ROLLUP: Chaotic Era | Oil, Jobs, Credit | Nasdaq x Kraken | BlackRock Staked ETH | Roman Storm Retrial

TIMESTAMPS

Ryan Sean Adams:

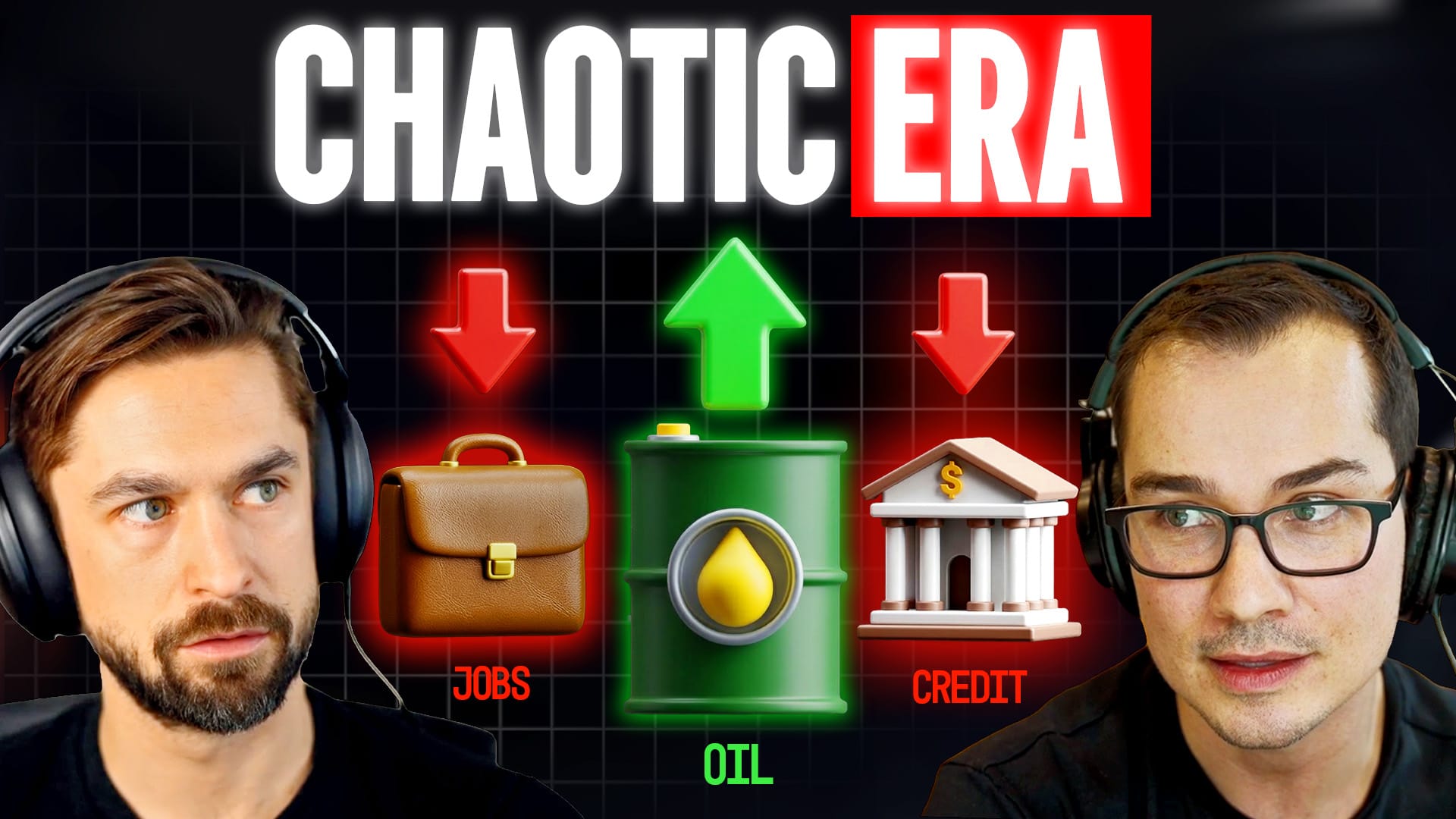

[0:04] Bankless Nation is the second week of March. It's time for the Bankless Weekly Rollup. We got some jittery markets today. You know, Vitalik, we got a jittery world. Yeah, jittery world. You know, Vitalik calls this the chaotic era. I saw him tweet something about that this week. I think that's we've moved from the stable era to the chaotic era. We're feeling that in the markets. Wars, we got AI, just overall jitters in the market. There's three things, though, we're paying attention to. We're going to talk about them. Oil, jobs, private credit, and how all those things affect crypto.

David Hoffman:

[0:33] Lots of big announcements on the crypto side of things as well. Kraken and the Nasdaq announced a partnership to issue and trade real tokenized stocks. Not the fake ones, the real ones. On which chains, a few chains, are going to be the winners here. And also, breaking news, as of today, BlackRock has released its long-awaited staked ETF.

Ryan Sean Adams:

[0:55] Finally!

David Hoffman:

[0:56] Wow. Finally, just in the phase of the market where no one cares.

David Hoffman:

[1:01] So we're going to talk about how to, we're going to pop up in the hood, talk about how that works, what are the fees, what's the stake rate, how all of that is going on the week.

Ryan Sean Adams:

[1:07] There's also some disappointing news on the week. The DOJ has decided it wants to retry the Tornado Cash case with Roman Storm. I thought that was done. Can we really say America is the crypto capital of the world if we're going and we're prosecuting our open source privacy developers, David? We got to talk about that. But also, maybe the Democrats, though, would be worse for crypto in the White House. Bernie Sanders has introduced a moratorium on AI data centers. David, we have to have a discussion about the coming AI tech backlash that I think the two of us both see.

David Hoffman:

[1:40] You know how in 2022 and 3, post-FTX, the Democrats came with their band hammer on crypto and tried to regulate crypto out of existence? And then crypto banded together and made the Fairshake super pack and a bunch of other super packs. I think we are, AI is in the phase of their political lifespan where the Democrats come and try and banhammer them and then they're going to need to rally together and fund.

Ryan Sean Adams:

[2:08] I think they're way more organized than crypto. I think they're already doing

Ryan Sean Adams:

[2:11] this. There's a lot to unpack there, so let's get to it.

David Hoffman:

[2:13] Our friends and sponsors over at- David.

Ryan Sean Adams:

[2:15] We got an animal of the week, okay? It is the forbidden third animal. You know the bull. We've been in bull markets before. We've been in bear markets before.

David Hoffman:

[2:24] We don't like those.

Ryan Sean Adams:

[2:26] We're in a bear market right now. But there's a third animal on the screen here. What are we looking at?

David Hoffman:

[2:30] We are currently in a kangaroo market. We've previously had the crab market. I think bankless listeners will be familiar with the crab market. The crab market goes sideways. Kangaroo market also goes sideways, but first it goes up and then it goes down and then it goes up and then it goes down. But it ends up sideways no matter what.

Ryan Sean Adams:

[2:49] This is actually, I think CNBC is saying it's a kangaroo market. So they're on board with the meme. Let's talk about the three things we're looking at. Number one is oil prices. Number two is the job numbers on the week. And the third is some tremors in private credit. So maybe let's start with oil. This, of course, is going on because of the war in Iran. We've seen some kangarooing on the oil price. What are we looking at?

David Hoffman:

[3:15] Yeah, definitely kangarooing up, however. I think there is a large story being told in the price chart of oil. To me, the way I interpret this is the higher the price of oil, the more pressure is on Donald Trump and the United States to end this conflict, this war in Iran, because, you know, war increases inflation that hurts people domestically. It makes people upset with the United States. When the oil price is lower, it gives Donald Trump and the U.S. Military a longer leash to continue doing whatever they're doing in Iran.

Ryan Sean Adams:

[3:49] The public also sees it at the pump directly, right? This is price of the pump over the last year. Look at this spike up ever since the war outbreak began.

David Hoffman:

[3:57] Yeah. There's just been some crazy volatility in the oil market. So on Monday, oil jumped 30% in one day from just a handful of key events. The Islamic regime said that they would be closing the Strait of Hormuz. That's where 20 to 30 percent of the world's total oil consumption passes through. About 50 to 21 million barrels of oil per day passes through the strait. There were some Israeli strikes on Iran's oil depots and refineries, and then Iranian drones attacked Qatari gas facilities and also Saudi Amarco's refinery in Saudi Arabia. So just a bunch of volatility in the oil market. Then Energy Secretary Chris Wright posted on X that the Navy had successfully escorted an oil tanker through the Strait of Hormuz. So everyone's like, oh, the straits open again. The United States military is protecting the oil tankers going through. Then they deleted the tweet. But not before oil plunged 20% on that news. But then the White House confirmed that no escort had taken place. And then oil started pumping again, erasing all of the gains in the stock market that it had that day. So right now, I think oil is the price that dictates the stock market, the global stock markets, and basically everything else.

Ryan Sean Adams:

[5:11] Well, yeah. I mean, I will say, though, the stock markets haven't been responding too much in kind. I mean, we have – There's

David Hoffman:

[5:18] Been intraday tracking of oil.

Ryan Sean Adams:

[5:22] Yeah, that's right. That's true. But I mean, since the war started, the S&P is only down 2.5%, which is like if it was tracking the price up of oil, I mean, oil has gone what? Like, where did it go to? Almost $120 per barrel?

David Hoffman:

[5:38] Oil is up 40% since the start of the Iran conflict.

Ryan Sean Adams:

[5:41] Right. And so it's almost surprising as stocks have not responded in kind in that way. I mean, there's some interesting volume going on on Polymarket right now when you look at the crude oil price by the end of March. So 4% chance that we hit $200 per barrel by the end of March. And this is on some pretty significant volumes.

David Hoffman:

[6:01] Yeah, it's actually pretty clear, I think. I mean, I don't really know. I don't know who's trading this, but there is $25 million of volume. And I can only imagine that the majority of that volume came after a lot of this volatility happened. To me, it indicates that there is actually pretty clear hedging activity going on, or at least some sort of financial use case of this market, which is nice to see.

Ryan Sean Adams:

[6:22] I mean, kangaroo market makes sense when you're dealing with the uncertainty of war. And right now, it seems like the oil markets are obviously trading on whatever the news of the war is.

David Hoffman:

[6:33] Or the tweets of the president about the news of the war.

Ryan Sean Adams:

[6:37] Exactly. And the question is, I think the market's asking is like, how long is this going to go on for? Right. So you've got some variables that are pointing the direction of a short type of conflict, something that won't persist. One of them is the popularity of this war. It's not super popular. You might call this mixed, but there's five in 10 that oppose the war. There's four in 10 that support. There's like one in 10 that is somewhat undecided. I think in order to have a longer persisting war in the US, the public would have to start with higher numbers to be on board with this. So that's gonna be a political pressure that Trump is facing. And it seems like he is looking for some of the exits or at least he's hedging. So there was a phone interview with CBS News and Donald Trump on Monday. So it was March 9th. He said this, I think the war is very complete, pretty much. We're very far ahead of schedule. So what is that? How do you interpret that?

David Hoffman:

[7:37] He's been giving mixed messages to the press. There was one interview where he gave where he said, yes, we've basically achieved everything that we've had to achieve. The war is almost over. But also, it could just be the beginning at the same time. He's just saying both. He's just saying all the things? He's just saying all the things.

Ryan Sean Adams:

[7:55] So he can select later. That's classic Trump, right?

David Hoffman:

[7:57] Exactly, which is not a bad strategy. I think Donald Trump does know that the Iran war needs to be deeply in the rearview mirror by the time the midterms come around.

Ryan Sean Adams:

[8:07] Yeah.

David Hoffman:

[8:07] There's a reason why. They would not have done this approximate to the time of the midterms. Yeah.

Ryan Sean Adams:

[8:14] Oil price is going to be a pressure on him. political sentiment is going to be a pressure on him. Market sentiment will be a pressure on him. All of these will make him want to end this faster. Actually, another interesting poly market is a US and Iran ceasefire by what date? So a 23% chance that that happens by March 31st, according to poly market. By April 30th, a 47% chance. And by June 30th, a 61% chance. Market using the same logic you did, which is like, resolve this in time for the midterms.

David Hoffman:

[8:46] Yeah. There's also a decent amount of volume on this one. I don't think the ceasefire makes sense because, okay, so the settling of this market says this market will resolve to yes if there is an official ceasefire agreement and a mutually agreed halt in direct military engagement. I bet Donald Trump is just going to declare victory. However, however it lands, he's like, whatever, however it landed, that was what we wanted. Like we won and now we're out of there. Peace. Like ceasefire means like a.

Ryan Sean Adams:

[9:18] Truce to me. Something more structured.

David Hoffman:

[9:19] Yeah. Like I don't, Donald Trump's not going to do a truce. He's like, no, we beat you guys. And now we're going home with our like gold medal.

Ryan Sean Adams:

[9:26] Yeah. I mean, it could be. What's interesting is the dollar is holding up pretty well. I mean, we talked about that last week, but the dollar is really proving itself as a flight to safety type asset. It's closing in on one year. the DXY, that is. Gold is not doing very much either. So it's kind of hovering at the 51,000 per ounce. Crypto prices as well, a bit of a kangaroo on the week. We had some hops up though, didn't we?

David Hoffman:

[9:51] Yeah, we had some bullish days. We had some bearish days and we were just hopping around. Overall down 1.1% for Bitcoin on the week and down 1.5% for Ether on the week. Not much of a story, I would say. It's also hard to tell a story about gold as it relates to the price action downstream of the conflict because gold is on the backs of a huge speculative bubble where it ran from 3,000... A speculative euphoria. Yeah.

Ryan Sean Adams:

[10:19] A big run-up for the last two years,

David Hoffman:

[10:20] For sure. A run-up. And it's drawing down based off of that run-up.

Ryan Sean Adams:

[10:25] Yeah.

David Hoffman:

[10:26] And that is just very close to the Iran war conflict. So, like, those two bits of signal are, like, interacting with each other and interfering. Interfering is a good word with the signal I'm trying to get here.

Ryan Sean Adams:

[10:38] I think crypto, just sum up crypto, I do think we have entered the apathy market for crypto. I mean, you're not seeing headlines. You're not seeing any reaction to news. It's just kind of hopping along. And I'm mostly outsourcing my brain on what's going to happen in the cycle to Michael Nato. I think he's got a pretty good cause on it.

David Hoffman:

[10:54] Because he's been right consistently.

Ryan Sean Adams:

[10:57] He's been right. All right. So that's one of the things that's happening. So in addition to oil prices, got to look at the odds of a recession on the back of some pretty grim job numbers, David. So last week, this took investors by surprise. is we were at negative 92,000 on jobs in February and the unemployment rate is actually rising. It's been pretty low historically, but now it's 4.4%. The expectation was that we would add 50,000 to 60,000 jobs, but we were down by 92,000.

David Hoffman:

[11:27] I'm getting deja vu here. Didn't you do this last jobs report?

Ryan Sean Adams:

[11:31] Last jobs report, maybe? I thought it was like flat or healthy. Actually, I can't recall. I thought it was flat,

David Hoffman:

[11:38] Healthy, and then it corrected downwards.

Ryan Sean Adams:

[11:39] Well, so you got war, energy prices, inflationary concerns, some bad jobs numbers, right? Like what's going on there? Are employers laying people off? Are they stopping the higher? So the R word is back in vogue again. And it was again, like this time last year, we started talking about a recession. But look at the poly market for the US recession by the end of 2026. We jumped up after these job numbers all the way to like, 37% that we would get a recession in 2026. We're since down to about 30% on those numbers. But the chance of a recession, the probability of a recession in 2026 is increasing given the unemployment data, given inflationary type pressures. So we got that to watch out for as well.

David Hoffman:

[12:25] Granted, it was higher in November and looks like October of last year. It was at 45% then. So we're kind of still trending downwards, but it did spike up from 20% to 30%.

Ryan Sean Adams:

[12:38] You're right. And I mean, GDP has been pretty strong and the AI boom is still booming. But the thing maybe I am most looking at here is private credit. Have you seen some of the headlines coming into the private credit space?

David Hoffman:

[12:52] No, that was not on my timeline this week. So you're going to have to inform me.

Ryan Sean Adams:

[12:56] Adam Cochran, so Adam Cochran, it says, if you aren't in finance, this likely means nothing to you. But if you are in finance, this is one of the main barometers of the end of an economic cycle and that things are actually getting quite bad. And what he's referring to is this headline, JP Morgan marking down loan portfolios of private credit groups, okay? So this is Adam Cochran sounding the alarm bells on this.

David Hoffman:

[13:22] But I will say, if you don't know who Adam Cochran is, he is good at engagement and sounding alarm bells. That's kind of like his deal is what he does.

Ryan Sean Adams:

[13:31] Yeah, that's right. But in this case, there is some substance here. So JP Morgan is actually restricting private credit lending. So it's not lending to some of these private credit companies after some markdowns that happened on the weekend. Jamie Dimon, CEO of JP Morgan, said that there's some cockroaches out there. He's talking to private lenders that are going to, I don't know, die.

David Hoffman:

[13:54] Wait, wait, wait. Cockroaches don't die.

Ryan Sean Adams:

[13:56] I don't know what he's saying. He said there's cockroaches and there's bad connotations. Okay, David, there's some bad connotations. And this also comes on the back. Here's a Reuters article. So this happened on March 6th. So late last week, I guess. BlackRock fund limits withdrawals as redemptions rattle private credit. So what they're referring to is a BlackRock fund in the private credit industry that just said, okay, we got to cease redemptions. $26 billion lending fund. There was 1.2 billion in redemptions. And I had to call a halt on that. All redemption ceasing. And you know, when there's kind of a run on a fund or run on the bank, and that fund or bank has to say, halt, no more redemptions. That's not a great sign, is it?

David Hoffman:

[14:41] Yeah, yeah, I would agree. My next question is, if we are trying to point at this as like, oh, there's a contagion, there's a financial crisis coming, I would like to ask the size of all of this stuff.

Ryan Sean Adams:

[14:51] Yeah, that's a good question, right?

David Hoffman:

[14:53] What's the TAM here?

Ryan Sean Adams:

[14:54] What's interesting about private credit is it's been growing in the background since about, you know, post 2008 when the banks were the primary lenders here. So after they fell apart, a whole industry stepped in, private credit industry. There's groups like Apollo that you've probably heard of. They're funding many of the data centers. And they've been funding a lot of, with private credit, SaaS firms, okay? Was it like three weeks ago when we started talking about the SaaSpocalypse?

David Hoffman:

[15:19] Right. And the whole idea about why they would fund SaaS firms is because SaaS growth became such a dependable metric that you could actually project it dependably and the models would fit. And so then it's like, okay, well, if the models are working and we can project revenue and growth, then we can like lend to these companies.

Ryan Sean Adams:

[15:39] Yes. And so that's where some of the jitters are coming in. Maybe some of the SaaS companies are actually bad. And 20 to 35% of this $2 to $3 trillion industry is SaaS companies. So some of the bears like Adam Cochran are saying, well, this is the subprime bubble. Okay, the subprime credit problem of 2026. It's here. It's in private credit. These are opaque markets. You can't really trust them. They're going to go belly up. The bulls are still saying, guys, like this is normal market operations. Okay, SaaS companies down. This is just a market test. If you look at private credit, their defaults have been pretty good, like 1.9%. That's like really low historically. Nothing to worry about. It's just a market test. So it's something to keep an eye on, but I don't have any conclusions on this myself. Yeah.

David Hoffman:

[16:28] Part of the story of the subprime mortgage crisis, the 2008 financial crisis, was the collaboration between the government policy and the lending sector. And so the lending sector got out of whack because it was not responding to capitalistic incentives. Naively without understanding what's going on and just like reacting to what you're saying. The private credit market, I would suggest, would respond to capitalistic risk incentives better than the subprime mortgage crisis did. Maybe. And so it would be naturally more resilient.

Ryan Sean Adams:

[17:02] I don't know.

David Hoffman:

[17:03] But I don't know. I could just be spitting out my ass here, dude.

Ryan Sean Adams:

[17:06] Yeah, I mean, you have to keep an eye on it. And I think you have to kind of hedge in both directions here. That's probably the safe move here. move here. We got more to talk about. The Nasdaq is partnering with Kraken to bring Tesla, NVIDIA, the whole QQQ on chain. The craziest part about this is they're not doing it with Schwab or TD Ameritrade. They're doing it with Kraken. This is a very crypto native approach.

Ryan Sean Adams:

[17:29] Also, the DOJ retrying Roman Storm. We'll talk about that and the implications for privacy. Before we do, we want to thank the sponsors that made this possible.

David Hoffman:

[17:38] Breaking news out of the Wall Street Journal reported this, but also a Nasdaq press release. Nasdaq is designing a framework for tokenized equities that would allow stocks like NVIDIA or Tesla, I think really all stocks, to trade either as a traditional share or as a traditional as a blockchain-based tokens. We get both. We get both. We get both. Both versions, this is the critical feature, both versions would get the same C-U-S-I-P, the same QSIP, which I totally knew exactly what that was before I woke up this morning. What's a QSIP? A QSIP is basically a social security number for a stock. Okay. So like a- Unique identifier? A unique, a phone number for a stock. Like, you know, what's the stock? How do I identify the stock?

Ryan Sean Adams:

[18:20] What's the QSIP?

David Hoffman:

[18:20] Yeah. And so now that we have the ones that trade on NASDAQ and we need the same things to also trade on public blockchains, they need to have the same QSIPs. And that's the unlock.

Ryan Sean Adams:

[18:30] So it's all registered with the DTTC, right?

David Hoffman:

[18:34] DTCC. Yes.

Ryan Sean Adams:

[18:35] DTCC. Thank you. Got these acronyms. Yes. Right. What is Kraken's role in this?

David Hoffman:

[18:40] I'm glad you asked. Yeah. So NASDAQ does all of the stuff on the NASDAQ exchange.

Ryan Sean Adams:

[18:46] Yes.

David Hoffman:

[18:46] Kraken will be doing all the stuff on the blockchains. Ah, that's cool. They have their X-Stocks token format, like token tech stack for doing this. It started on Solana. It's now on Ethereum, Tron, Ton as well. X-Stocks is. X-Stocks is. Yeah. And so NASDAQ is just using Kraken's X-Stocks tech stack to distribute stocks as tokens on blockchains.

Ryan Sean Adams:

[19:14] Okay. Yeah. I mean, so the big winners of this, I think, in cryptos, clearly it's Kraken. And it's clearly Xdocs, which is a third party that's partnered with Kraken around this. Also, some of the chains involved, Solana, Ethereum, maybe some of the other chains that you mentioned too. Chainlink doing the Oracle stuff. So there's some winners here from a crypto perspective. Now, this doesn't roll out for another year, David. So not until the first half of 2027. So big partnership announcement. I mean, the biggest, deepest tech capital markets in the world, some of the most exciting companies in the world. But it's not going to hit us until next year. It's still... A pretty big deal. And I mean, the response was somewhat muted about it. I mean, we didn't get crypto prices doing anything on the back of this news. So again, this points to maybe the apathy market.

David Hoffman:

[20:02] Yeah. Yeah, that's right. Also, there is just a bunch of competition in this space too. So like, they're not the only ones trying to do this. Like the New York Stock Exchange has their own strategy. Robinhood has its own strategy. I haven't heard of Coinbase's yet, but you can only imagine that they've got to be brewing something up over there.

Ryan Sean Adams:

[20:17] Yeah, everyone wants to do it. This is a take. The NASDAQ just partnered with Kraken to enable 24-7 trading of tokenized stocks. Of course, that's the benefit. The craziest part is it runs on Kraken, not through traditional brokers like Schwab and TD. I guess we pointed out some of the winners. Who are the losers? It's old TradFi, Schwab,

David Hoffman:

[20:36] TD. It's anyone not doing this, yeah.

Ryan Sean Adams:

[20:38] Who are not doing this. So it's a big move. Eric Balchunas says that this is one of his big themes of the year. It's how tokenization isn't going to replace ETFs but rather distribute them. It's actually bullish. This will deliver the world's most beloved ETFs and stocks to people on chain and less developed countries. You get VOO and chill for the masses, basically. These are popular ETFs, all right? VOO. What is VOO?

David Hoffman:

[21:03] That's Vanguard, right?

Ryan Sean Adams:

[21:04] Yeah, that's a Vanguard something. I don't know what chill is, but Balchunas knows.

David Hoffman:

[21:08] No, I think he's making a Netflix and chill reference.

Ryan Sean Adams:

[21:12] I didn't get it. VOO and chill. Chill is not an ETF. I would have been all caps there. Sorry, Valchunas.

David Hoffman:

[21:20] I do. You have to give a tip of the hat to Kraken. They've had some banger TradFi-oriented announcements lately that, like, really do the whole, kind of like the DeFi mullet thing of, like, NASDAQ on TradFi and Kraken in DeFi, Nat and Kraken on chain. Kraken, yeah. And Kraken, yeah. Yeah, well, they have that app, yeah. And we know that they're gearing up for an IPO, I would assume, this year. And so they've been like teeing up a pretty good, like pretty weighty announcements ahead of their IPO.

Ryan Sean Adams:

[21:52] You know Kraken's going to want to go on the NASDAQ and like tokenize themselves, right? And then, you know, obviously have their own tokenized stock. Wow. Very recursive play. That'd be fun. That'd be fun. Why not do that?

David Hoffman:

[22:02] Can you tokenize the stock and then can you go backwards? Can you keep on looping it?

Ryan Sean Adams:

[22:08] I don't know. We got more talk about this later in the episode about actually crypto native tokens going back and tokenizing themselves and going from on-chain to off-chain.

David Hoffman:

[22:17] No, no, no. Equitizing, securitizing themselves into equity.

Ryan Sean Adams:

[22:23] What I'm saying is the bridge is going two ways here in all places. Let's talk about some bad news, though. The DOJ announced on this week that they are going to retry the Roman Storm case.

Ryan Sean Adams:

[22:36] David, recall for us the Roman Storm case and the first time this went around. What happened?

David Hoffman:

[22:41] Roman Storm, open source developer of Tornado Cash, the privacy mixer, which got added to the OFAC sanctions list. First ever technology non-entity that was ever added to the OFAC sanctions list because North Korea and other adversaries were using Tornado Cash to launder money. Uh roma storm got charged for building it despite being totally out of his control because it's autonomous a bit of software that trial happened in august of 2025 a federal jury convicted storm on one count, conspiracy to operate an unlicensed money transmitter business, which of all the counts was the least serious one from a Roman Storm perspective. So that's like the least serious one. He gets to go home and hang out with his daughter. That's good.

Ryan Sean Adams:

[23:28] And he still wanted to appeal that, right?

David Hoffman:

[23:30] He still wanted to appeal it. Yeah. But it's the most serious one as it relates to crypto and DeFi because it implies that open source developers can be money transmitters. Right. The jury deadlocked on money laundering and sanctions violations. And so that's good. So that's what happened. Now, the DOJ has proposed an early October retrial, even as Roman Storm's existing conviction is being challenged. So there are two retrial counts, conspiracy to commit money laundering and conspiracy to violate IEPA sanctions. Same things that they did once before. And Roman Storm faces up to 40 years if he is convicted on these, plus five years for the prior conviction.

Ryan Sean Adams:

[24:11] So this is incredibly disappointing news because it was completely optional as to whether the DOJ would retry this or not. The first time around, it was a jury of 12 Americans, four weeks of evidence, and they came away with a hung jury. It was deadlocked, right? And so they could have just stopped. They didn't have to retry Roman on these counts. So this is Roman in his own words tweeting this out. And he's giving a history here. He's saying some things that have happened since the original court case. Donald Trump declared that the war on crypto is over. The attorney general in a memo, a DOJ memo, said that they are not a digital asset regulator and they wouldn't target mixers for end user accounts. The U.S. Treasury, you know you're talking about it being on the sanction list, Tornado Cash, they removed Tornado Cash contracts from the sanction list entirely. Treasury in March 2026, that's just this month, said that lawful users of digital assets may leverage mixers to enable financial privacy. So we thought we were in the clear with this administration that they were calling off the dogs and they were just, you know... Being much more open to open source privacy developers, but it appears not. And one of the people leading this war is actually, do you remember the pre-Gary Gensler who he was? Jay Clayton.

David Hoffman:

[25:29] Say his name. Jay Clayton.

Ryan Sean Adams:

[25:32] Jay Clayton.

David Hoffman:

[25:34] Bad man. He's a bad man.

Ryan Sean Adams:

[25:36] He is not proving himself to be a friend of crypto. So there's a story actually in Bankless about some of his history. So Jay Clayton is now the U.S. Attorney General for the Southern District of New York. He's leading the charge here. He's the guy who is deciding to re-prosecute. He was the guy who decided to prosecute the first time. He also brought the Ripple lawsuit together when he was back at the chair of the SEC. Not only Roman Storm, the Samurai Wallet developers. He's doing all of this and he's a Trump appointee despite Trump's pro-crypto rhetoric. Yeah. So there's a problem here in terms of how can you be the crypto capital of the world when you're prosecuting an open source software developer?

David Hoffman:

[26:18] Who's Jay Clayton's boss? Who's telling him to do these things or giving him the leash to do these things without being checked on by at least the rhetoric of the president? Yeah.

Ryan Sean Adams:

[26:30] He's a Trump appointee. So you'd imagine he's he's plugged into that whole apparatus. Right.

David Hoffman:

[26:35] Which has he not gotten the memo?

Ryan Sean Adams:

[26:38] I don't know. Or maybe there's a public memo of things that the administration, people in the government are saying. And there's another insider memo of like what you are actually going to do. I mean, watch what they're doing, not watch what they say.

Ryan Sean Adams:

[26:51] Another thing that came down the pike this week related to this is Treasury dropped a report. So do you recall Congress as part of the Clarity Act, they actually asked Treasury to weigh in on AMLKYC and market surveillance and privacy mixers. They actually mandated as part of the Genius Act, they said, Treasury, hey, go write a report about this. Well, Treasury went and they published a report this week. And some people in crypto saw some language in the report and started celebrating it. So this is Bitcoin Magazine. They were praising that this report said that lawful users of digital assets may leverage mixers to enable financial privacy when transacting through private blockchains. A big win for privacy, they said. And it is true in this report, Treasury is acknowledging that there are non-lawful uses of privacy mixers, but there's also, they've acknowledged there's lawful uses of privacy mixers. And that's something the Biden administration never did. They were like, oh, privacy mixers, got to be criminal, got to be bad. Didn't even acknowledge that there could be American citizens that are just legitimately using these services for privacy on chain. That is the good part. But honestly, David, if you read the report, the rest of the report is kind of bad.

David Hoffman:

[28:08] What do you mean? In what way?

Ryan Sean Adams:

[28:11] Well, in the way like it is suggesting that we regulate privacy mixers under the Patriot Act. In fact, it's suggesting another special measure under the Patriot Act to be targeted non-custodial software. talking about the creation of subtypes of the BSA, the Bank Secrecy Act, targeted at DeFi services.

David Hoffman:

[28:34] We don't want the BSA and DeFi to be all together.

Ryan Sean Adams:

[28:38] It's a different thing. It's a Bank Secrecy Act. DeFi is not a bank, right? To rescind, modify, or update. There was some guidance, actually, in 2019, FinCEN guidance that specified that if you were a non-custodial software developer, you're not a money transmitter. They said that to us. And that was a pro case in the Roman Storm case. Well, this is saying that we should modify that in certain ways. It wasn't really reinforcing this. And also generally recommending that we use AI for data surveillance of DeFi protocols and that we have digital identities for DeFi protocols in place that effectively do the AML KYC thing. So it's not great for crypto privacy and this is coming out of the treasury. So there's really a question in my mind as to You know, when we're talking about America being the crypto capital of the world, what do we mean by crypto, actually? You remember this Ben Hunt kind of argument where he came on Bankless, his previous podcast guest, and he said, look, the nation state's never going to actually allow you to have real self-sovereign crypto, private crypto.

David Hoffman:

[29:43] Yeah, they're not going to let you do the badass cypherpunk things. They're going to let you have the crypto Disneyland stuff.

Ryan Sean Adams:

[29:50] That's right. The shrink wrap crypto. He called it crypto TM, right? Trademark crypto and i do feel like this administration is giving us a lot of great things with respect to kind of the the crypto tm stuff like the stuff that wall street is cheering on right so

David Hoffman:

[30:05] The democrats were like we're gonna ban you guys and we'll just ban the whole thing i think what you're saying is like well the the donald trump administration is like we get to have everything that we want shrink wrapped and put behind wall street as products that's.

Ryan Sean Adams:

[30:20] Right The crypto TM, right? So we got the CFTC and Wall Street, all that. And that's good. That's great. We got stable coins. That's great. We got custody crypto. They're big fans of that. They're a big fan of ETFs. DeFi, this has been kind of, they've called off the dogs largely on DeFi. But when it comes to privacy, when it comes to self-sovereign crypto, I think what's coming out of treasury is a no. And the evidence for that is they're continuing to prosecute Roman Storm. How can you be the lowercase c crypto capital of the world if you're still doing that? Maybe better than the Democrats, maybe better than the Biden administration, but we're still not getting what we need on the crypto side of things.

David Hoffman:

[31:02] It is because it's privacy, because it's a mixer. It is not just open source developers, but it is like going up against what I think the nation state would say, like a national security threat versus individual freedoms. And when you take the judgment of the nation state about a nation state security threat, the judgment is always gonna be like, well, it's a threat and we need to ban it. And it takes a very noble politician and a very noble leader to preserve the rights of individual freedom and autonomy and privacy over the nation state because inherently the nation state is always going to protect itself.

Ryan Sean Adams:

[31:42] It takes people like the founding fathers and, you know, digital bill of rights, a bill of rights, you know, to give give civil liberties to the people and to

Ryan Sean Adams:

[31:49] trust them with those civil liberties. So I guess we're not there yet, but we will see. There is a link we'll include in the show notes. If you'd like to donate to the Roman Storm cause, please do so. You need some legal support and those funds will help.

David Hoffman:

[32:02] We have to do this all over again. Yeah. But then we get crypto and we get to keep it. And it's the Wild West free, open, public permissionless version of the thing. Not the thing that just gets wrapped into a product wrapper and distributed on Wall Street.

Ryan Sean Adams:

[32:16] And he could fully win in court this time. So that is the hopeful case. Coming up next, we got best friends forever. Mike and Paul from the SEC and the CFTC. They're working on Project Crypto. Also, BlackRock releasing their ETH staking ETF. David, I know you've investigated the details on that. I want to hear about them. And then Bernie Sanders and the moratorium on AI data centers.

Ryan Sean Adams:

[32:38] What is this anti-tech backlash and where will it lead? All that and more. But before we get there, we want to thank the sponsors that made this possible.

David Hoffman:

[32:46] Ryan, this picture just warmed my heart. This was one of the most heartwarming things I've seen on the timeline for the podcast listeners. We have just a very hearty Mike Selig. Bromance. Mike Selig, the new chair of the CFTC, giving a nice firm handshake to the SEC chair, Paul Atkins. And they just look overjoyed. They just look like they're about...

Ryan Sean Adams:

[33:09] This would have never happened with Gary Gensler. No. Who was the previous year?

David Hoffman:

[33:13] In the Gary Gensler era, Gary tried to encroach on the CFTC territory. I can't remember what it was about, but he did this. And then the CFTC had to plant a flag, being like, Gary, back off.

Ryan Sean Adams:

[33:24] Get off our back. Not everything is a security.

David Hoffman:

[33:27] Yeah, exactly. So Paul Atkins tweeted out, The era of turf wars, duplicative registrations and differing regulations between the SEC and CFTC is over. By aligning regulatory definitions, coordinating oversight and facilitating data sharing, Chairman Selig and I will ensure we deliver the clarity that market participants deserve. This is, I think if you're a fan of small government, you're a fan of this. Because this is ideally two agencies doing more with less, with more than what they have. There's been a broad question of like, why do we have the SEC and the CFTC? Why can't we just have one big markets regulator? This is something that we asked Chair Selig when we had him on the show. Yeah. And his answer is like, well, if we can just collaborate, that's basically the same thing.

Ryan Sean Adams:

[34:12] Basically the same, yeah. It's two departments toward the same set of goals, names.

David Hoffman:

[34:16] Exactly. So what actually officially happened, other than a picture of a handshake being tweeted out, is that the SEC and CFTC issued a Memorandum of Understanding, which is essentially like a formal playbook on how the two agencies will do all of the stuff that they need to do. Sharing information, joint operations, common definitions, streamlined rules. It's basically like a tweet of friendship.

Ryan Sean Adams:

[34:41] I know, but this should have been the way it was always set up to be, right? Like the fact that, I mean, it's great, I'm glad, but this is basically an announcement that, hey, government's going to be more functional now. We're going to stop doing silo turf wars. It's great. You should have always been doing that, but I'm glad that's happening now. It's great. But they are going to work together very closely. We heard from Mike Selig earlier this week on the Bankless podcast that they're hand-in-hand with Project Crypto as well. And that's going to be an area of close collaboration, which is very needed.

David Hoffman:

[35:11] Let's get into the BlackRock Staked ETH ETF. So Ryan, what is the ticker for the first BlackRock ETH ETF? Do you want to remember what it is?

Ryan Sean Adams:

[35:20] ETH A, right?

David Hoffman:

[35:20] ETH A, yeah. Now we got ETH B.

Ryan Sean Adams:

[35:23] Okay.

David Hoffman:

[35:24] We got ETH B. So ETH A is if you want ETH unstaked, ETH B is if you want ETH unstaked. Is if you want Ether staked.

Ryan Sean Adams:

[35:31] Why would I want ETH A when I can get ETH B?

David Hoffman:

[35:33] That's a good question. If you are holding ETH A in your brokerage, you might want to consider transitioning to ETH B. You definitely don't have a tax liability because ETH price has definitely gone down since.

Ryan Sean Adams:

[35:44] Oh, that's true. That's true.

David Hoffman:

[35:45] So you can- But that is.

Ryan Sean Adams:

[35:47] I should say for our tax listeners, of course, those are two separate assets. So that will be a taxable event.

David Hoffman:

[35:52] That will be a taxable event. Yeah. But it could be a tax loss harvesting event.

Ryan Sean Adams:

[35:55] Yeah. Nice.

David Hoffman:

[35:57] Okay, so how does it actually work? The reason why we haven't just been able to get this out the door is you actually just can't naively have a 100% staked ETF.

Ryan Sean Adams:

[36:09] That's right.

David Hoffman:

[36:09] Because of the withdrawal queue, because doing redemptions is difficult. It's actually kind of one of the problematic components of the Ethereum protocol. You sit in a queue.

Ryan Sean Adams:

[36:17] Potentially. It depends on how many other stakers are withdrawing at the same time. That queue has been as long as like 30 plus days.

David Hoffman:

[36:24] 40 days. 48 days, I think, was the longest. It's no longer that high now, but the problem is, is like BlackRock, when they create this legal structure, this entity, this asset, they need to account for all possible risks. Yeah. This is one of them. And so the way that they solve this is that it's just 80% staked, 20% vanilla. Okay. And so they have a 20%, what do they call this? A liquidity sleeve that targets between 70% and 95% of its ETH to be staked under normal market conditions. The remaining 5% to 30% is kept as a liquidity sleeve, and that allows for redemptions.

Ryan Sean Adams:

[36:59] So that means you're not getting the full staking yield.

David Hoffman:

[37:01] You're not getting the full stuff. And in addition to only 80% being staked, there is also 18% cut of the yield. And so for every dollar of staking rewards that the asset earns, BlackRock and Coinbase and some of the validators take 18 cents. And so if you are staking ETH yourself the bankless way at home, doing your duty to Ethereum, you are receiving like 3.5% ETH yield. If you do it in ETH B, the banked rate is 2.87%. So that is your cost of convenience for you if you do the BlackRock ETH B.

Ryan Sean Adams:

[37:40] It's great that this product is now available, right? So this is kind of more of the internet bond type meme. It's something that Bitcoin does not have. So maybe that's going to be attractive to some investors. We got two ETFs to play around with.

David Hoffman:

[37:54] Yeah. I would like to take a victory lap here, Ryan, where I previously said that I do not think the staked ETH ETF will be all that bullish. And I do. I think if you go look.

Ryan Sean Adams:

[38:05] At the ETH price. Well, if it happens in a bear market,

David Hoffman:

[38:06] David, come on. If you, ETH price did not respond to this news.

Ryan Sean Adams:

[38:10] Yeah, not at all. Not at all. Just shrugged it off. That happened today though. So it's a pretty big deal in the background. David, a trend to watch. Are DeFi tokens turning back into US securities? This is a proposal from the ACROSS protocol. Can you tell us about this?

David Hoffman:

[38:26] So Risk Labs, which is the team behind ACROSS, did a temp check. This is a temperature check. They're just putting out a feeler about, hey, how do you guys feel about these things? about the possibility of migrating the DAO token structure to a USC corp, which would hold the protocol IP and run all operations. So there's a couple different options.

Ryan Sean Adams:

[38:45] What is, for people who don't recall, what is a CROSS?

David Hoffman:

[38:48] It is a bridge protocol is what people know it as. It's an intense space bridge protocol. So I use across to hop from chain to chain. It basically happens in the background now at this point, but it is a interoperability protocol basically. Okay. So there are two options for ACX holders. One would be a ACX token to share conversion. So you would hold your tokens and then it would just convert to equity, which is kind of cool, but problematic. U.S. Investors who are not accredited or have under 5 million tokens will need to get accredited investor status. So, small corollary there.

Ryan Sean Adams:

[39:28] But this is the cross protocol going from a DAO and a crypto-native token, essentially, to a private U.S. C-corp. This is a temp check about that.

David Hoffman:

[39:40] This is a temp check about that.

Ryan Sean Adams:

[39:41] But if this happens, that's what the proposal effectively is. You go from a token to a private shares in a C-corp and kind of a one-to-one split or one-to-one redemption here.

David Hoffman:

[39:51] Yeah. The second option that ACX holders has is they just get a buyout at something that's like 25% premium to the price, which is why the price pumped.

Ryan Sean Adams:

[39:59] The proposal claims- The price did pop too. Look at this.

David Hoffman:

[40:02] Yeah, it did pop quite a lot. It went from $25 million market cap to a $45 million market cap FDV. The rationale that Hart, the founder of Across, he just says it is just like, We just need to have a centralized entity. The DAO token thing makes things difficult for us. We need enforceable contracts. We need a clear legal counterparty. We need structured revenue agreements. We need a C-Corp. We need a C-Corp.

Ryan Sean Adams:

[40:26] That's painful, right? It's sad. I totally get it. So one thing, like my take on this when I read this is first respect to across protocol for like optimizing for the best interests of token investors. Okay. Yeah. A lot of other crypto projects were just like cut and run or rug the token holders. You didn't have any, you know, investor protections or rights anyway. Ha ha. And Cross is not doing that, right?

David Hoffman:

[40:48] So, kudos to them. Ryan's just, you know, pat and pump in the back of his fellow Canadian.

Ryan Sean Adams:

[40:53] Yeah, yeah, that's right. And Heart, the team is fantastic. They've been doing a great job.

David Hoffman:

[40:59] Good ice climber.

Ryan Sean Adams:

[41:00] This is, oh yeah, you've ice climbed with Heart, right? Okay, so this is sad though. I feel like this is sad for our tokens because we're going in the wrong direction.

David Hoffman:

[41:09] No, guys, wait, wait, wait.

Ryan Sean Adams:

[41:11] Which way are you going? Yeah, I thought like DAOs and tokens and more useful capital was going to come on chain. And now we're going from on chain to off chain. And what Hart basically said was having a token generally hurts more than it helps. I think he's right. I mean, even look at the token price, David, like over time. It is just like, you know. Not that chart. Yeah, it's down.

David Hoffman:

[41:32] Yeah, the price pump that you see, it doesn't really look like one when you zoom all the way out.

Ryan Sean Adams:

[41:36] I mean, so there is a discount right now that the market is placing on tokens. And I think they're discounting them because they're realizing tokens don't have investor rights, don't have good alignment, aren't solving principal agent problems. There's no fiduciary responsibility. So the market is just flat out discounting all of our DeFi tokens, right? So who would want to be a token in this environment? If you're an investor, you don't necessarily want to be a It's a little sad because I feel like we're ceding ground. One day, maybe we fix these things and we start putting more capital assets on chain. This is not that day. I wonder if almost the route is like, okay, so across becomes a private C corp. Maybe it goes public at some point or something. And then it comes back on chain. Is that what we have to do as a tokenized real world asset?

David Hoffman:

[42:23] Yeah, but it won't be permissionlessly purchasable. Like it would be an equity on chain. And we want equities on chain, but we don't want our tokens to turn into equities. We want our tokens to be even more investable of an asset than equities themselves. And equities have a lot of things going for them as an investable asset. They are literally assets that are meant to be invested in. And tokens... Aren't not that, but they aren't purely that either. And there's a lot of encumbrances that tokens have. And we need to find ways to make tokens even better than equities.

David Hoffman:

[42:58] And that's a very hard thing to do.

Ryan Sean Adams:

[43:00] Well, today is not that day. We're not doing it yet. We got some more work to be doing in that space for sure. This was some news coming out of Polymarket that you were excited about. A partnership with Palantir?

David Hoffman:

[43:11] Yeah. Yeah. Okay. So this is odd. So it reads odd, but it actually makes a ton of sense when you look into it. So Polymarket from Shane tweeted out that they are excited to announce a partnership with Palantir and TWGAI to build the next generation of sports integrity market platforms. So like what's going on here is like, why the hell is Polymarket and Palantir working together?

Ryan Sean Adams:

[43:34] Yeah.

David Hoffman:

[43:34] What does Palantir do that's relevant to Polymarket? Palantir provides data infrastructure and surveillance capabilities. So, like, large-scale data integration and anomaly detection built originally for the government to, like, surveil the world, but now they are applying it on ingesting trading data and flagging suspicious patterns in real time. Basically, insider trading or shenanigans going on on the prediction market using Palantir's capacity. What is TWGAI? Glad you asked. TWGAI is the intelligence division of TWG Global, who I also didn't know what this was. TWG Global is a massive conglomerate with a huge sports portfolio. So they own majority stakes in the Lakers, the Dodgers, the LA Sparks, Chelsea Football Club, Cadillac F1.

David Hoffman:

[44:26] TWGAI is their AI arm that specializes in financial services and sports analytics. And so they already have built AI software stuff for finance and insurance and so you put these things together and you have this portfolio of people that own all the sports stuff and then you have Palantir which can help do market integrity create market integrity in Polymarket and then you have Polymarket which is trying to foster just a very large sports economy on its prediction market platform and so when Shane tweeted this out he tweets out the current state-by-state regulatory password for sports prediction market is broken, this partnership builds integrity infrastructure from the ground up at the federal level using Palantir and TWG to establish market trust and make the case that prediction market regulation belongs at the federal level, not fractured across states. So it's a combination of user protections for market integrity while also advocating that if we were regulated piecemeal by the states, we would never be able to do this in the first place.

Ryan Sean Adams:

[45:26] Yeah, I guess I was wondering how they're going to solve these problems of identifying insider trading and stuff like that. It seems like what they're doing is they're throwing AI at it.

David Hoffman:

[45:34] They're AI and data.

Ryan Sean Adams:

[45:36] Yeah, and trying to figure that out. Let's talk about another AI subject, and this is Bernie Sanders, who does not like AI. Let's play a clip.

David Hoffman:

[45:45] Thanks very much for joining me. I will soon be introducing legislation calling for a moratorium on the construction of new data centers. Now, as a result, I've been called a Luddite, anti-innovation, anti-progress, pro-Chinese, among many other things.

Ryan Sean Adams:

[46:03] This is a whole nine-minute video, but Bernie Sanders is writing a bill, a championing bill in Congress to call for a moratorium on the U.S. Building new data centers. And he goes on as to why. He talks about the job loss, obviously, that will affect Americans. He talks about mental health problems that AI is causing. He talks about the energy use, of course. He talks about the billionaires who are going to make the majority of wealth on AI and leave the rest behind. And he also has some like AI doomer type themes too. You saw a clip last week of Bernie Sanders meeting with some of the decelerationist folks, the effective altruist type folks like the Eliezer Kowskis of the world. And he talked about loss of control, that maybe AI could kill us, that it's a safety issue and worried about effects and outcomes of human life. So it's all of these narratives combined and Bernie Sanders is leading a campaign to stop AI data center building. And I think, David, this is a backlash that is going to gain a lot of steam in the U.S. And it might be the issue, one of the top three issues deciding the 2028 election as well as it's going to surface during the midterms too.

David Hoffman:

[47:25] In terms of a just a persuasion piece, this video, nine minutes, 40 seconds, a fantastic job, like just a good argumentative piece of content.

Ryan Sean Adams:

[47:35] You think so?

David Hoffman:

[47:36] Yeah. Like, I don't agree with it, but he's doing the job that he needs to do. There's like three or four minutes of it where he's just quoting from tech billionaires about all the ways that AI is going to disrupt the economy. And he's like, Dario Armadi says it's going to replace all the jobs. Yeah. And these are his words. These are the tech leaders who are like Mark Zuckerberg, the second richest person in the world, said this. And so he takes the same rhetoric that we know from Eliezer Yudkowsky that we experienced on the podcast when we had him on. He does the Bernie Sanders spin on it of it's going to disenfranchise the bottom half of the population. And it's going to make all the very rich people, Elon Musk, Mark Zuckerberg, Sam Altman, it's going to make them even more rich. It's very populist. It's very decelerationist. There's a very strong growing alliance between the decelerationists and the leftists.

Ryan Sean Adams:

[48:30] But it's also, David, it seems to be a popular opinion. I mean, this is the NBC poll showing that AI has worse poll numbers than ICE. So AI is even less popular in the U.S. than ICE. Only two things are even less popular. One is the Democratic Party. Oh, no. The other is Iran. Okay, but, you know, it's, let's see here, total negative. Is 52% total positive, sorry, 46%, total positive 26%. It's only as 26% of US citizens who are positive on AI. I mean, I think Bernie is just capturing this popular sentiment wave, which is a lot of Americans are scared of it. They don't like it. That makes them feel uncertain. And that's going to turn into votes.

David Hoffman:

[49:19] Yeah, yeah. The political divide, in my mind, is going to be determined by... Like global leftist decelerationists and techno-nationalist accelerationists.

Ryan Sean Adams:

[49:34] I guess.

David Hoffman:

[49:35] And I think that is a framework that I think has been useful to me, and I kind of expect that to go forward.

Ryan Sean Adams:

[49:41] Yeah, I think one of my concerns about this is basically when you start to say moratorium on AI data centers, you're kind of saying moratorium on tokens, AI tokens. You're saying moratorium on intelligence. You're saying slow down on a lot of things, like slow down economic growth, slow down the affordability of a key set of services around healthcare and therapy and legal services, a slowdown of America relative to other countries, a slowdown potentially of tax revenue that the GDP of this industrial revolution could create. It's like a real decelerationist take. And it's very different to me than the left of the 1990s, which was like kind of the Bill Clinton Democrat, uh, democratic left, which, um, they, their, their take was like, um, The economy can boom. Tech can do really well. Everyone can do really well. We're just going to take a larger portion of taxes to fund our social programs, right? This approach is much more decel, right? It's like, that's not good enough. What we're actually wanting to do is decelerate the growth here, slow progress, almost freeze things in time.

David Hoffman:

[50:53] Yeah, we don't want to tax it. We don't want it fundamentally.

Ryan Sean Adams:

[50:56] So I do think that this binary is being created, the one that you kind of described, which is like the decel kind of side of things versus the accelerationist side of things. And they're both really pulling against one another right now. And it's a political issue. It might be the political issue of the next four years into the presidency.

David Hoffman:

[51:18] Yeah. AI obviously has mainstream awareness. Only, I think like less than 1% of people in the United States actually pay for AI. So there's still a lot of penetration left to do. but you can imagine by the time the 2028 election comes around that's two and a half years from now. You know how good AI is going to be in two and a half years? There will be actual real job disruption by then not just like the fake AI doomer porn stuff that we're seeing on Twitter.

Ryan Sean Adams:

[51:44] Yeah, so I guess watch for that. I think it's going to roll downstream into crypto because if you're anti-tech for AI then you're probably also going to be anti-crypto policy and we might be starting to see the early signs of a political backlash on all this. We'll have to navigate it as we do every week on Bankless. Thank you for joining us. Of course, got to let you know, none of this has been financial advice. Crypto is risky. You could lose what you put in, but we are headed west. This is the frontier and it's not for everyone, but we're glad you're with us on the Bankless journey. Thanks a lot.