From Chaos to Clarity: How Trump’s SEC Pick Could Reshape Crypto Regulation

President-elect Donald Trump stole the crypto industry’s heart with promises to end the Biden Administration’s anti-crypto crusade and “fire” SEC Chair Gary Gensler on day one.

While Trump has yet to propose a Gensler replacement and his ability to relieve sitting SEC commissioners appears legally dubious, crypto participants are nonetheless ecstatic about prospects that a new SEC chair will soon alleviate one of the industry’s greatest regulatory pain points.

Commissioners Hester Peirce and Mark Uyeda may have already removed themselves from contention for the chair, but they have been outspoken advocates for digital asset liberties and regulatory restraint throughout their tenures at the SEC.

Today, we explore Commissioner Pierce and Uyeda's official statements in hopes of gleaning insight into what a hypothetical pro-crypto Securities and Exchange Commission might look like under the Trump Administration. 👇

🚢 Proposed Token Safe Harbor

One day prior to the confirmation of Gary Gensler as SEC chair in April 2021, Commissioner Peirce had digital assets on her mind.

Recognizing that a new SEC chair would come with a new agenda of enforcement priorities, Commissioner Peirce attempted to steer the conversation toward how securities regulations could be crafted to accommodate blockchain-based tokens by releasing an updated token safe harbor proposal via GitHub.

Peirce's refreshed proposal sought to provide decentralized application developers with a three-year exemption, or safe harbor, from federal securities registration. It incorporated substantial revisions that the crypto community, securities lawyers, and members of the public had provided as feedback on her previous draft from February 2020.

Safe harbor 2.0 is up. Thanks for all the comments on version 1. Looking forward to your feedback on this version: https://t.co/aRYPKAjutQ

— Hester Peirce (@HesterPeirce) April 13, 2021

Under the Trump Administration, a pro-crypto SEC can be expected to prioritize the deliverance of crypto clarity while actively soliciting industry feedback to craft regulations that balance the needs of burgeoning decentralized applications with the agency’s imperative to protect the investing public.

🖼️ Non-Fungible Folly

“Stoner Cats” is a collection of 10,320 NFTs that minted out for $8.2M ETH in July 2021; proceeds of this sale went towards funding the production of an animated series – also dubbed Stoner Cats – which featured Hollywood stars including Mila Kunis, Ashton Kutcher and Chris Rock. In exchange for their purchase, holders of Stoner Cats NFTs were promised exclusive access to the series, unspecified future entertainment content, and an online community.

While the SEC eventually settled with the entity behind Stoner Cats for conducting an unregistered security offering, Commissioner Peirce and lone fellow Republican SEC Commissioner Mark Uyeda dissented from this enforcement action.

Although they acknowledged that NFT creators should not receive a free pass from securities regulations, Commissioners Peirce and Uyeda contended the SEC’s application of securities regulations in this case merely contributed to legal ambiguity that would make it difficult for creators to distribute and monetize their content.

Wow! SEC commissioners Peirce and Uyeda just released a statement saying they DISAGREE with the SEC's actions against Stoner Cats nfts

— okHOTSHOT (@NFTherder) September 13, 2023

Comparing nfts to 1970s Star Wars collectables, and stating the need to protect artists' ability to create without excessive legal constraints🤯 pic.twitter.com/w7xOCI0grv

Under the Trump Administration, a pro-crypto SEC can be expected to produce comprehensive guidelines for how security regulations apply to NFTs; in the place of uncertainty about the legal status of a hypothetical tokenized Pokémon card should come clarity on when digital assets are exempt from securities regulations.

🪙 Token Tensions

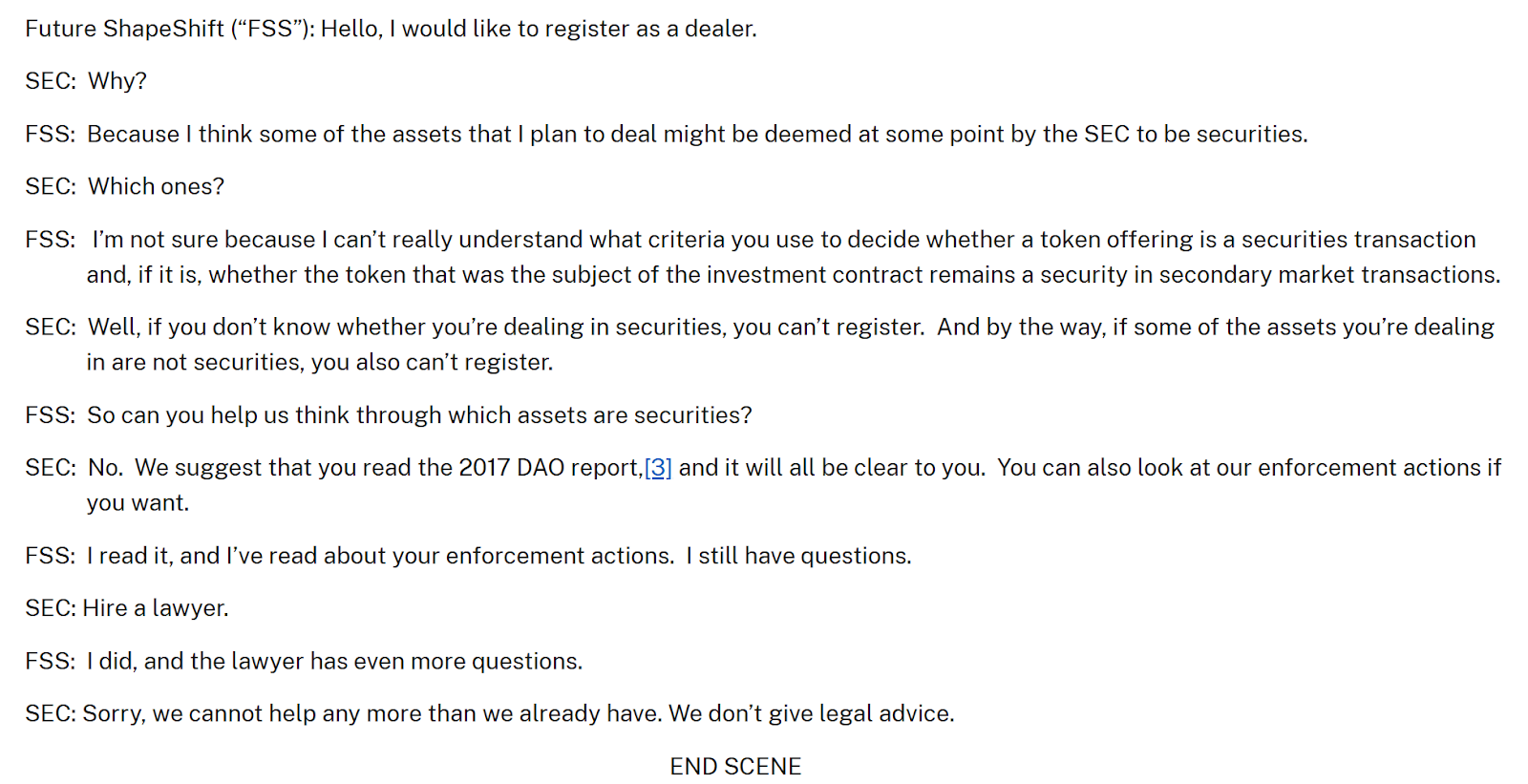

In its most recent display of an outwardly contested enforcement action against a crypto company, this March, the SEC settled charges against crypto exchange ShapeShift for behaving as an unregistered securities dealer in connection with the operation of its online crypto asset trading platform.

Despite becoming a peer-to-peer decentralized exchange in 2021, for more than six years, ShapeShift had acted as a broker intermediary, fulfilling orders from inventory and serving as counterparty for all crypto transactions that occurred on its platform.

Although Commissioners Peirce and Uyeda did not challenge assertions that ShapeShift had operated as an unregistered securities dealer prior to 2021, in yet another joint dissent, they voiced concern for ambiguity seeded by the SEC’s enforcement action.

To qualify as an unregistered securities dealer, ShapeShift must have facilitated the sale of securities. The SEC’s unwillingness (or inability) to identify the securities at issue or how their sale created an investment contract creates an untenable environment for the secondary trading of crypto assets.

Under the Trump Administration, a pro-crypto SEC can be expected to provide clarity around which tokens qualify as securities, eliminating threats of nebulous wrongdoing faced by crypto-native exchanges like Coinbase while simultaneously green lighting registered securities dealers to list such assets alongside existing offerings.

🧐 Looming Questions

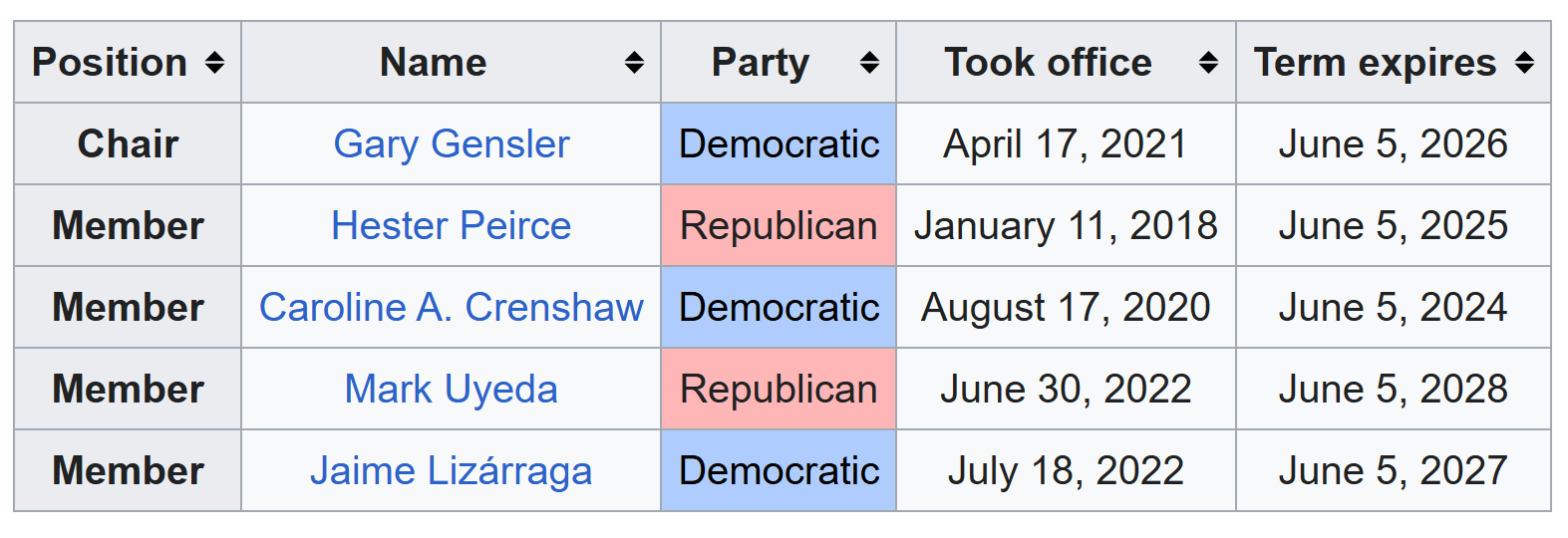

Decades of precedent suggest that Chair Gensler will resign and cede control over the SEC to a Trump appointee, but his term does not expire until 2026 and it is entirely unclear whether President Trump can forcibly remove Chair Gensler before then without protracted litigation.

It is worth noting, however, that many within the crypto industry have interpreted a recent Gensler speech from November 14, in which the Chair remarked, "It's been a great honor to serve," as an unofficial resignation notice.

ok Gary Gensler just gave a speech that sounds an awful lot like a farewell address

— RYAN SΞAN ADAMS - rsa.eth 🦄 (@RyanSAdams) November 14, 2024

phrases like "It’s been a great honor to serve" usually mean one thing

is he about to resign? pic.twitter.com/w5JAOyYepX

As an independent regulatory agency, the SEC enjoys significant autonomy from the executive branch, and despite Trump’s bombastic pledge to fire Chair Gensler on day one, murky case law may support the notion that SEC commissioners can only be relieved “with cause,” not simply fired “at will.”

Although the SEC’s chair wields discretion over the agency’s budget and oversees its staff, they require majority consent from the Commission to appoint administrative unit heads, and each commissioner receives an equal say in agency proceeding votes that direct how the SEC interprets and enforces securities legislation.

Commissioners are appointed by the President of the United States into rolling five-year terms but must be confirmed by a Senate majority. Term expirations are staggered to ensure that one member can be relieved on June 5 every year, and while commissioners may serve an additional 18 months beyond their term expiration date to prevent a vacancy, at no time can more than three of the five commissioners belong to the same political party.

While Commissioner Crenshaw’s term expired on June 5 of this year, she continues to serve at the SEC and has been re-nominated by President Biden to fill the resulting vacancy.

Should this vacancy persist until President Trump’s inauguration, he can easily fill the position in a Republican Senate with a candidate of his choosing to solidify a seemingly pro-crypto majority within the SEC. Unfortunately, the present Democrat-controlled Senate still has ample time to confirm Crenshaw for an additional 5-year term, and the Biden Administration can always resort to a sneaky recess appointment following the Senate’s adjournment on December 20.

Even in the absence of Gensler’s resignation and assuming Crenshaw is confirmed for a renewed term, President Trump can still impose his might on the SEC by designating either an unwilling Peirce or Uyeda as acting chair.

While no clarifying rulemaking activities could occur in this scenario, the Acting Chair gains control over SEC Staff, providing them authority to rescind controversial SEC Staff Accounting Bulletin 121, entertain requests for no-action letters, pause or terminate ongoing enforcement investigations and litigation, and solicit public feedback as the first step for future crypto rulemaking procedures.