Turning Losses into Gains ($)

View in Browser

Sponsor: MetaMask - Spend crypto anywhere online and AFK with MetaMask Card.

- 🇺🇸 Senate Banking Committee Advances Crypto CLARITY Act. Ethical concerns regarding Donald Trump’s multibillion-dollar crypto empire continue to loom large among Democrats, threatening to stall the bill’s path through Congress.

- 👯♀️ Hyperliquid Shifts Stablecoin Strategy Back Toward USDC. After last year’s messy split from USDC, Hyperliquid is reconnecting with old friends as Coinbase and Circle return to the center of its trading ecosystem.

- 🐙 Kraken Abandons LayerZero Bridge, Switches to Chainlink. kBTC joins a growing list of crypto assets that have abandoned LayerZero in favor of alternative interop solutions.

| Prices as of 5pm ET | 24hr | 7d |

|

Crypto $2.70T | ↗ 2.3% | ↗ 1.6% |

|

BTC $81,480 | ↗ 2.6% | ↗ 2.0% |

|

ETH $2,291 | ↗ 1.8% | ↗ 0.2% |

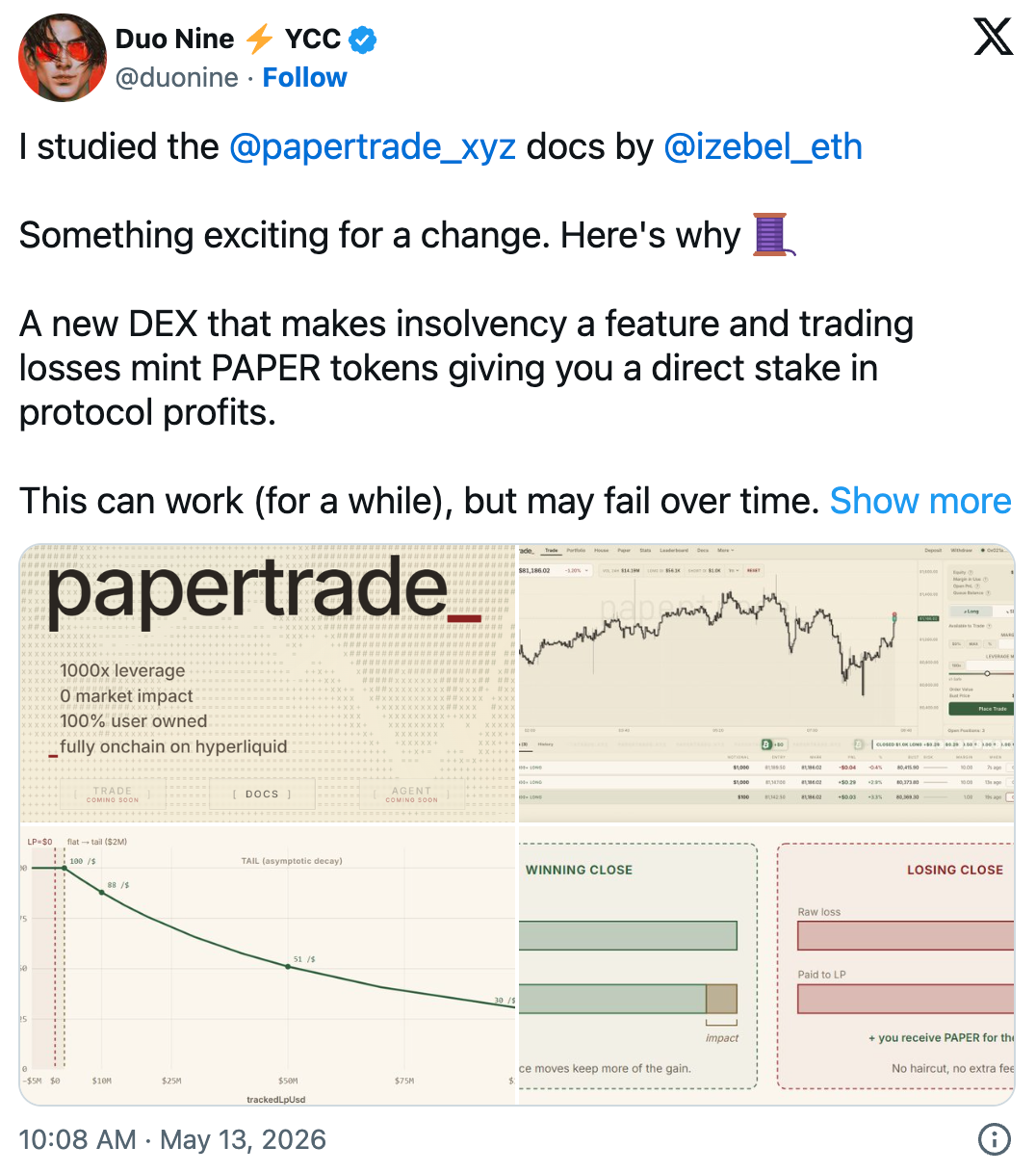

Most DeFi protocols only reward profitable traders.

Papertrade flips the model entirely, rewarding its users for losing. The result is one of the most unconventional, reflexive, and undeniably innovative mechanisms for onchain trading that the crypto industry has seen in years.

What is Papertrade?

Developed by pseudonymous X user @izebel_eth, Papertrade is an upcoming fully on-chain perpetual futures exchange built on Hyperliquid via HyperEVM. The protocol promises traders:

- Up to 1000x leverage

- Zero slippage

- No funding rates

- No fees to open positions

- No gas costs passed to users

On the surface, it looks like another hyper-leveraged perp venue designed for degens, but underneath sits one of the strangest and most novel tokenomic experiments DeFi has produced in years.

Losing Is the Product

What truly sets Papertrade apart is the design of its native PAPER token.

PAPER functions as a loss rebate token. It is distributed to traders the moment they realize a loss, whether by closing a position underwater or through liquidation. These tokens serve as a consolation claim on the protocol’s future value and can be staked to earn a proportional share of protocol revenue, which is continuously distributed in USDC.

According to Papertrade’s documentation, PAPER will be fairly launched, starting from a supply of zero with neither pre-mint, nor team allocation, nor VC allocation, nor airdrop, nor vesting schedule.

When traders on Papertrade close their position at a loss or are liquidated – the two actions that generate PAPER tokens – their forfeited funds flow directly to the protocol’s liquidity pool (LP). This LP is used to pay out the positions of profitable traders, with a small LP revenue share fee applied to winning positions that is redistributed among PAPER stakers.

Once the LP exceeds $5M, every dollar lost by traders (in addition to the LP revenue share fee) is owed to PAPER stakers, effectively soft-capping the liquidity pool beyond this value while allowing unclaimed funds to continue accruing within the LP contract.

In the event that the funds stored within the LP are insufficient to pay out a profitable trader's position (i.e., the LP is insolvent), winnings of profitable traders will be queued on a first-in-first-out (FIFO) basis, and paid out as funds become available from other users’ losses.

There are no external counterparties on Papertrade. Instead, all trades are executed as synthetic swaps against the LP, which uses the Best Bid/Offer (BBO) – the median between the highest bid and lowest offer – for a crypto asset on Hyperliquid’s order book at a specific moment in time to price contracts.

Even if no trades on Hyperliquid are actually executed at this price, the synthetically derived midpoint is still used to determine a trader’s entry price and later calculate PnL upon exit.

Optimal Strategies

With Papertrade, it will quite literally pay to be early...

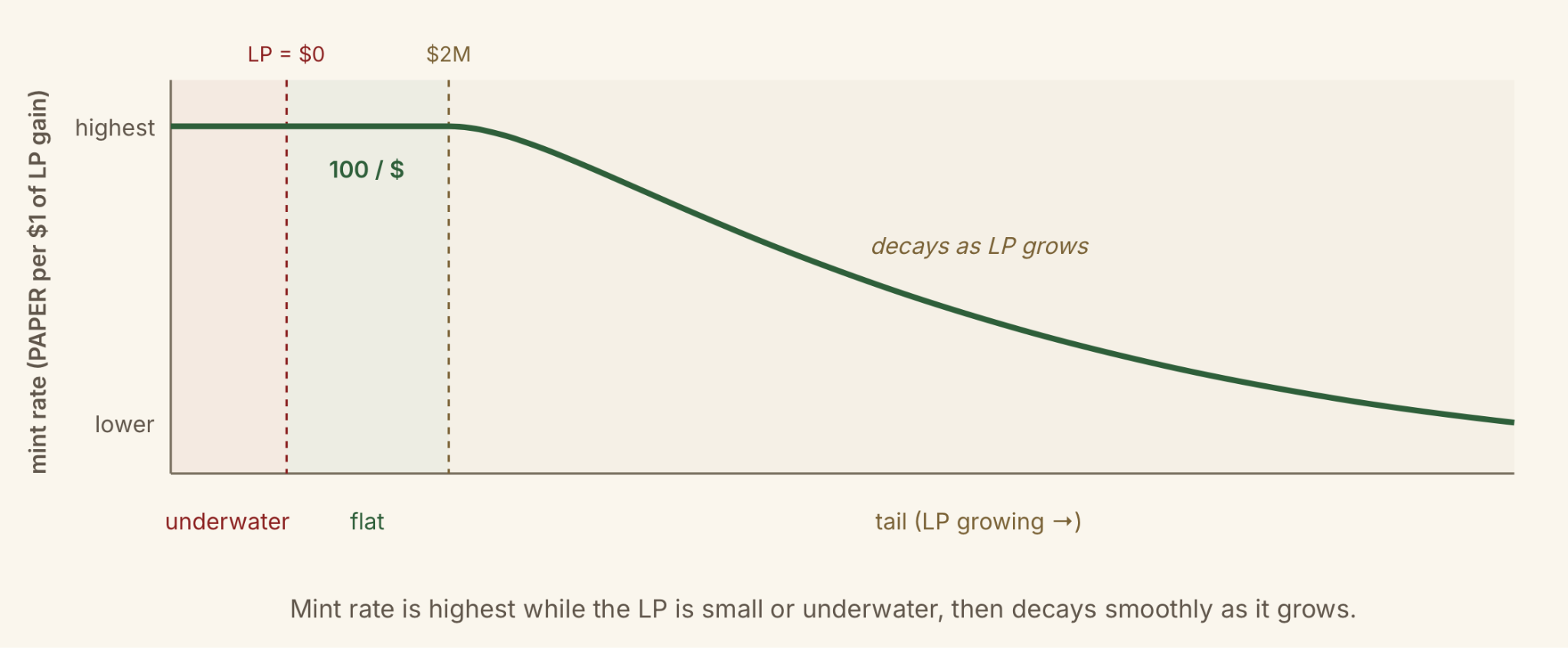

PAPER’s emission schedule is designed to heavily favor the very earliest of protocol participants, with 100 tokens emitted for every dollar of trader losses when the value of the LP is less than $2M. Once the LP surpasses this threshold, the rate of emission will decay asymptotically, or steadily approach zero as accumulated LP gains grow toward infinity.

Additionally, although the PAPER emission schedule remains fixed, regardless of how long Papertrade has been live, earlier PAPER holders will momentarily receive a larger proportional ownership stake in the token supply, entitling them to a greater share of protocol fees and potentially increasing the intrinsic value of their tokens.

From a game theory perspective, Papertrade creates a perverse incentive for users to maximize leverage and intentionally lose trades during the protocol’s earliest stages in order to accumulate as much PAPER as possible.

While deliberately lighting money on fire is rarely advisable, the core appeal of Papertrade is arguably not trading itself, but the acquisition of loss rebate tokens. After all, traders seeking pure execution quality or sustainable profitability already have access to numerous perpetual trading venues with more conventional/safer market structures.

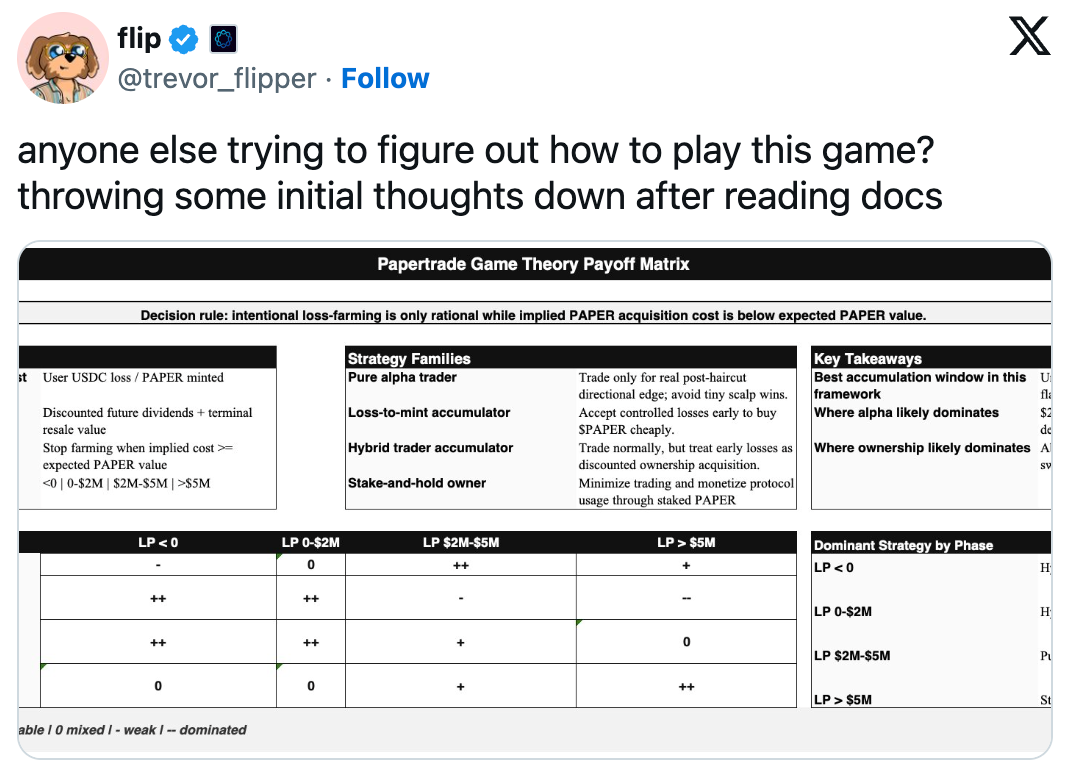

A payoff matrix constructed by Delphi Digital researcher @trevor_flipper illustrates this dynamic well. When LP value remains below $2M, taking large losses appears to generate the highest expected payoff through PAPER accumulation. Beyond that threshold, trading with an actual edge becomes the dominant strategy, with PAPER staking becoming the most lucrative play once the LP value surpasses $5M.

Risk Considerations

Of course, this entire mechanism could also implode spectacularly, with the most obvious concerns centering around oracle and pricing manipulation.

As Papertrade derives contract pricing from Hyperliquid’s BBO midpoint, rather than requiring actual execution liquidity, attackers who are able to successfully manipulate the order book even momentarily can extract value from the LP.

While the impacts of smaller price distortions are partially mitigated by the fee share applied to profitable trades and redistributed to PAPER stakers, a sufficiently violent blowout in Hyperliquid’s order book could be sufficient to drain the LP entirely.

Additionally, even in the absence of an exploit, sustained net profitability among traders could push the LP deep into insolvency, causing unpaid claims to accumulate. As confidence in the protocol’s ability to honor winning positions deteriorates, the expectation of realizing profits on winning trades may fade altogether, undermining the fundamental reason to use a trading platform in the first place.

Innovative Design

Whether it succeeds immensely or fails catastrophically, Papertrade introduces one of the first genuinely new market structures crypto has seen in years, transforming trader losses into ownership, converting liquidation pain into yield-bearing exposure, and creating a bizarre incentive system where losing early may actually be the optimal strategy.

That does not make it safe.

It does not make it sustainable.

But it does make it interesting.

And in an industry increasingly dominated by copy-paste applications and recycled token models, genuinely new ideas deserve attention.

Spend crypto online or IRL directly from your crypto wallet at over 150 million merchants worldwide—anywhere Mastercard is accepted. This is how you offramp: 3% cashback, zero foreign transaction fees, and exclusive benefits. Keep full custody of your funds until the moment you pay. Get the MetaMask Virtual Card now, free.

Market Plays:

- 🦍 Longing on Leverage Sir

- 🟠 LPing strkBTC on Ekubo

- 🚀 Trading $SPACEX on Lighter

- ➿ Looping $USDe on Jupiter Lend

- 🪂 Depositing to Glider’s Coinbase Portfolio

Hot Reads:

- 🧱 The Case for Modular Security — Nam Chu Hoai

- 🌄 Sky: Stablecoins, Credit, and Yield — Carlos Gonzalez Campo

- 🔮 The Opportunities for Innovators We’re Seeing — Ethereal Ventures

- 🔗 Distributed vs. Represented: A Cleaner RWA Lens — Nick Sawinyh

- 💵 What the Dollar Knows That the Market Forgot About ETH — William Mougayar

Farming Opps:

- 🟠 BTC: 8% APR with Ekubo’s LBTC-WBTC pool on Starknet

- 🟠 BTC: 2% APR with Vesu’s WBTC vault on Starknet

- 🔵 ETH: 4% APR with Convex’s WETH-weETH vault on Ethereum

- 🔵 ETH: 3% APY with Pendle’s wstETH PT on Arbitrum

- 🟢 USD: 10% APR with Uniswap’s USDC-RLUSD pool on Ethereum

- 🟢 USD: 6% APR with Convex’s RLUSD-USDC vault on Ethereum

Airdrop Hunts:

- 🌐 World Markets: Hunt World Markets airdrop

- 📜 Papertrade: Prepare for Papertrade launch

- ✨ Space: Claim SPC airdrop

- 🤖 USDai: Claim CHIP allocation

- 🫦 Fluent: Claim BLEND airdrop

Anthropic's secondary market is tens of billions of dollars deep, stacked with SPVs on top of SPVs charging 10% fees plus carry, and almost entirely opaque.

Dio Casares of Patagon breaks down how it actually works: which deals Anthropic blesses and which get cease-and-desists, why fake share certificates show up in 10-20% of executed deals, what tokenized equities and pre-IPO perps actually represent, and the mess of lawsuits and stuck shares coming when Anthropic finally IPOs.

Watch the full episode 👇

Not financial or tax advice. This newsletter is strictly educational and is not investment advice or a solicitation to buy or sell any assets or to make any financial decisions. This newsletter is not tax advice. Talk to your accountant. Do your own research.

Disclosure. From time-to-time I may add links in this newsletter to products I use. I may receive commission if you make a purchase through one of these links. Additionally, the Bankless writers hold crypto assets. See our investment disclosures here.