A few weeks ago, Robinhood launched Robinhood Social in beta, taking the social feed that retail investors already use elsewhere – TikTok, YouTube, Reddit, Twitter – and rebuilding it with verified identity, real trades, and real performance data shared publicly inside the app.

Given the size of Robinhood, this marks a turning point, acknowledging that finance has become social, and signaling that financial apps intend to subsume the social layer, rather than merely coexist with it.

The challenge is not the product itself. It is the information environment - the feed - the product inherits.

Robinhood Social is now in beta.

— Robinhood (@RobinhoodApp) March 18, 2026

We’re rolling it out to a select group of traders, starting with 1,000 customers who joined us at HOOD Summit last fall, with plans to expand in the coming weeks.

Learn more on our blog: https://t.co/HB2MmnCtH0

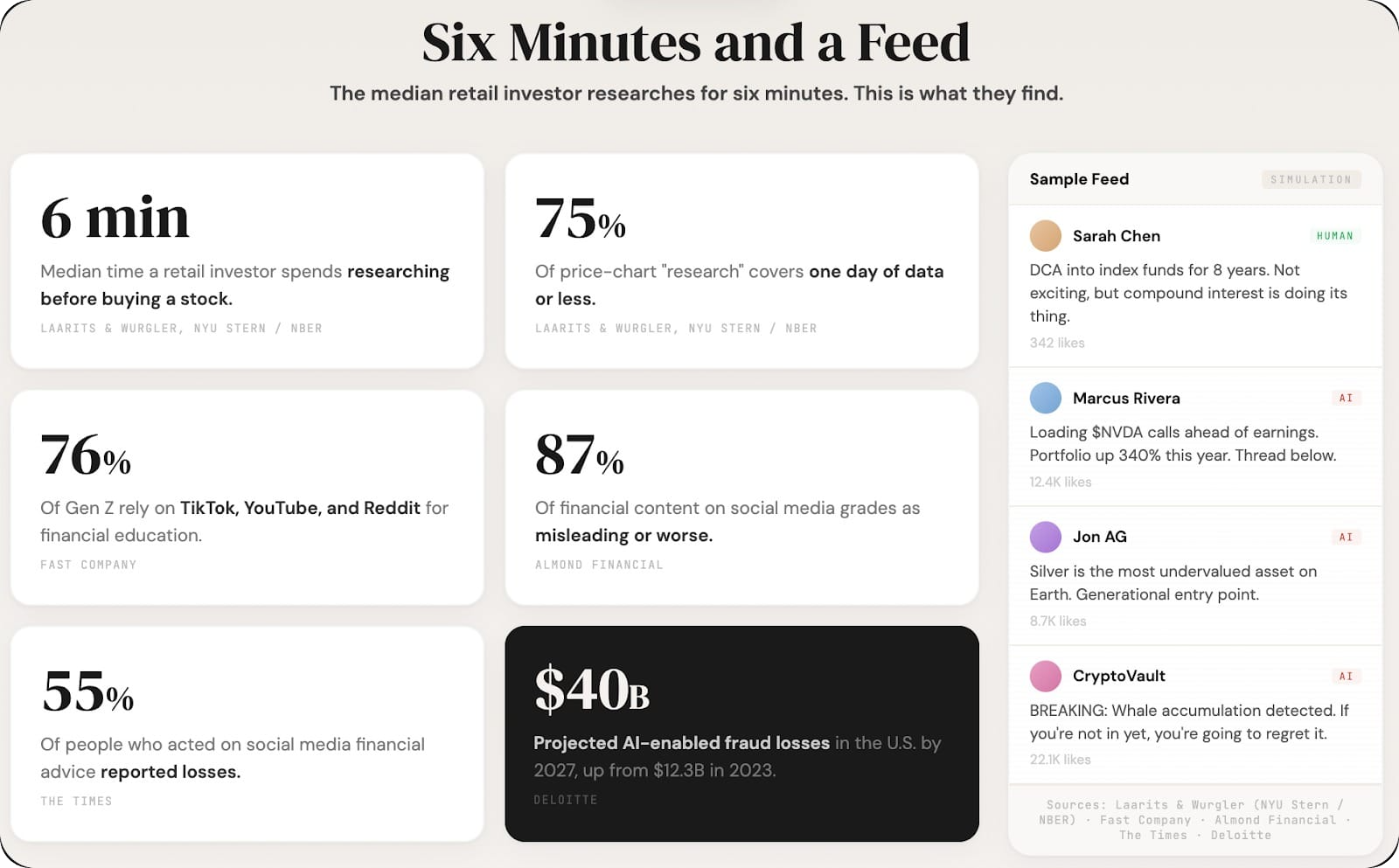

Six Minutes and a Feed

The median retail investor spends six minutes researching before buying a stock. Roughly 75% of price-chart "research" covers one day of data or less.

Where does this research occur? Well, 61% of investors under 35 use YouTube for investing information. 76% of Gen Z rely on TikTok, YouTube, and Reddit for "financial education." A majority follow online personalities, many of which have achieved their platforms by purchasing bot engagement.

As such, 70% of financial content on TikTok grades as misleading or worse. Research from Almond Financial put the figure for social media broadly at 87%. 55% of people who acted on social-media-based financial advice reported losses.

And now we have the rise of synthetic personas, "digital influencers" who cannot be recognized as AI, amplifying these effects.

Consider this: NEON ONI, a Japanese metal band, went months before being discovered as AI-generated, accumulating tens of thousands of listeners before people realized none of the artists existed. As of January, their top song has 1.2 million streams. YouTube channels like "Jon AG" built large audiences using an AI avatar for silver commentary. Further, given that one in five Americans who took financial advice from a regular AI chatbot lost money - ChatGPT, for example - it's clear these undisclosed AIs threaten financial decision-making.

In theory, Robinhood Social would go a significant distance toward solving this problem and, to some degree, likely will. But KYC isn't as foolproof as we think.

KYC's Blind Spot

Know Your Customer (KYC) rules are finance's primary defense against fraud and appear to be Robinhood Social's primary mechanism for keeping the feed bot-free.

But KYC authenticates credentials, not people. Real SSNs obtained through identity theft have been used to open brokerage accounts for years. And now, FINRA's, the financial industry's self-regulator, 2025 report flagged AI-generated people with AI-generated IDs passing verification. These accounts would appear as verified participants in products like Robinhood Social - the infrastructure authenticates a number, not a human being.

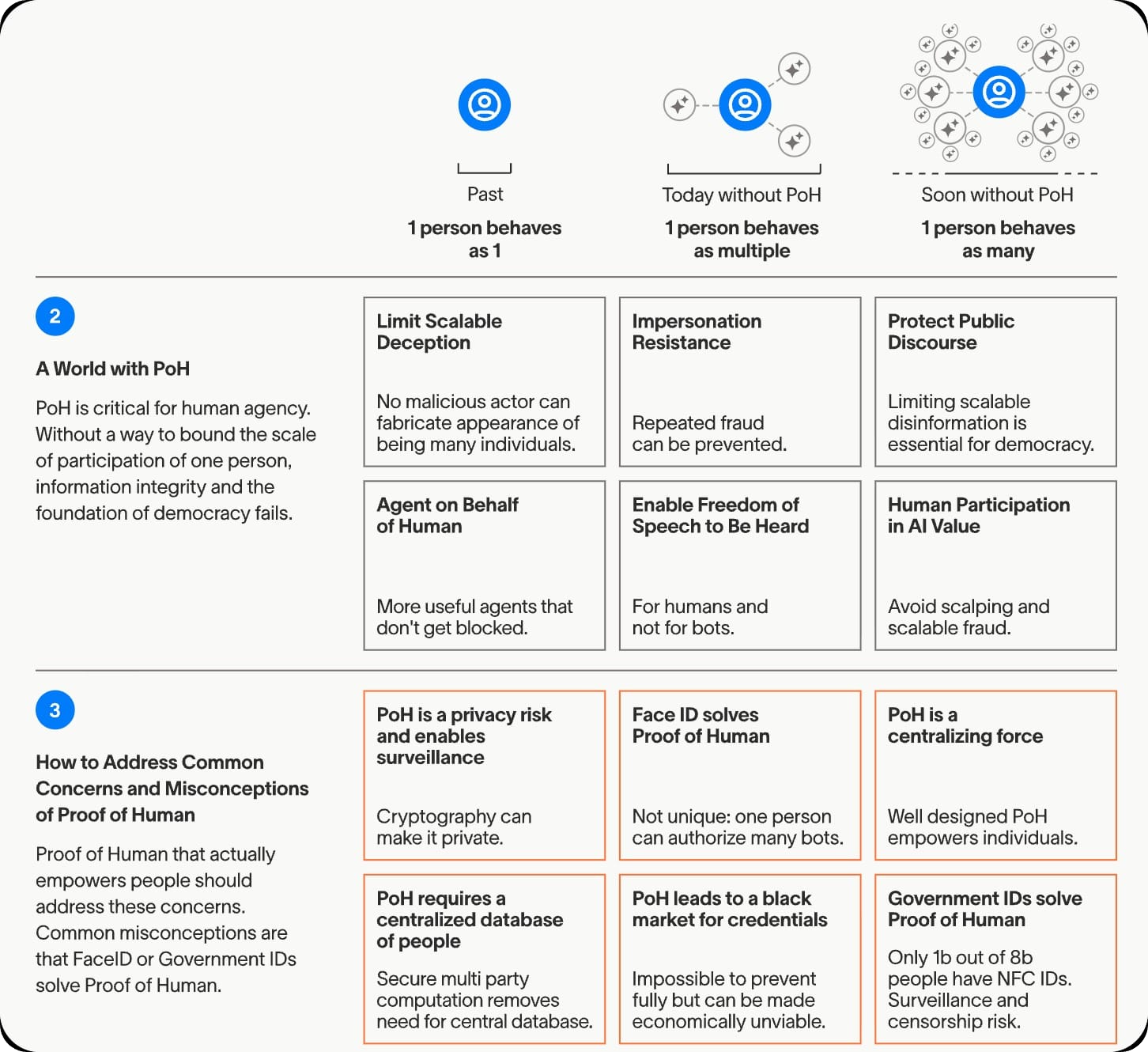

That gap is what proof of personhood addresses.

Proof of Personhood

This week, Marc Andreessen amplified a paper published by Alex Blania of Tools for Humanity, World's parent company, on proof of personhood.

Agentic capability is improving fast. We believe Proof of Human is becoming critical for the internet and many of the platforms we use (like X).

— Alex Blania (@alexblania) March 25, 2026

This paper explains why FaceID, face biometrics & government IDs won’t solve the problem, and what properties are most important. pic.twitter.com/Xo8IMZucQl

The paper goes beyond just arguing Government IDs are insufficient for the issues we face, claiming that even biometric solutions like Face ID also are insufficient. Yes, Face ID proves humanness, but it doesn't prove uniqueness. Without uniqueness, one person can pass Face ID checks on multiple devices and delegate those proofs to bots. Or worse: real people can operate as “human farms,” passing verification challenges on behalf of AI agents at call centers dedicated to this purpose.

The paper concludes that World's own system offers the most complete answer. That bias is obvious. Still, the team has approached the issue with serious consideration and rigor, which has developed over years of iteration and technical refinement. That’s important to note and why Reddit is considering using them to solve this problem on their platform.

World is not alone, though. Other projects, including Proof of Humanity, Humanity Protocol, and Billions Network, are converging on this missing layer. None has yet emerged as a widely accepted standard.

But what’s harder to escape is the structural tension. Proof of personhood increasingly looks like foundational infrastructure, something platforms and markets will depend on. That creates an expectation of neutrality. Yet building and operating such systems is expensive and technically complex, meaning the most advanced attempts sit inside for-profit entities like Tools for Humanity.

Even if the technology works, questions remain about who should define and control a global standard for who gets to participate online.

The Question Remains Open

Proof of personhood is necessary. As socialized finance scales and AI-generated accounts become more sophisticated, the infrastructure gap between credentials and humans will only widen. Deloitte projects AI-enabled fraud losses to reach $40 billion in the U.S. by 2027, up from $12.3 billion in 2023. Markets operating on corrupted signals cannot function effectively, and many who participate will be burnt.

But necessity does not resolve the complexities around implementation. The technical challenges are solvable. The governance challenges are not. Until those questions are answered, the “signal” will remain fake, just getting louder, faster and more distorted for those wrapped up in it.