Synthetic Dollar Slump

Fall from Grace. The token of synthetic dollar stablecoin issuer Ethena underwent an impressive post-launch surge, but once the initial rally petered out, ENA found itself caught in a perpetual downtrend! Why has ENA continued to plunge, and what moves is the team making to bolster adoption of its stablecoin?

ENA achieved all-time highs in both dollar and BTC-denominated terms on April 11, a mere two days before USDe reached peak supply and broader risk markets took a turn for the worse, seemingly plunging on concerns of elevated conflict in the Middle East.

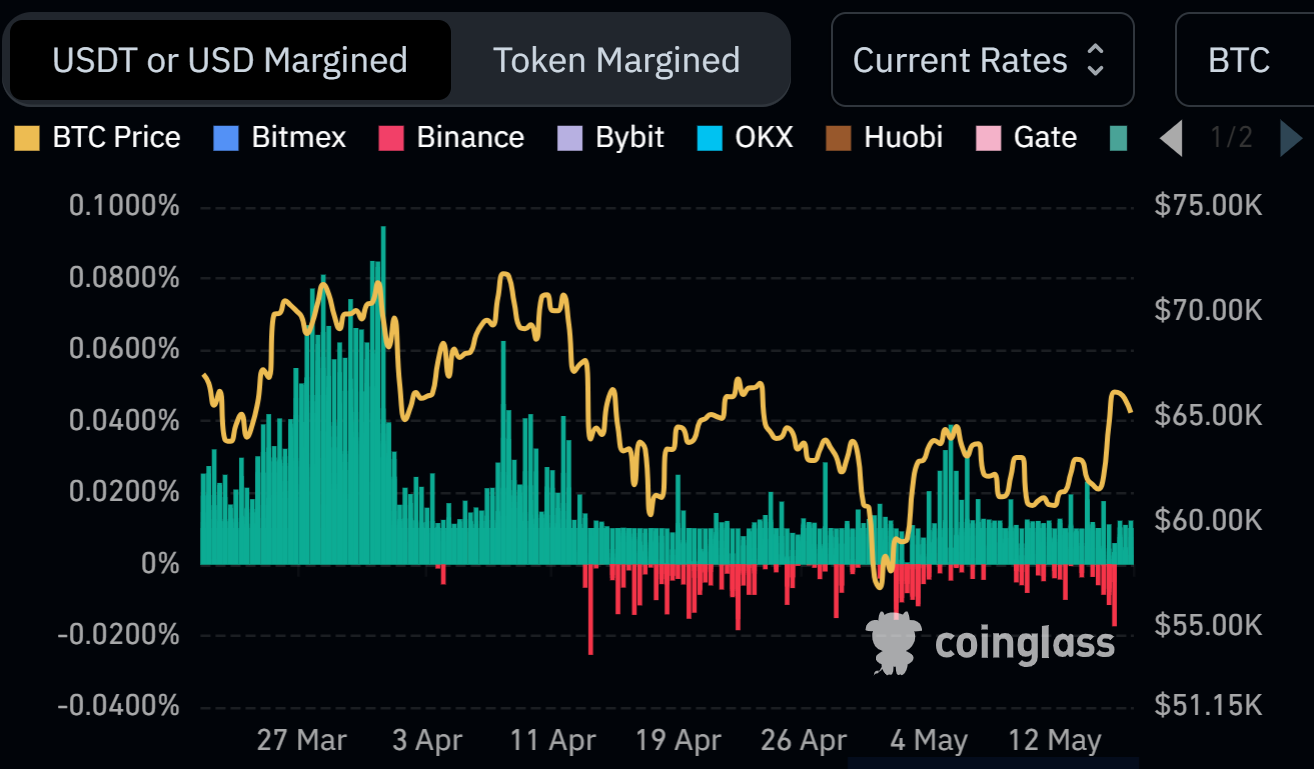

While funding rates on the BTC and ETH perpetual swaps (the predominant source of Ethena’s revenue) cooled significantly coming into April, speculation over the impending second wave of ENA airdrop rewards fueled demand for Ethena assets and allowed yields to remain elevated.

This bastion of return support has since crumbled, with fixed yields on USDe swaps from Pendle compressing to 29% from the 100%+ levels seen at the beginning of April.

In recent weeks, mounting evidence has begun to suggest that crypto markets may have shifted into a more negative funding rate regime, with funding rates dipping negative for persistence periods of time throughout April and into May.

Although extremely elevated funding rates as BTC smashed into all-time highs the first two times turbocharged returns on Ethena’s delta-neutral strategy and resulted in an influx of deposits, negative funding rates have begun to eat into yields, reducing the attractiveness of holding USDe and creating concern about future outflows.

Due to fact that net negative funding rates would cause the depositors to incur a loss, Ethena established an insurance fund at its inception, which receives a portion of the yield generated and has accrued $39.4M in reserves to safeguard against losses on $2.32B in outstanding USDe liabilities, a meager 1.7% buffer.

Today, Ethena announced that it would be reducing the portion of revenues that it retains for the insurance fund from 50% to 20%, allowing returns on sUSDe to nearly double to 37% APY, a change that is expected to last until at least June and coincides with Ethena’s Bybit integration, which will enable users on the CEX to utilize USDe as trading collateral.

To date the sUSDe contract has received protocol yield attributable to assets backing staked USDe, with the protocol retaining the remainder

— Ethena Labs (@ethena_labs) May 16, 2024

As of today, the retained portion is reduced to 20%, with the remainder going to the sUSDe contract

As a result sUSDe APY = 37.2% pic.twitter.com/lAMiFeCHMt

Funding rate compression has clearly taken a toll on Ethena, forcing the Protocol to adopt increasingly drastic measures to promote adoption of its dollar-pegged assets.

Unfortunately, this most recent action is but a half-measure, providing a fleeting distraction from underlying fundamental issues. Even at a 50% take rate, the Ethena insurance fund was woefully inadequate to compensate depositors for losses from a prolonged period of negative funding rates.

Institutional players have begun arbitraging the basis between spot BTC and futures contracts, indicated by the holdings of spot BTC ETF among hedge funds, increasing competitiveness for the types of trades utilized by Ethena and squeezing profit margins.

Should crypto truly be transitioning into a more negative funding rate environment, ENA will continue to struggle and it is likely that Ethena will be forced to tap the insurance fund, the depletion of which could spawn a crisis of confidence about the backing of USDe.

Millennium is king of the bitcoin ETF holders w/ about $2b across four ETFs. This is out of over 500 holders (about 200x the avg for new ETF). Majority are inv advisors (60%) but a big dose of HFs (25%). Never can be totally sure what HFs up to but they were def big buyers. pic.twitter.com/iVtVXjhId0

— Eric Balchunas (@EricBalchunas) May 15, 2024