Ethena dominated DeFi mindshare throughout 2024, and despite its synthetic dollars garnering plenty of criticism and concern upon launch, the team's efforts have become one of DeFi's most notable success stories this year as traders have flocked to the protocol.

There are signals that the basis trade tokenization play is just getting started as other DeFi players look to latch onto Ethena's growth prospects.

In recent months, market froth has turbocharged Ethena revenues and transformed ENA into a top-performing crypto play, meanwhile, crypto credit providers have come to increasingly integrate USDe in their reach for yield.

Today, we explore Ethena’s 2024 success story 👇

🪙 An Explosive Rise

Ethena accepted its first public deposits on February 19, and within one month of mainnet, USDe’s circulating supply had flipped those of all but 5 stablecoin competitors.

Thanks to its sizable airdrop incentives and a well-timed launch into the hottest funding rate environment seen all year, USDe supply expanded unchecked to $2.39B until mid-April before stalling out on waning ENA airdrop excitement and cooling crypto market conditions.

Although Ethena’s subsequent May 16 decision to reduce the insurance fund take rate temporarily reinvigorated USDe and resulted in a one-month 50% supply expansion, continued funding rate compression throughout the third quarter took its toll. By September, this USDe supply bump had reverted in its entirety and ENA price was down 86% off its post-launch highs.

While the funding rate arbitrage strategies employed by Ethena have already long been possible for any trader with futures familiarity, the issue has been that funds collateralizing these trades have to be locked on the exchange (whether in CeFi or DeFi), leaving them unable to be re-pledged elsewhere.

With Ethena's approach, this basis trade position itself becomes “tokenized” and is represented as USDe, allowing traders to earn additional yield in DeFi or borrow against their holdings.

Despite some initial hesitance from third-party apps to incorporate (s)USDe collateral at a rapid clip, Ethena’s synthetic dollars now dominate crypto credit markets due to simple yield economics.

Yield providers that fail to compete against Ethena’s market-leading returns risk reduced deposits or excessive borrowing demand. This dangerous dynamic can spike algorithmically set borrowing rates well above market value and compelled numerous DeFi lending markets to frantically onboard billions of dollars of USDe derivative collateral when funding rates exploded yet again in November.

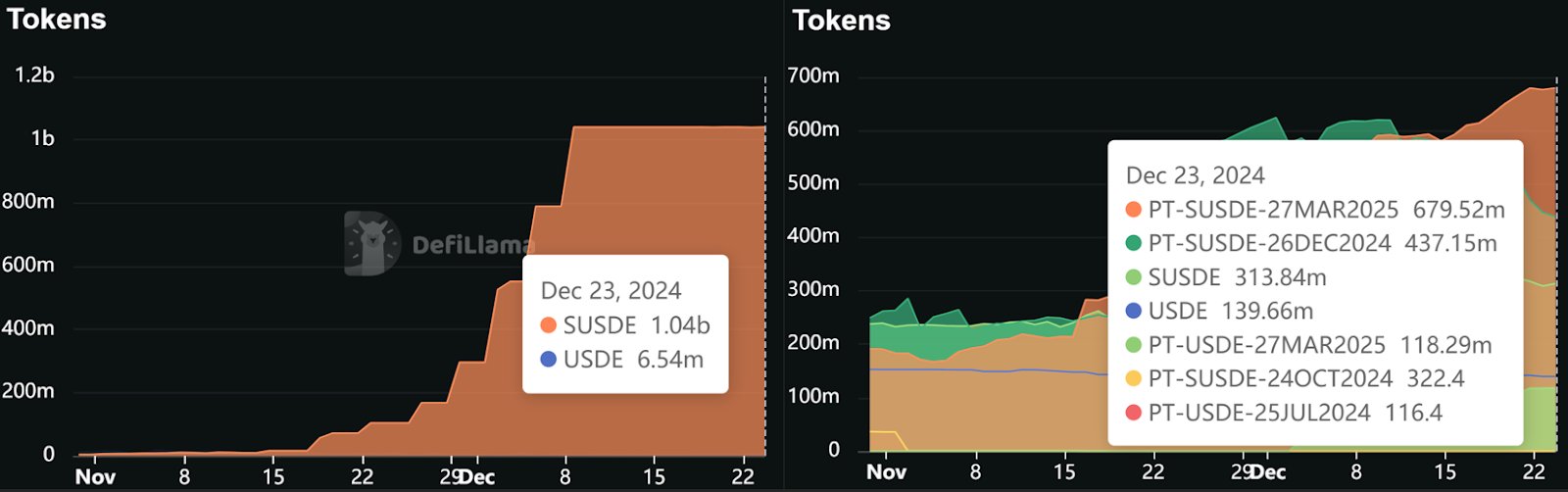

In just a few weeks, Aave sUSDe deposit caps exploded to $1B (its lending markets held a meager $20M of Ethena collateral at the start of November). At the same time, MakerDAO and other lenders on Morpho were swelling to absorb $1.2B in extremely illiquid Pendle sUSDe principal token (PT) exposure at extremely high 91.5% maximum leverage ratios.

🧐 Unrivaled Asset?

Ethena assets are now intertwined with bluechip DeFi, and ENA has relished in that fact, staging an impressive 500%+ resurgence off its September lows to settle within striking distance of post-launch highs.

Although negative funding rate environments are a known risk that could cause USDe to incur losses, many crypto observers are optimistic that Ethena’s recently deployed US Treasury product (USDtb) could become a suitable basis trade alternative that establishes a yield floor for Ethena depositors.

Prediction: USDtb will be the largest on-chain tokenised treasury product within 1 month of launch

— José Maria Macedo (@ZeMariaMacedo) December 16, 2024

This is huge for Ethena, not just because it gives them a "lower-risk" yield-bearing stablecoin product, but also for USDe itself

Whenever funding rates < treasury rates, Ethena… https://t.co/wBD11tdHEE

All that said, funding rates are inherently volatile and there is plenty of uncertainty around how Ethena would appropriately navigate a prolonged negative funding rate scenario. In the event losses must be realized to convert existing synthetic dollar exposure into treasury collateral, USDe investors may begin to preemptively sell tokens to avoid additional losses, causing further redemptions that could potentially incite forcible USDe liquidations or a market-wide crisis of confidence should the unwind occur in thin markets with high demand for hedges (i.e., during a market downturn).

At its core, Ethena is an unregulated tokenized hedge fund. Even though its basis trades proved immensely successful in Q4 2024, investors should consider the various unknowns surrounding the protocol that could create problems when funding rates shift.

i dont get why so many people are focused on ethena's high yield (its a basis trade) instead of the fact that there's been 2 projects that tried this before and both gave up because they lost money due to yields inverting

— 0xngmi (@0xngmi) February 20, 2024