Silvergate Crashes the Party

Dear Bankless Nation,

After a couple of months of crypto peace and prosperity, there’s trouble brewing with a good old-fashioned bank run facing crypto-friendly Silvergate. Things aren’t looking great with a mass exodus of depositors and the bank staring down the barrel of insolvency.

A TradFi blowup ought to push regulators to establish clearer guidelines and protections for good faith actors aiming to innovate, but in all likelihood the federal government will just use this as another excuse to put up roadblocks for institutional players that embrace crypto.

- Bankless team

If you've ever onramped into crypto through a centralized exchange, you have likely indirectly used Silvergate bank.

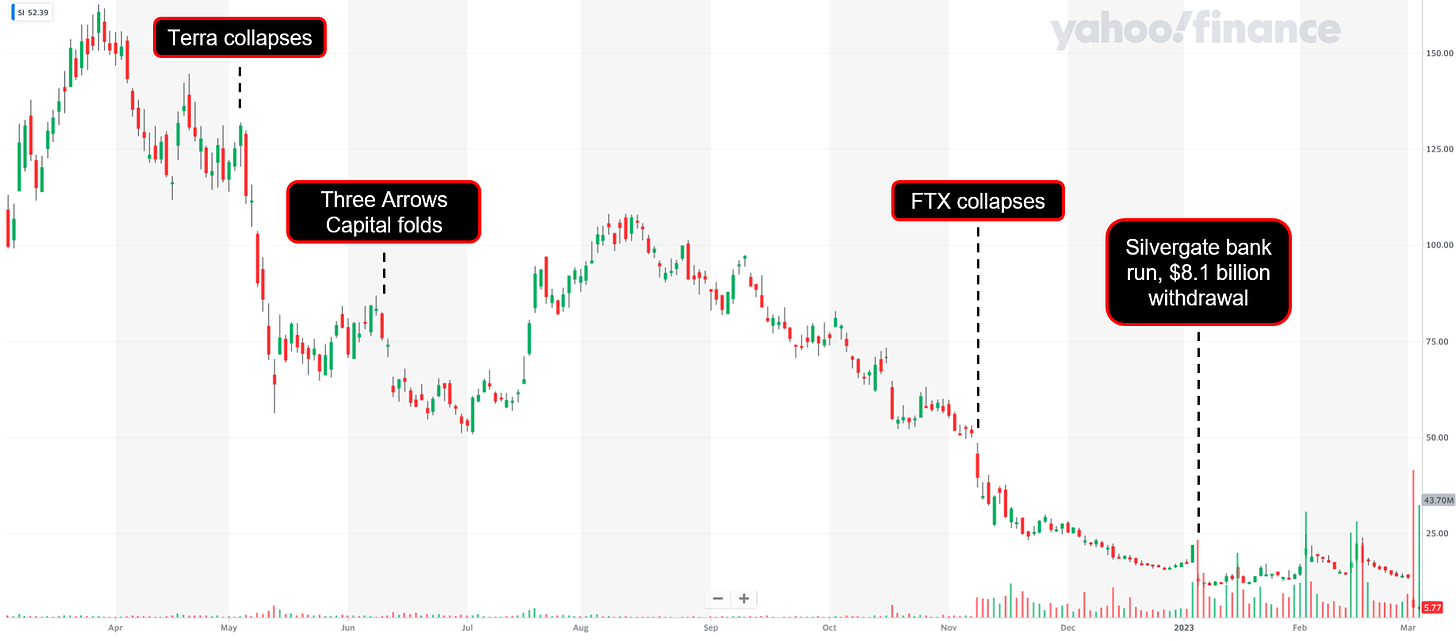

Silvergate is the biggest crypto-friendly bank, with 90%+ of its deposits from the crypto sector. The bank pivoted from a small regional presence in the past decade into a major bank with $12B in deposits by Q3 2022, servicing major crypto institutions like Coinbase, Gemini, FTX and BlockFi.

After months of turmoil, Silvergate is seemingly capitulating under a mix of regulatory and market pressure this past week — undergoing something of a bank run.

The straw that broke the camel’s back was Silvergate’s two-week delay of its annual 10-K SEC filing last Thursday, citing the need for more time to assess its finances. Silvergate’s stock immediately spiraled on the news, dropping 55% to around $6.50 per share. JPMorgan analysts downgraded Silvergate’s already-beaten down stock from “neutral” to “underweight” rating.

In response, Silvergate’s clients began severing ties with the bank’s services. Coinbase quickly distanced itself when it announced a switch to Silvergate’s main competitor Signature, another crypto-friendly bank.

At Coinbase all client funds continue to be safe, accessible & available.

— Coinbase (@coinbase) March 2, 2023

In light of recent developments & out of an abundance of caution, Coinbase is no longer accepting or initiating payments to or from Silvergate.

Other clients that have left Silvergate for greener pastures include Paxos, Crypto.com, Bitstamp, Cboe Digital Markets, Galaxy Digital, Gemini and LedgerX.

On Friday, Silvergate was forced to suspend its Silvergate Exchange Network (SEN), its zero-interest payment platform that crypto companies use to make fiat transactions with one another.

Silvergate’s insolvency concerns have been brewing for months.

When crypto suffered a credit crisis in 2022, Silvergate saw an $8B drawdown. To maintain a liquid balance sheet, the bank was forced to off $5.2B worth of bonds in its portfolio amid a high interest rate environment where the Fed was hiking rates to stave off inflation, incurring losses of $751.4M.

Silvergate also borrowed a whopping $4.3B in short-term loans from the Federal Home Loan Bank (FHLB) system, a government-backed shadow bank that supports domestic commercial banks in poor market conditions by borrowing from institutional investors at generally below market interest rates and lending to member banks.

Silvergate survived the FTX collapse but it did not come out unscathed. The bank reported a ~$1B loss for Q4 2022 and was forced to cut its staff by 40% (200 employees).

Unfortunately, the bank’s close association with FTX attracted the attention of regulatory hawks, increasing reputational risk and investor uncertainty.

U.S. Senators Elizabeth Warren, John Kennedy and Roger Marshall began probing Silvergate on December 6 for its role in facilitating fraudulent transfers between FTX and Alameda, alleging an “egregious failure of Silvergate’s responsibility to monitor for and report suspicious financial activity carried out by its clients”. Silvergate’s press release then claimed that total deposits from FTX were less than 10% of all its $11.9B deposits.

On February 2, U.S. prosecutors in the DoJ were reportedly investigating Silvergate’s for its relationship with FTX and Alameda.

In short, Silvergate is buckling under the combination of a massive capital withdrawal plus unwanted regulatory scrutiny. Bad liabilities, not bad assets, are the root of the problem. Unlike Three Arrows Capital or FTX, the ongoing bank run on Silvergate is not due to the implosion of risky overleveraged loans against volatile crypto collateral. As Bloomberg’s Matt Levine writes on Money Stuff:

The story today is that Silvergate’s customers are withdrawing their money because they are worried about Silvergate, “in light of recent developments & out of an abundance of caution,” classic bank-run stuff. But that's not why they were withdrawing their money in late 2022, when the trouble started. Then, they were withdrawing their money because crypto had collapsed: Silvergate’s crypto-exchange customers faced withdrawals from their customers, so they took their money out of Silvergate. The customers — crypto exchanges — were the problem, not Silvergate.

Ultimately, the knock-on effects of FTX contagion is starting to catch up with Silvergate. As the main channel for market makers in crypto to move capital quickly, Silvergate’s demise does not bode well for the industry.

The Silvergate panic led to a total crypto market cap dip of 4.8% during ETH Denver week.

This fiasco also poses an important existential question for crypto: how can crypto survive without relying on centralized, TradFi rails?

The easy answer is “just don’t use TradFi”. But that is perhaps too naive in the short-term, and the reality is there will be some dependency on financially regulated institutions to facilitate capital flows in and out of the sector.

If so, crypto must avoid putting all its eggs in one basket and not build into a centralized pothole as it seems to have done with Silvergate. As it stands, the small handful of crypto banks — in particular Silvergate and Signature — represent convenient chokepoints and easy targets for anti-crypto regulators to undermine the industry.

Diversification of crypto banks is key, but unfriendly actions and a general lack of support from financial regulators have made it extremely difficult for banks to embrace new financial technologies and serve crypto clients. This has hamstrung the sector and may leave America’s dinosaur financial institutions less willing to take risks to innovate.