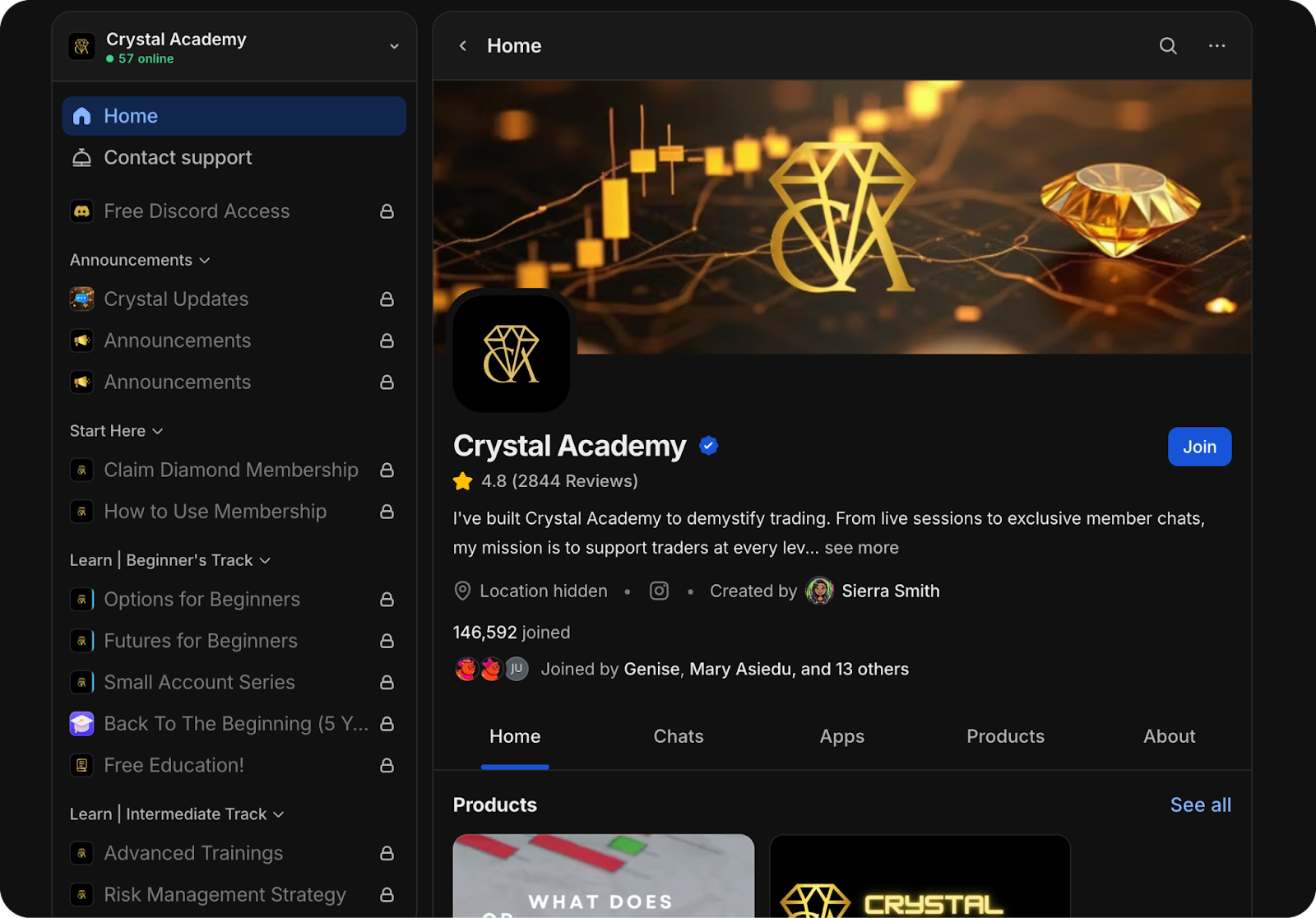

At the surface, Whop is a hosted marketplace and storefront system that lets creators and online businesses sell digital products and memberships. Creators get a customizable profile, or "Whop," that functions as both storefront and hub. Inside it are modular tools for chats, courses, livestreams, gated communities, and content delivery, along with growth tooling like affiliates, promotions, and analytics.

Whop also runs its own storefronts, like WhopAI which serves as a destination for discussing the platform's internal agents that have been built to help creators accomplish tasks like building out business plans or apps for their pages. For those looking to get started, the homepage sports two on-ramps:

- Whop University, a self-paced training hub that teaches creators how to set up storefronts, price products, and scale distribution.

- A paid content campaign product that lets users create user-generated content (UGC) clips, post them to social platforms, and get paid per thousand views.

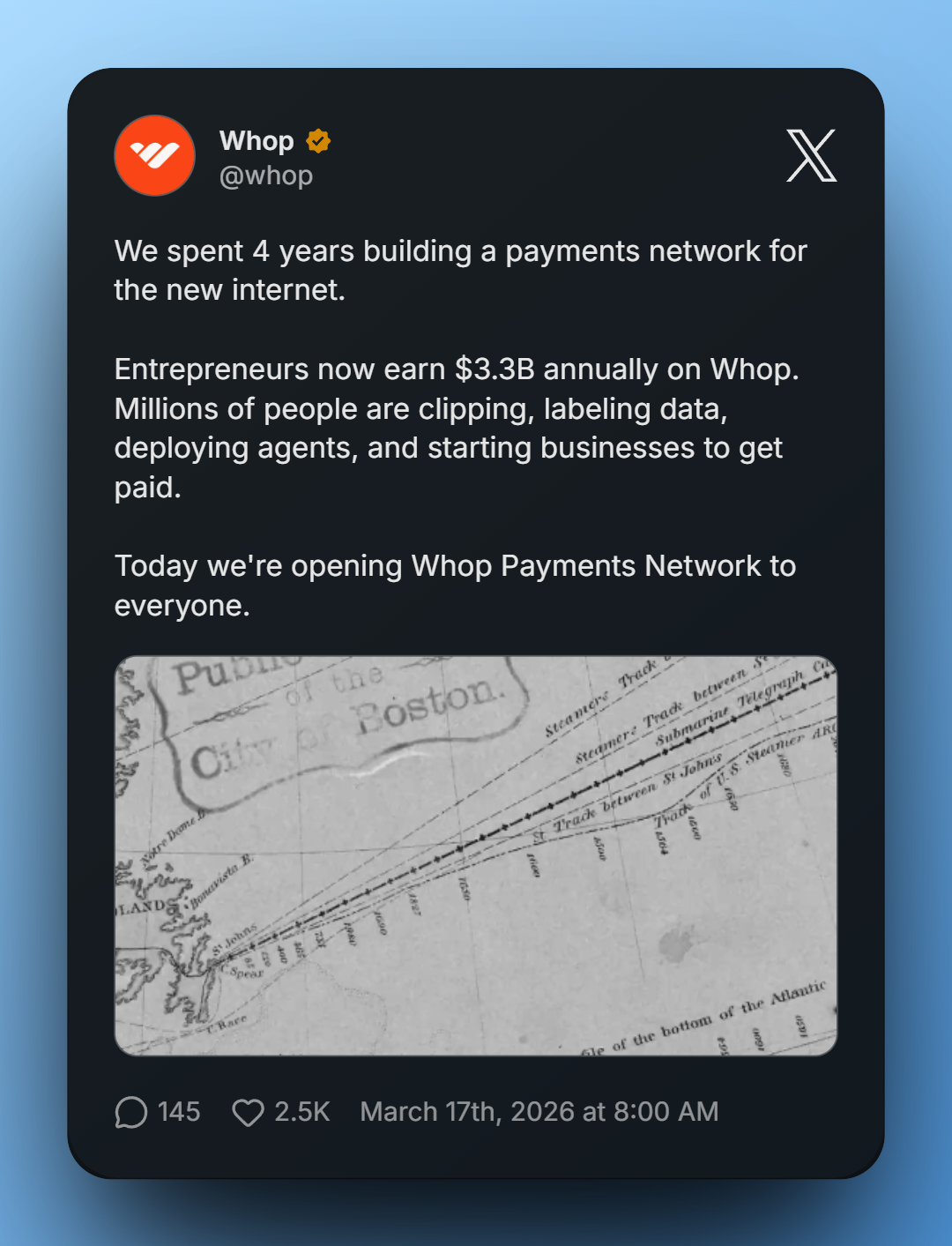

The Payments Network

Underneath the marketplace sits the Whop Payments Network, which is where the company morphs into a fintech. Instead of creators and their platforms stitching together checkout, payouts, subscriptions, taxes, affiliates, and compliance across multiple vendors, they can plug into Whop.

One standout feature is payment orchestration. In practice, most online platforms rely on a single payment provider. When a payment fails, because of false fraud flags, cross-border issues, or expired cards, that sale is just lost. Payment orchestration changes this by routing each transaction to the provider most likely to approve it, and retrying failed payments automatically before the customer drops off.

More broadly, the Payments Network lets Whop extend beyond its own marketplace. Creators who "outgrow" Whop, or want to sell directly on their own sites, can still use this underlying payments infrastructure. It's a smart play for Whop to embed itself into the broader creator economy as infrastructure.

Treasury: The Post-Revenue Layer

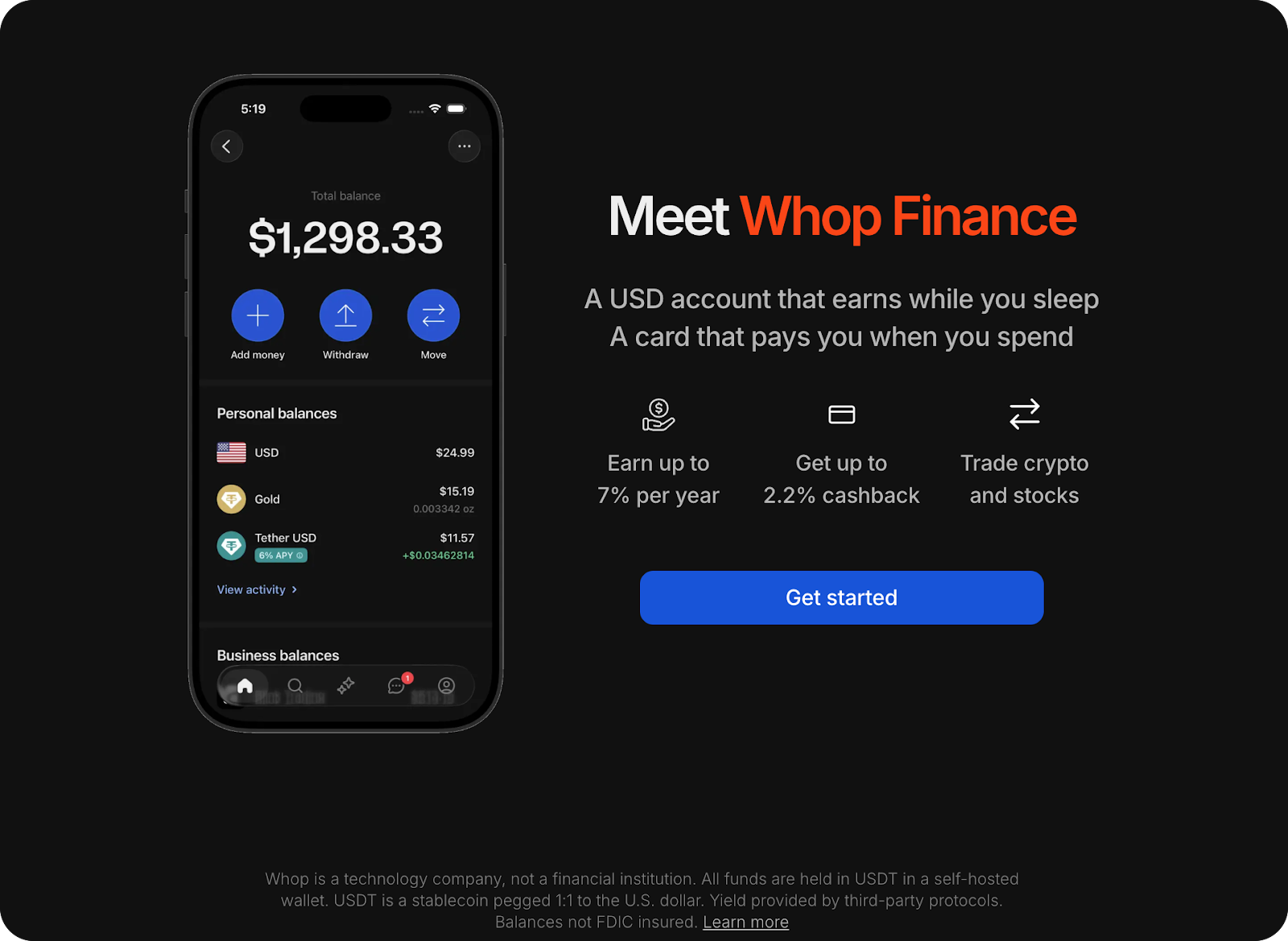

Last week, following a $200 million investment from stablecoin giant Tether a few months back, Whop launched Treasury, a savings layer boasting up to 6% returns for which the platform ventures onchain.

Treasury is an opt-in yield layer that allocates idle balances into onchain strategies. When enabled, users can convert their earnings into USDT, which are then routed to yield-generating protocols. In their announcement post, Whop says Treasury is the first product of Whop Finance, a broader financial toolkit that hints at a card and tools for trading crypto and stocks.

Notably, Treasury isn't FDIC-backed, though it could implement an insurance policy like the one Aave's app intends to launch with. Overall, Treasury sets the stage for Whop to effectively act as a bank to their users, providing high-yield savings now with additional features slated for down the road.

The Demographic Convergence

When you take a bird's-eye view of Tether's portfolio, a distinct profile emerges.

Tether's portfolio includes Rumble, the video platform that has become a destination for fringe, predominantly right-wing content. Meanwhile, Whop provides payment rails for platforms like Kled, which pays users for training data, and Ohana, where people sublease their apartments while digital nomading.

All these companies serve users who want to operate outside traditional systems. Crypto fits perfectly here. Whop sits at the center of this economy. Kled, Ohana, Rumble – all serve the same general user. Tether has clearly identified that market, one with a similar profile as their own company, and is now providing the tooling to make it scale.

The Tension and the Future

What makes Whop interesting for crypto is that it helps crystallize one of the key demographics for which crypto proves vital.

Previous crypto attempts at creator monetization – creator coins, social tokens, NFT membership passes – have largely failed because they started with crypto-native concepts and hoped creators would adapt to them. Whop starts with what “digital entrepreneurs” are actually doing in 2026 – selling courses, running communities, arbitraging attention – and applies crypto as the backend to serve a class of workers that traditional financial infrastructure was never designed to.

Whop's marketplace model is low-barrier by design, which means it also lowers the barrier to grift. Day-trading bots, life-upgrade subscriptions, and guru courses of questionable value have a natural home on Whop, and critics have noticed. There are a number of complaints filed with the Better Business Bureau (BBB) as well as Reddit threads which detail fraud by sellers. ZachXBT even took to Twitter recently, saying: "Whop needs to stop associating with all of the biggest paid group, course, and e-commerce guru grifters."

For users already comfortable operating in high-velocity, loosely-moderated digital environments – in other words, crypto – that tension may matter less than whether the infrastructure works. Regardless of Whop's rough edges, what's clear when examining the platform is a distinct class of digital worker who needs financial infrastructure that moves as fast as they do has emerged, and for that, crypto presents itself as the natural fit.

We're past "in it for the tech" or "in it for the money." MegaETH is bringing you products worth using, powered by USDM.

Not financial or tax advice. This newsletter is strictly educational and is not investment advice or a solicitation to buy or sell any assets or to make any financial decisions. This newsletter is not tax advice. Talk to your accountant. Do your own research.

Disclosure. From time-to-time I may add links in this newsletter to products I use. I may receive commission if you make a purchase through one of these links. Additionally, the Bankless writers hold crypto assets. See our investment disclosures here.