The Hyperliquid Altcoin That's Getting Interesting Again

In my opinion, Hyperliquid has one altcoin worth talking about: KNTQ.

The governance token for Kinetiq, Hyperliquid's largest staking operation, sits on top of two core products: liquid-staked HYPE, primarily kHYPE, and Markets, Kinetiq's own perpetuals exchange.

KNTQ is where the money lands. Revenue from staking, Markets, validator commissions, and the rest gets routed into KNTQ buybacks that flow to staked sKNTQ holders.

That said, today Kinetiq introduced a new revenue stream: Launch, a marketplace-as-a-service platform that gives deployers a path to crowdfund HIP-3 markets, kHYPE holders a new way to earn, and, with any luck, KNTQ more revenue.

Much of this is contingent on how Kinetiq’s faring thus far, so to make sure we accurately assess the impact Launch may have, we must look at how Kinetiq’s been holding up.

Launch by Kinetiq will go live on Wednesday, June 10th. pic.twitter.com/x8iJJota3i

— Kinetiq (@Kinetiq_xyz) June 3, 2026

How It's Faring

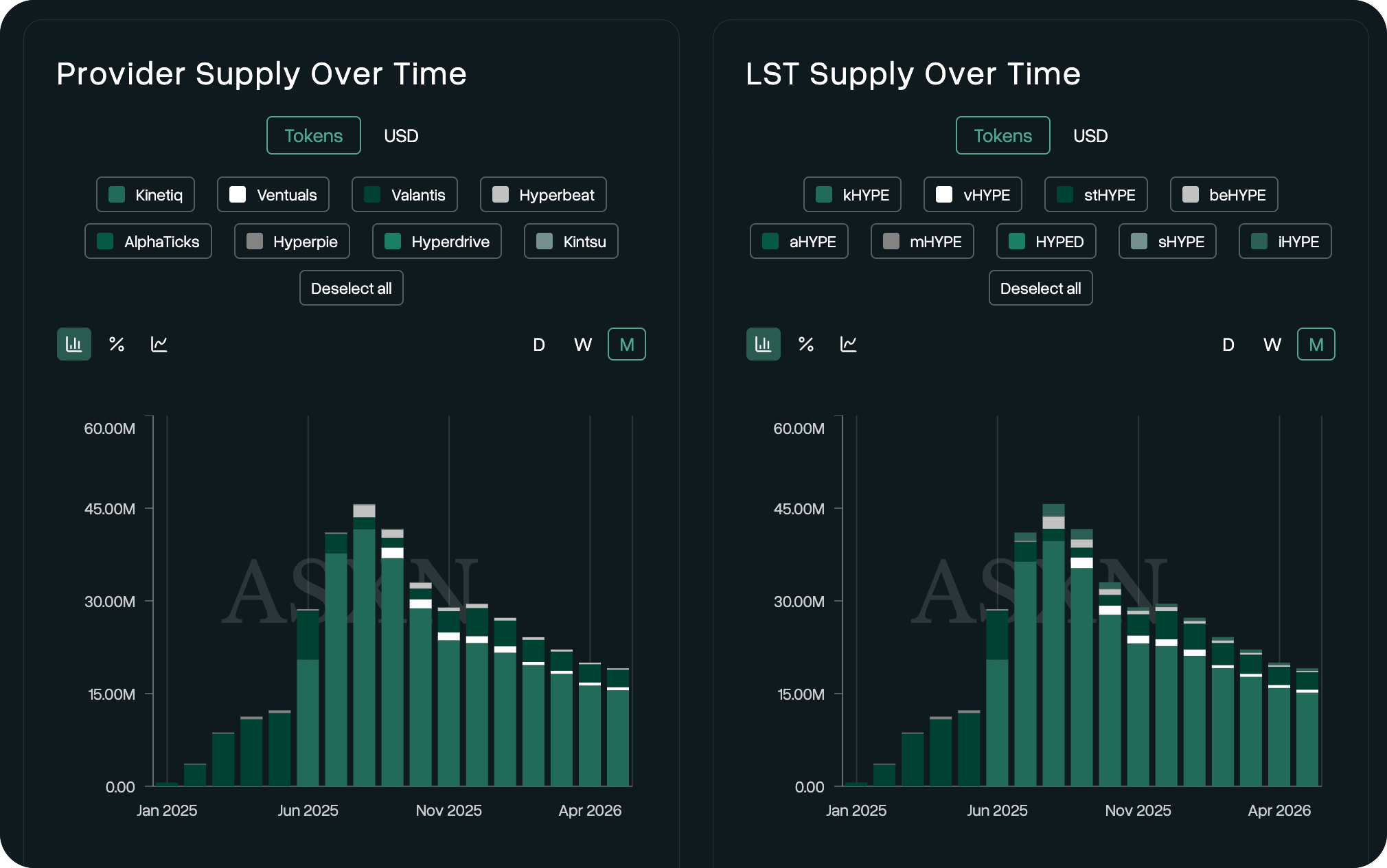

Kinetiq's core strength is being the largest liquid staking protocol for HYPE, responsible for over 80% of the liquid-staked supply, with over $1B in TVL currently.

Share is not size, though, and kHYPE's supply tells a less promising story. Total kHYPE supply has dropped from its high of 41.5M last August to 15.6M as of May 31st, a 62% decline. Alongside that, liquid-staked HYPE as a share of total staked HYPE has fallen from 10.42% to 4.42% over the same period, even as overall HYPE staking has grown slightly, to 43% of supply.

So, while Kinetiq's share of the liquid-staking market has held steady or even increased, its core staking business is shrinking. HYPE holders appear to be favoring native staking over liquid staking, likely because the DeFi that gives liquid staking its purpose has stagnated while its risks have piled up, reducing the HYPE flowing through kHYPE and weighing directly on Kinetiq's revenue.

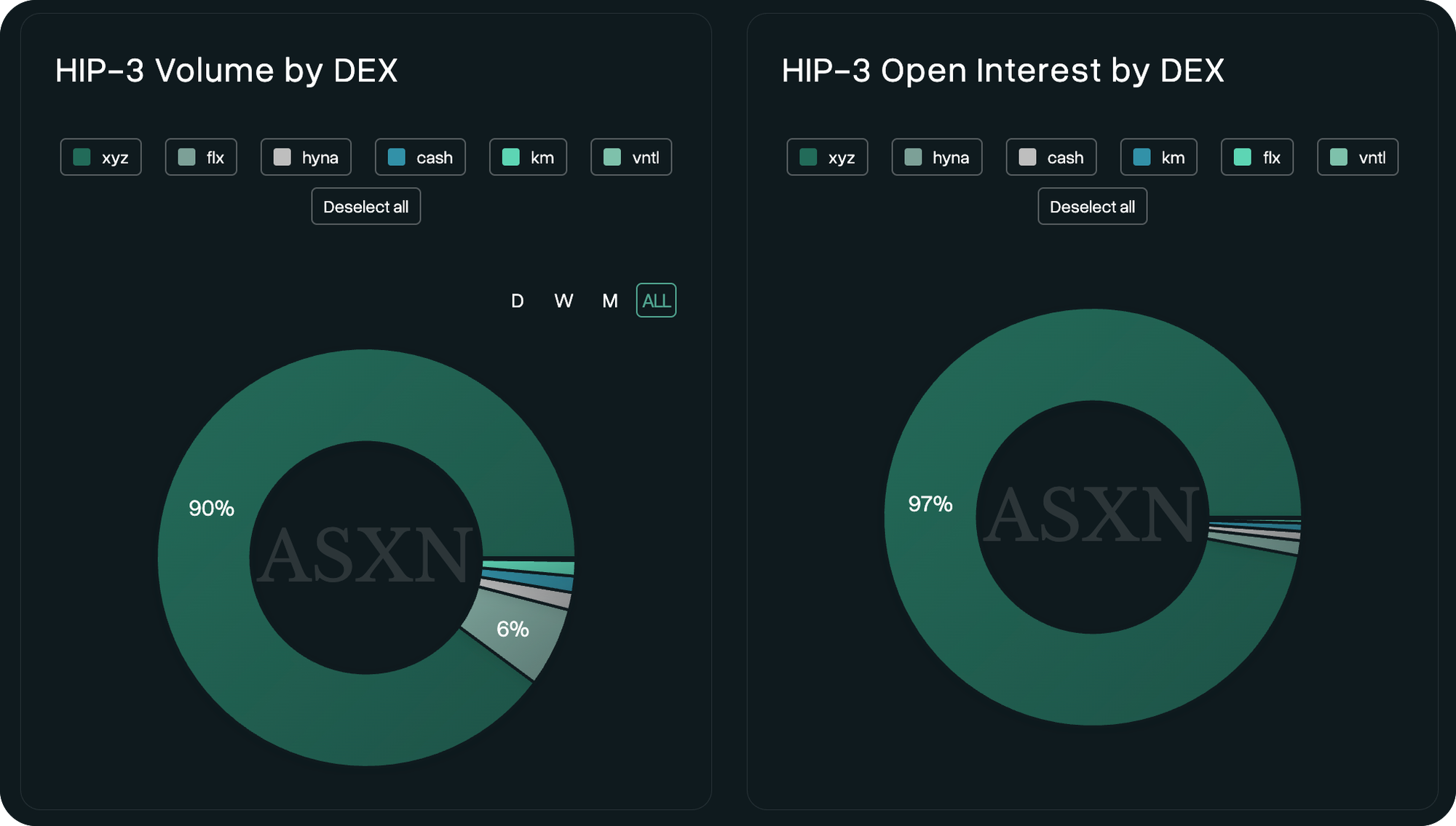

Kinetiq's HIP-3 exchange, Markets, tells a similar story of compression, running into the same wall every HIP-3 venue hits: Trade.xyz, the largest HIP-3 exchange, owns the liquidity, and traders go where the liquidity already is.

A big piece of the liquidity problem was the margin asset: Trade.xyz launched on USDC, while Markets bet on USDH, which fragmented liquidity instead of giving traders the margin with the lowest friction. Felix, another HIP-3 deployer, recently wound down citing this dynamic as a core reason, and Kinetiq's market share shows the same drag: averaging just 1.45% of market share since Market’s launch against Trade.xyz's 89%, lately closer to 95%.

These dynamics show up in Kinetiq’s financials, with revenue and earnings peaking in Q4 last year.

What Launch Is

Launch hopes to change that. It's HIP-3-as-a-service, a way to crowdsource the heavy lift of spinning up a perpetuals exchange.

Deploying a HIP-3 exchange normally means locking up more than 500,000 HYPE and running everything around it. Launch breaks the capital piece into a pool. A team that wants an exchange gets an isolated staking pool, HYPE holders contribute the stake, contributors earn rewards from that exchange, and Kinetiq takes a slice of deployer revenue that feeds back into KNTQ buybacks. Instead of betting its HIP-3 upside on one exchange, Kinetiq can earn from many.

Kinetiq Launch is probably one of the most important products being built on Hyperliquid right now.

— Vikingo.hl (@VikingoDigital_) June 4, 2026

Think of it as Kickstarter for HIP-3 exchanges.

Until now, launching a HIP-3 perp exchange required staking 500K+ $HYPE, creating a capital barrier of more than $20M.

Launch… https://t.co/gwOsAWo5V8 pic.twitter.com/94b71GtXZe

The catch is that Trade still dominates and it's hard to imagine that changing with new Launch markets. HIP-3 keeps growing as a share of Hyperliquid's total volume, with stock-based perpetuals as the primary draw. Trade is the venue for those, and its size gives it the best depth and pricing. New venues will still need traders, market makers, and a reason to exist that Trade doesn't already cover.

Further, new deployers differentiating by launching “esoteric markets” here (think Pokemon cards, compute, etc.) does not prove competitive: once one gets traction, Trade can simply copy it, the trap Felix cited on its way out. It’s a tricky situation, and probably not where Launch will find its best success.

Yet, Launch will also crowdfund HIP-4 markets, Hyperliquid's new binary outcome markets, which open the door to prediction markets and options. These markets are early, which leaves far more design space for newcomers than HIP-3 does. Only twelve HIP-4 markets are live today, across a thin set of topics. There are no options markets yet, and plenty of prediction markets left to build. And while stocks are what people want to trade on leverage, there's a long list of events people want to bet on that no prediction market lists yet.

The copy trap bites less here, and not just because small markets are not worth chasing. Perps are continuous markets where duplicate listings compete around the same instrument, so liquidity tends to compound around the deepest venue. Prediction markets are different: demand splits across thousands of uncorrelated, time-bounded events, and a copied market may resolve before a rival can bootstrap real depth.

Timing helps too. HIP-3’s race was decided before Launch existed, while HIP-4 is still in its curated rollout, so Launch can be at the line before permissionless deployment fully opens instead of chasing a flywheel that already spun up. The pooled model fits the shape of these markets on top of that: no solo deployer wants to commit scarce HYPE capacity to one-off event markets, but a crowd might fund a rolling portfolio of them, and Kinetiq takes a slice of each. It does not need any single market to be huge. It needs the tail to be wide and active.

If Kinetiq's next leg of growth comes from anywhere, the open field is more likely than the crowded one. Keep an eye out here.