Liquity Embraces NFTs in V2 Stablecoin Upgrade

Liquity, the DeFi borrowing project behind the LUSD dollar stablecoin, published its new codebase ahead of the platform’s upcoming V2 protocol release. The code revealed a slew of new upgrades, including a shift to managing LUSD borrow positions as NFTs.

The big picture

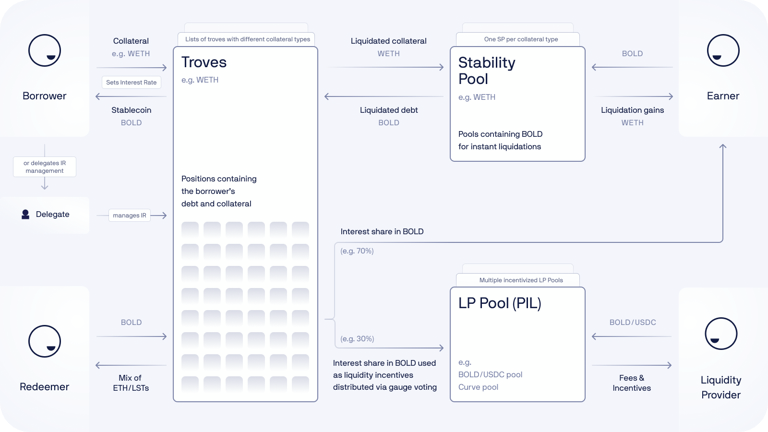

Liquity lets you borrow interest-free LUSD loans against ETH in “Troves,” a.k.a. collateralized debt positions (CDPs).

With Maker’s recent Sky Protocol rebrand marking an expansive pivot away from the popular DAI stablecoin, many DeFi users are hungry for a solid, simpler alternative for their decentralized stablecoin needs.

Liquity V1 and LUSD are battle-tested and have worked well so far, so the optimized V2 system is aimed at building in parallel to V1 to create a next-gen decentralized stablecoin ecosystem that can win market share from incumbents like DAI.

The latest

Liquity V2 introduces new features like user-set interest rates, multi-collateral support, and native stablecoin yield generation, alongside enhanced LQTY staking. With Protocol Incentivized Liquidity (PIL), stakers in V2 can strategically direct protocol revenue anywhere onchain while earning ETH and LUSD from Liquity V1.

The V2 protocol also debuts BOLD, a new stablecoin that will live on Ethereum, with several teams already preparing to deploy the V2 across multiple EVMs and Layer 2s (L2s) to promote further liquidity for BOLD.

Why it matters

- Liquity V2’s user-set interest rates allows borrowers to actively manage their redemption risk in a way that mimics the flexibility of traditional money markets, but with full decentralization.

- This will create a dynamic interest rate market where risk-tolerant users can optimize for capital efficiency, while more conservative borrowers can pay higher rates for added security. This approach, paired with support for multiple collateral types like ETH and liquid staking tokens (LSTs) like stETH, will offer borrowers more control and adaptability than in V1.

- The new BOLD stablecoin doubles down on USD peg stability without relying on governance or centralized collateral. With backing from ETH and LSTs, BOLD will notably sidestep the growing trend of stablecoins depending on real-world assets (RWAs) or custodians.

- Liquity V2 also introduces multiple Stability Pools, one for each collateral type, to absorb liquidations of undercollateralized loans. BOLD holders who deposit into these Stability Pools earn two types of yield: a majority of the interest payments from borrowers and liquidation gains from the corresponding collateral. This yield is aimed at creating a powerful incentive for users to hold and deposit BOLD.

- Looking ahead, the ecosystem that will grow around Liquity V2 is likely to expand beyond just lending, potentially leading to the creation of entirely new financial primitives centered around BOLD.

Powered by NFTs

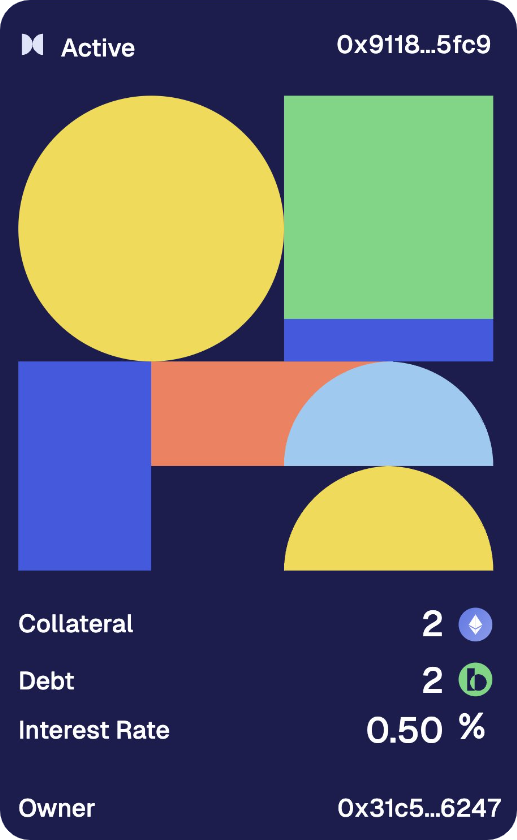

Another interesting wrinkle about Liquity V2 is that its Troves, i.e. CDPs, will be represented as fully onchain NFTs, similar to how Uniswap uses NFTs to represent its V3 liquidity provider positions.

This infra choice offers better flexibility in managing debt and collateral by allowing users to trade their entire LUSD borrow positions as an NFT, including both the collateral and the associated debt. This opens the door for borrowers to exit their positions without needing to liquidate or repay their loans directly.

That said, this concept of non-fungible vaults (NFVs), pioneered by Open Dollar, paves the way for decentralized loan markets, where CDPs can be freely traded on NFT secondary marketplaces. This mirrors the traditional finance market's ability to trade loans but with the added benefits of DeFi’s transparency and decentralization.

The NFT CDP approach also introduces new avenues for automation and composability, such as automatically listing a Trove for sale when liquidation risk becomes imminent. These possibilities can lead to a new wave of NFT-powered financial strategies that can provide users with greater control over their portfolios. This NFTfi crossroads is one to watch going forward accordingly!

Potential action steps

- 📰 Read the Liquity V2 whitepaper to get a full handle on the protocol

- 🏦 Try opening a small Trove on Liquity V1 to learn the basic UX ahead of the V2 rollout

- 📱 Follow Liquity on social media to stay tuned for the official V2 launch date announcement

- 💵 Explore Open Dollar on Arbitrum to get a feel for an NFT CDP system that’s already in action

- ⚔️ Keep an eye on the Bankless Liquity profile for future quests around the V2 platform