The Bull Case for Lido

The rise of restaking caused crypto investors to dump Ethereum staking heavyweight Lido Finance in the first half of 2024, sending LDO sliding into multi-year lows against ETH.

In the past few weeks, LDO investors were re-invigorated by the protocol's potential to upset the EigenLayer ascendancy. But on Friday, LDO holders were dealt a massive blow after the SEC designated its liquid staking token as an unregistered crypto asset security in a lawsuit filed against MetaMask creator Consensys.

LDO may have sharply underperformed ETH on a year-to-date basis, but today, we’re discussing why the fundamental bull case for LDO has never been stronger 👇

🥩 Restaked Competition

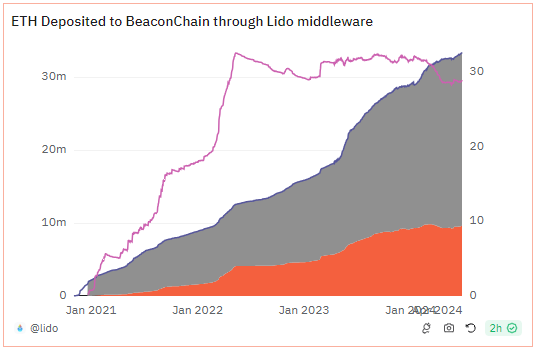

During 2023, Lido was an unstoppable force, accumulating one out of every three ETH staked and doubling its Ether under management.

Throughout the year, Lido’s control over the percentage of ETH staked has consistently threatened to crack 33% – the first of three critical thresholds at which a staking entity can more easily manipulate consensus – inciting lively debates among Etherians about whether the ecosystem should forcibly limit Lido’s stake to prevent unwanted centralization.

In 2024, these contentious conversations have drifted into the periphery along with a decline in Lido’s share of ETH staked to a seemingly more acceptable 29% (purple line), the lowest level since April 2022.

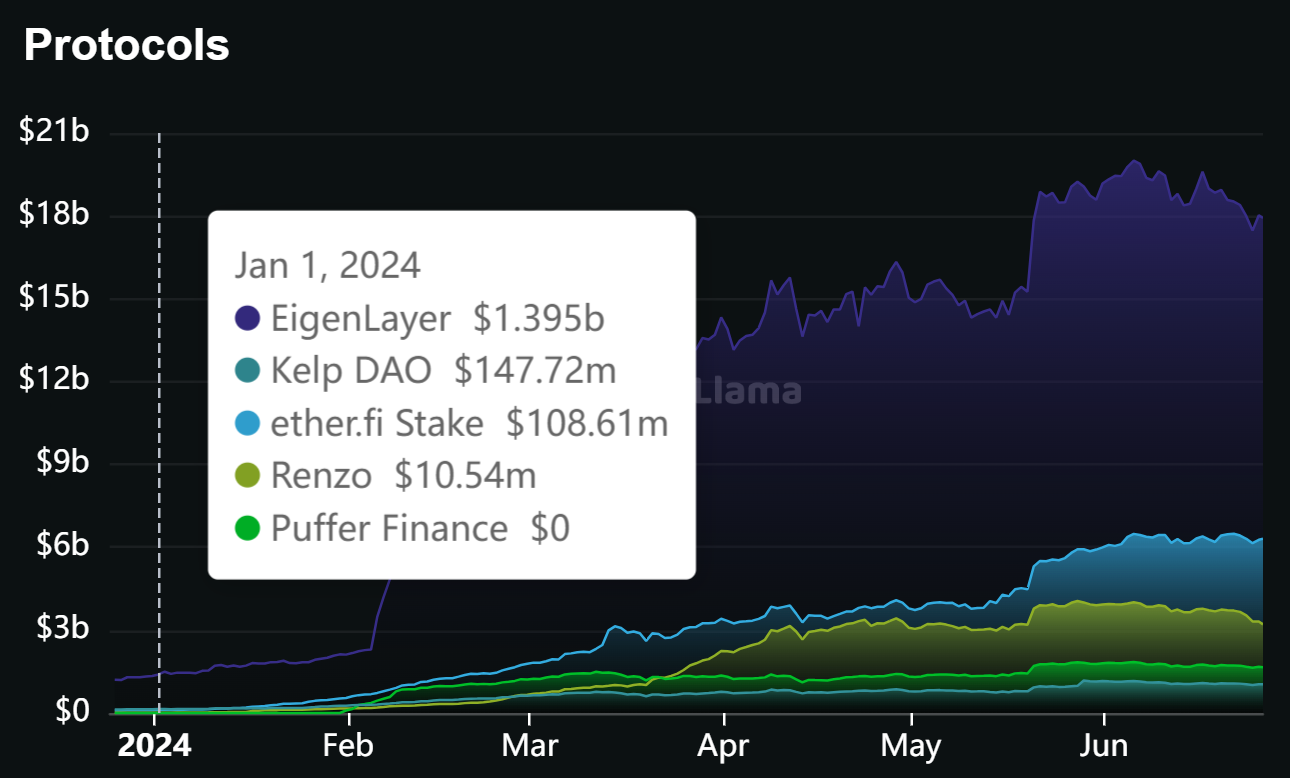

Though Lido has continued to enjoy net ETH inflows, the protocol’s market share downturn coincided with the emergence of a breakout phenomenon that challenged the dominance of its vanilla staking model: restaking. Despite the fact that restaking services are neither operational nor producing yield to this day, projects offering exposure to the meta through promised future airdrops quickly became the hottest farms of the year.

In just a few months, EigenLayer, ether.fi, Renzo, Puffer, and Kelp all progressed from relative obscurity into trusted protocols with billions of dollars in TVL!

Putting aside the contested merits of restaking, the attraction of their associated airdrops has been undeniable, empowering Lido’s restaked competitors to gobble up market share thanks to the outsized amounts of capital chasing these lucrative airdrops.

The arrival of EigenLayer’s much anticipated airdrop catalyzed a second wave of depositor excitement in May, yet the rise of a Lido-aligned restaking alternative threatens to reshape the sector’s landscape…

🧬 Symbiotic Relationship

Symbiotic’s deposit contracts hit mainnet just two weeks ago and have already accumulated $300M in deposits since their launch, making it the fastest growing restaking protocol in June and one of the few in the sector to experience TVL inflows this month!

The protocol is undeniably the most credible EigenLayer competitor in existence by virtue of its seed funding from reputable crypto venture capital firms Paradigm and cyber·Fund, an investment company that served as an early contributor to Lido DAO.

Although Symbiotic is largely an EigenLayer carbon copy, planning to offer restaked services for a wide variety of assets, this restaking ecosystem is uniquely differentiated through its close connections to Lido.

Coinciding with the launch of Symbiotic was the release of Mellow Finance, a restaking vault management service that is also backed by cyber·Fund and was designated as the first member of the “Lido Alliance,” a status conveying an official partnership with and endorsement from Lido.

Introducing advanced DeFi strategies for stETH with Mellow & Symbiotic ✨ https://t.co/dzmYEFY8dM

— Lido (@LidoFinance) June 11, 2024

A new initiative to provide stETH holders with access to new DeFi opportunities, including restaking. pic.twitter.com/KRIqIPzvAa

Unlike the EigenLayer model of liquid restaking, which encourages user deposits to non-Lido restaking managers who independently stake, Mellow Finance’s managed deposit model transitions restaking operators into mere liquid staking tokens delegators.

Compared to the popular alternatives for liquid restaking, Mellow Finance better manages the liquidity risk associated with LRTs (i.e.; the need to withdraw through the Ethereum staking queue to convert to ETH at par in the event of a depeg) by enabling their expedient conversion into LSTs; this design also reinforces the implicit winner-take-all dynamics of staking.

As token liquidity is a key factor in evaluating the attractiveness of an LST and Lido maintains a monstrous 60% share in this segment of the staking market, stETH restaking through Mellow offers a clear advantage from a risk-adjusted perspective.

While stETH holders were only able to earn airdrop exposure to a single opportunity under the EigenLayer regime, they can earn both Mellow and Symbiotic points by utilizing Mellow.

Simultaneously, many EigenLayer restaking projects have already distributed an initial round of tokens, diminishing the potency of their future rewards and solidifying Mellow’s position as the top airdrop farm.

Once the fundamental bull case for Symbiotic x Mellow restaking becomes apparent as existing stETH capital migrates to this opportunity, there is an extremely high probability that EigenLayer’s mercenary capital will outflow from associated LRTs into stETH, finally sparking measurable growth in Lido’s staking market share for the first time in two years.

🧐 Closing Thoughts

The SEC’s attempt to designate Lido’s stETH as a crypto asset securities poses unresolved risks for unregistered staking services, but this event likely created a local capitulation bottom and leaves little room for unexpected dangers to derail LDO until the pending litigation is decided in multiple years' time.

Businesses do not need to be sexy to be sound investments, and although restaking has become a focal point for crypto investors, staking providers similarly generate fees from depositor yield and come with the added benefit of a proven revenue stream.

With Lido’s $30B+ in ETH under management earning 3% APR, the protocol currently generates $1B in annual income at its 10% take rate, giving the token a price to earnings (P/E) ratio of ~23x. Although considered “average” for a stock, such a multiple appears to underprice LDO given the crypto industry’s heightened growth potential and aforementioned Lido-specific tailwinds.

Admittedly, Lido’s current 10% management fee to operate a low cost software enterprise could be easily subject to compression should a competitor attempt to corner the market with a low cost alternative, however, widespread stETH integrations throughout DeFi and market leading liquidity provides Lido some degree of flexibility to charge a premium for its services.

Presuming the Symbiotic ecosystem shines in the coming months, stETH will yet again approach the 33% staking concentration threshold, and while this is bound to reignite the argument over whether Ethereum should impose a hard cap on Lido, fragmented social consensus will have a difficult (if not impossible) time implementing such drastic network changes.