Dear Bankless Nation,

It currently costs ~$100K to become an Eth2 validator. 😱

That’s insane. The 32 ETH threshold has priced out a lot of people. (Who remembers when it was 1,000 ETH 😅 )

It’s an issue—the current requirements go against Ethereum ideals and the notion of open, democratized access to financial services. Adding to it, running an Eth2 validator requires a fair amount of technical knowledge. You need hardware, you have to run the software, keep it maintained so you don’t get slashed, etc.

It can be a lot.

So how can anyone expect the average individual to stake ETH?

Luckily, there are two main options out there.

The first is staking ETH through a centralized exchange like Coinbase and Kraken. This is the most beginner-friendly approach as they’ll abstract away all the complexities and allow you to stake any amount of ETH (not just the fixed 32 ETH required!) while earning a decent return.

The problem is that it’s centralized. You have to trust the exchange to hold your ETH and they usually take a hefty cut on the rewards you earn. Obviously, this isn’t an ideal solution for those that align with bankless values.

The other main option is decentralized staking providers. This is the holy grail for staking ETH and the one that we like to advocate for.

These open protocols democratize access to staking, providing you with an easy UI to stake any amount of ETH while also giving you a tokenized representation of your deposit to use elsewhere. The best part is that these protocols are designed to hold the deposits in a non-custodial fashion—you don’t have to trust anyone!

Lido and Rocket Pool are the two key contenders in this area. While Rocket Pool has yet to launch, Lido has been on mainnet for some time. And the growth has been astonishing.

They’ve already accumulated hundreds of thousands of ETH in deposits, valuing the total outstanding stETH (the protocol’s tokenized staked ETH derivative) to over $2.3B.

So we had to take a look to answer one key question:

Is Lido undervalued?

- Lucas

Lido is a non-custodial, liquid staking service.

The protocol provides stakers with liquidity for their assets through the issuance of a tokenized derivative. For Lido’s Ethereum implementation, this includes stETH. This token allows users to earn staking yields while still holding onto a fungible token, allowing holders to deploy their assets throughout DeFi.

How Lido Works

Before we dive into the LDO token, let’s take a moment to understand how Lido works under the hood—specifically for Ethereum and stETH.

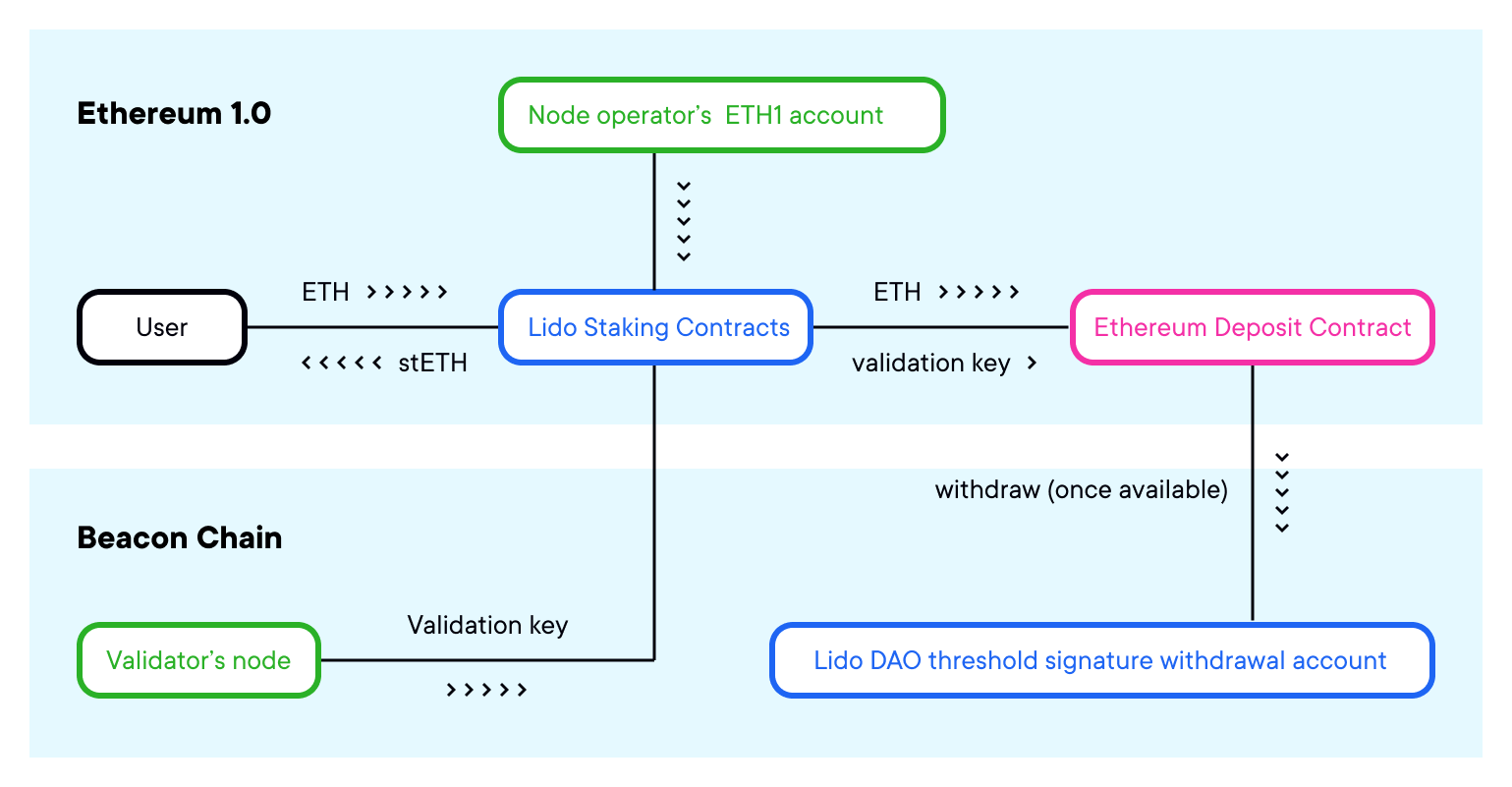

After a user clicks “deposit” on Lido’s interface, their tokens are sent to the protocol’s staking contracts.

These contracts pool together all user funds and then distribute them to DAO-selected node operators, of which there are currently nine, in increments of 32 ETH. These node operators are the entities responsible for managing and maintaining validators, meaning they’re the ones doing the actual staking.

There are a few important things to note about this system. First, because user funds are pooled together, slashing penalties result in a loss of funds for all depositors. The second key point is that node operators do not have access to user funds, but instead a public validation key that allows them to validate transactions with another user's stake. This means that Lido is non-custodial.

In addition to distributing tokens to node operators, the staking contracts are also responsible for minting and burning stETH, Lido’s staking derivative. stETH represents a claim on the underlying staked ETH along with all future earnings. Notably, it’s minted at a 1:1 ratio based on the amount a user deposits.

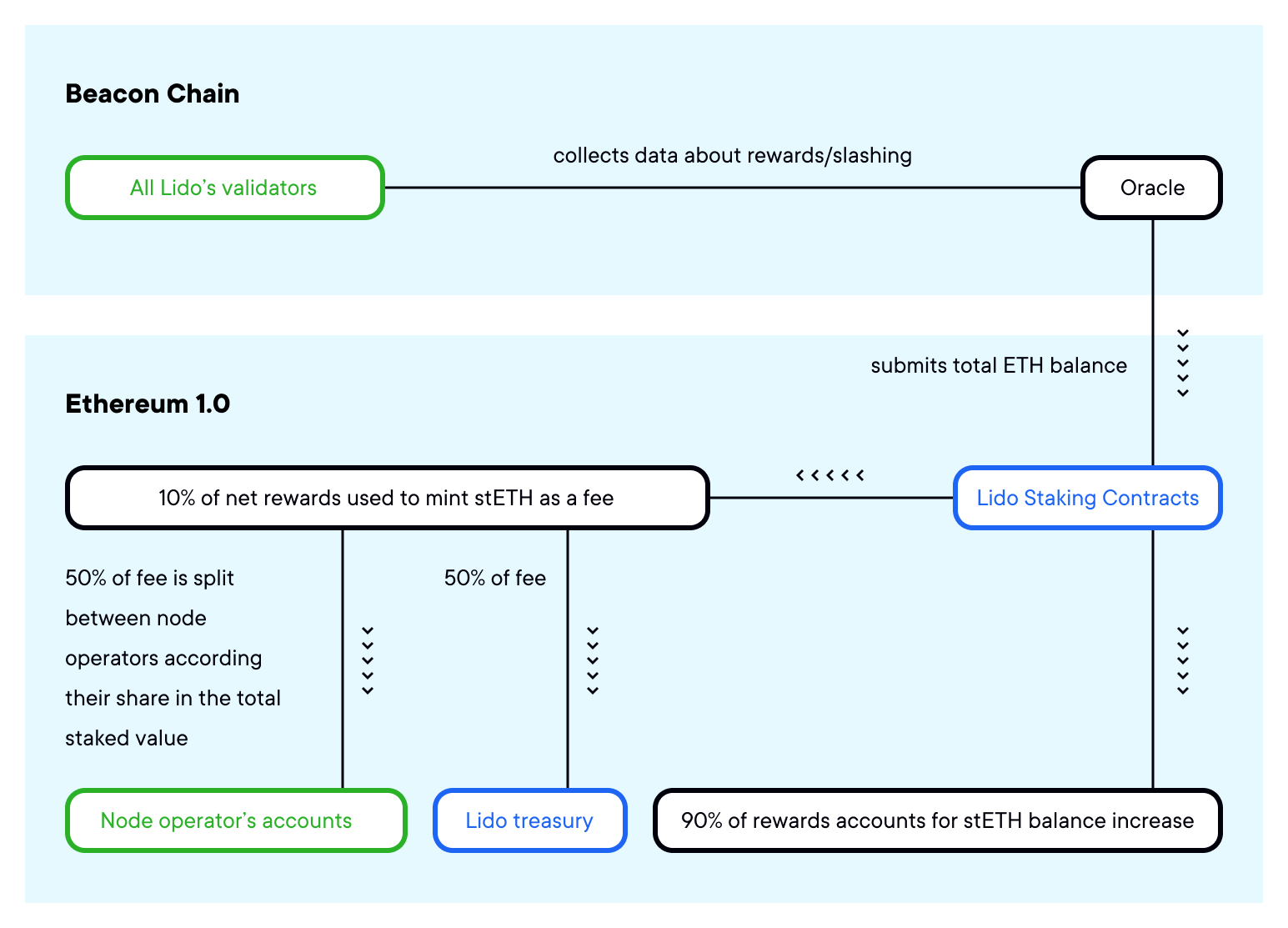

The protocol uses oracles selected by the DAO to monitor validators’ balances and to rebase users' stETH balances to account for rewards.

Currently, 90% of the earnings from staking go to depositors, while the DAO has a 10% cut of rewards. Currently, this fee is allocated at 50/50 split between node operators and slashing insurance.

🧠 To learn more about how Lido works in detail, click here.

Lido’s Value Proposition

Now that we understand how the protocol works, we can see the value that Lido provides to users.

For starters, it greatly increases the accessibility of non-custodial staking. As we know, self-custodial staking is difficult for non-technical users. It also comes with real stakes (pun intended) as failing to properly run a validator could result in the loss of funds through slashing penalties.

Lido simplifies staking ETH to make it as easy as using any other DeFi protocol, transferring the technical and slashing risk to world-class operators. Importantly, due to the pooling of user funds, holders with less than the 32 ETH required to run a validator can now stake and earn passive income on their holdings.

The stETH token—Lido’s staking derivative—also provides a major benefit for users by allowing them to access liquidity on their underlying Ether. Traditionally, staked assets are locked and unable to be used for other purposes. This is especially true at the current moment, as the Beacon Chain will not enable withdrawals until after the PoS merge.

Through stETH, Lido users can earn staking yields, maintain their share of the network, and also unlock the value of their tokens. In other words, stETH can be used as collateral for other DeFi protocols, drastically improving the utility of their staked position.

Competitive Advantages

Now that we understand how Lido works, let’s explore a few of the reasons as to why it’s been successful, and the factors that could enable it to maintain its competitive positioning.

Liquidity Network Effect

Due to the “liquidity begets liquidity” nature of staking derivatives, Lido benefits from strong network effects.

As we know, liquidity is a kingmaker within DeFi. This is because the more liquidity an asset or protocol has, the more likely it is to attract future liquidity, creating a network effect in which the “liquidity host” continually increases its economic bandwidth, and therefore utility, entrenching it within the DeFi stack.

This is a dynamic we’ve seen play out with stablecoins. Despite concerns over its reputation, the immense liquidity of Tether’s USDT has allowed it to maintain a dominant, albeit recently declining, share over this market.

This concept may also be applicable to staking derivatives such as stETH, as the more liquidity that stETH has, the more useful it becomes, and therefore, the more likely it is to attract future pools of liquidity.

🤓 To read a piece by Paradigm Researchers that dives into this concept further, click here

stETH Integrations

The integration of stETH within DeFi is critical to Lido’s success and helps reinforce its network effect.

Lido has managed to secure several key partnerships on this front to bolster stETH adoption. The most prominent is Curve and the ETH-stETH pool, which is incentivized by Lido via LDO rewards. This pool takes advantage of Curve’s low-slippage trades between like-assets to allow stETH holders to easily swap between the staking derivative and “regular” ETH. The pool currently holds over $3 billion in deposits, and more than 505,000 stETH, accounting for roughly 66% of the total stETH in circulation.

Beyond Curve, the protocol has partnered with DiversiFi, ARCX, and 1inch.

Along with building liquidity for exchange, Lido has also begun to make inroads in having stETH become a widely accepted form of collateral. stETH can be used collateral on smaller money markets such as Inverse Finance’s Anchor, as well as within two different active pools on Rari Capital’s Fuse.

However, the wheels are in motion to list stETH on Aave and enable it as collateral on Maker.

Barriers to Entry For Staking Services

New staking protocols face incredibly high barriers to entry.

Between the complexities of interacting with the Beacon Chain, slashing risks, and the inability to fork staked assets to go along with the active governance needed to ensure the orderly operation of the system, it’s incredibly difficult to run and maintain a staking service.

Due to their scale, incumbents such as Lido can enhance their offerings in ways that new players cannot. An example of this is access to slashing insurance, as Lido was able to partner with Unslashed Finance to purchase insurance for 196,479 ETH, roughly 26.5% of the total stake, from up to 5% in penalties.

Furthermore, because of their immense resources, Lido will also likely be able to employ advanced MEV strategies to increase returns for stakers, thereby increasing their competitiveness over potential challengers.

Intellectual Capital

Lido benefits from an incredibly strong cohort of intellectual capital. Along with a highly skilled and competent core team, Lido boasts multiple prominent members from all walks of crypto as contributors and community members, including UpOnly host Crypto Cobain, Tim Beiko, and Hasu. Additionally, the protocol has the backing of many of the space’s top investors, such as Paradigm, Three Arrows Capital, and ParaFi Capital.

Total Addressable Market (TAM)

We’d be remiss to talk about Lido without mentioning its addressable market.

The staking industry is expected to explode in growth over the next several years, with even TradFi institutions such as JP Morgan expecting earnings from staking to grow to $40 billion by 2025.

We don’t need boomers to tell us why this is possible: Due to the returns provided by staking, as well the incentive placed upon users to maintain their share of the network, it’s likely that a substantial portion of supply in PoS networks ends up being staked.

While post-merge Ethereum will almost certainly be the largest market for staking providers by a wide margin, Lido’s TAM includes all PoS networks. In addition to providing liquid ETH staking, Lido currently offers the same service for LUNA holders on Terra, with plans to expand to Solana, and potentially Polkadot.

These other chains not only represent growth opportunities for Lido, but could also position the LDO token as a cross-chain diversifier within an investor’s portfolio.

LDO Token Economics

Let’s take a look at the LDO token itself.

The sole, albeit incredibly important, purpose of LDO is governance over the protocol. There are currently no direct mechanisms to drive value to the token, such as buybacks or a staking mechanism that locks up supply, meaning that LDO is more akin to a traditional, growth-stage equity.

Despite this, token economics can still play a significant role in influencing its price movements.

Token Allocation

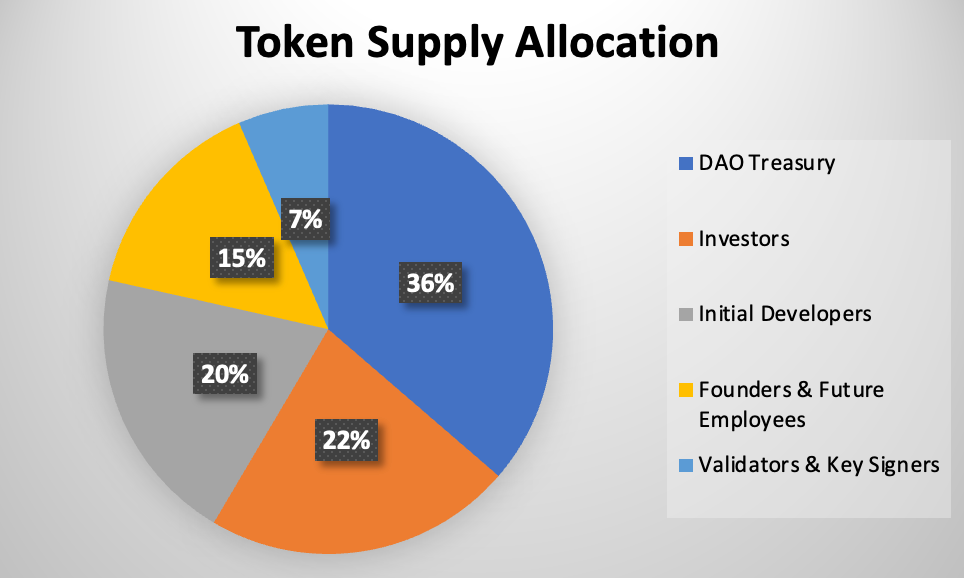

Lido has a total supply of 1 billion tokens. At launch, 36% was allocated to the DAO treasury, a combined 35% to team members (This includes founders, initial protocol developers, and future employees), 22% to investors, and 6.5% to staking validators and the withdrawal key signers.

These latter three groups tokens have a one-year lockup, followed by a one-year vesting period.

As we can see, this means that 63.5% of the total supply was allocated to protocol insiders. Because of this, it’s reasonable to say that control over Lido is still highly concentrated. In addition, the impending expiry of the lockup period poses the risk of placing perpetual downward pressure on the price of LDO due to sales from these parties. While the effect of this may not be felt as strongly during a bull run, it could potentially exacerbate declines should the market turn bearish.

Token Emissions

Along with allocation, emissions play a key role in determining the level of sell pressure a token may face. This represents an area of uncertainty for LDO holders, as there is no pre-set issuance schedule for the token. Instead, the decision to issue or distribute tokens, such as via liquidity mining programs, is at the discretion of the DAO. Currently, there are active liquidity mining programs in place on Curve, ARCx, 1inch and DiversiFi.

While this means that there will not necessarily be a constant emission-based sell pressure, it has led to a few interesting dynamics. For example, only 2.8% of the total LDO supply is circulating in the open market.

Along with creating a wide discrepancy between the quoted market cap and fully diluted valuation, it also means that the token may be more susceptible to wild price moves or sensitive to emissions.

Governance

As referenced earlier, governance is critically important to the functioning of Lido—perhaps more than other protocols. That’s because beyond just voting on standard project matters such as the allocation of the treasury, LDO holders are responsible for selecting node operators to handle the validation of users' stake, as well as oracle providers to help ensure the proper rebasing and distribution of stETH.

Lido governance has lived up to this need for active management, as since December 2020 there have been 83 proposals being put to a formal on-chain vote through Aragon, the platform used to handle DAO operations.

Of these proposals, 70 have passed, with 13 either failing to reach a quorum or being outright rejected. By DeFi standards, Lido has also seen pretty good voter engagement, with an average turnout of 55.9 million tokens per vote, or 5.59% of the total supply.

However, a deeper look at some voting metrics suggests that concerns surrounding centralized governance may be warranted.

For instance, 79 of the 83 votes were unanimous, in that all tokens voted the same way. Furthermore, 22 proposals received an identical turnout. As an example, seven proposals had a total vote count of exactly 52,718,000 million. This suggests that despite the high nominal engagement, a smaller group of holders may be participating in governance, and may have outsized influence over the direction of the protocol.

On-Chain Operational and Financial Metrics

Let’s look at some on-chain metrics to evaluate Lido’s performance and competitive positioning.

Deposits & Market Share

Lido has experienced tremendous growth since its launch in 2020. The protocol currently holds over 738,000 ETH, good for a 11.11% share of all ETH staked on the Beacon Chain.

This places Lido as the largest non-custodial staking entity and second-largest overall behind Kraken.

The protocol has also seen this share increase dramatically in recent months. Since April 2021, this has more than doubled from 5.2%. This suggests that Lido could be seeing signs of product-market fit.

Beyond growing its portion of the overall staking pie, Lido has been eating into the portions of other non-custodial solutions at a similarly rapid rate. Since April 2021, the protocol has seen its share of these deposits increase from 52% to 80.5%. This is further evidence that Lido is quickly emerging as the clear market leader in non-custodial staking.

Protocol Revenue

As previously mentioned, Lido generates revenue by charging a fee on the staking rewards earned by depositors. This fee is currently 10% and is being split evenly between paying node operators and slashing insurance. This means that the protocol's revenue is driven by the fee charged, the amount of assets staked, the yields earned by validators, and if measured in USD, the price of ETH.

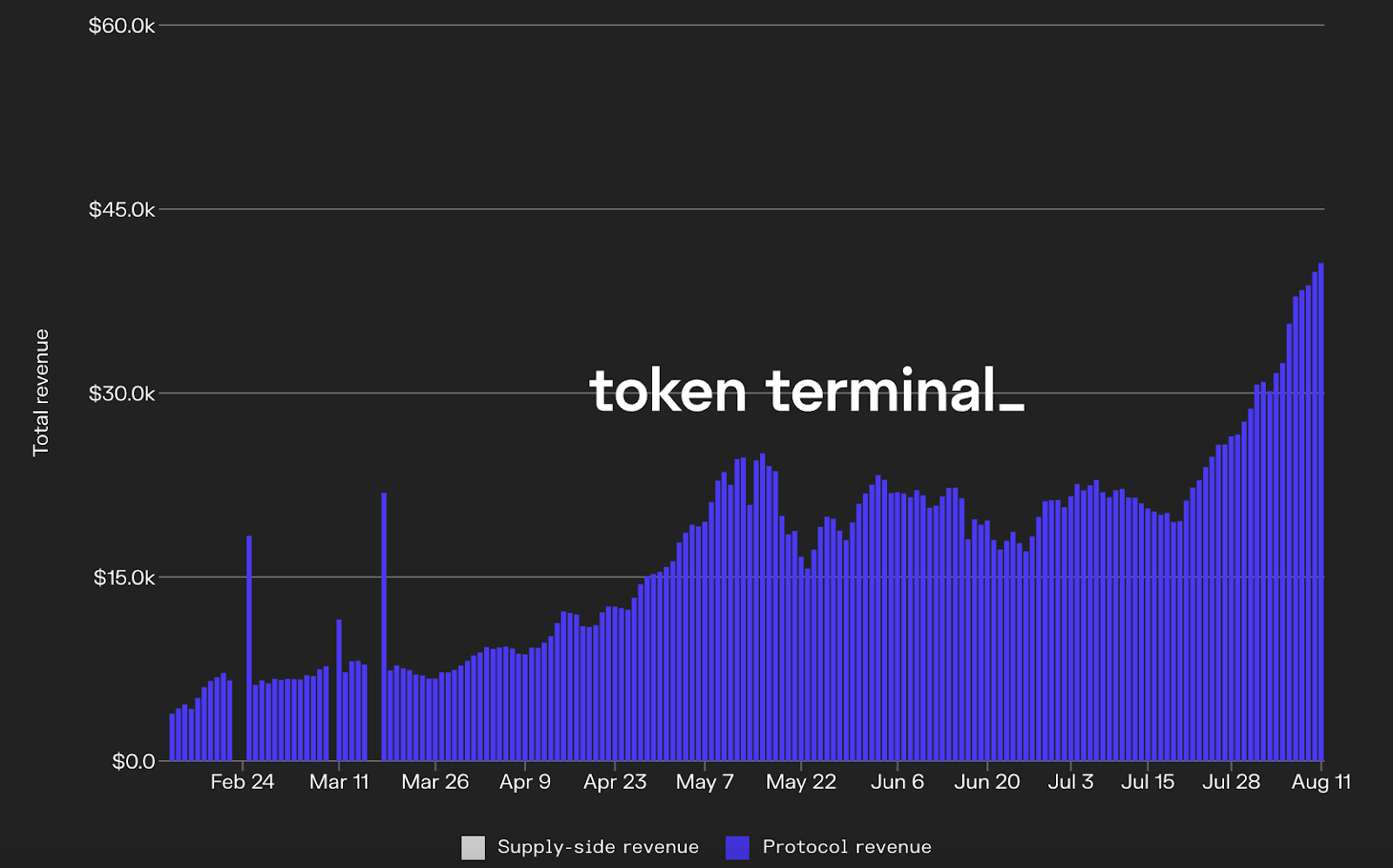

Since its launch in December 2020, Lido has generated $3.02 million in protocol revenue, about $4.53 million when annualized. While this may seem low when compared to other DeFi protocols, it’s worth pointing out that Beacon Chain staking yields, Lido’s revenue only consists of issuance, rather than also including returns from transaction fees and MEV. Lastly, despite it being active, Lido is currently not earning any revenue from Terra staking.

Taking a closer look, we can see that Lido’s daily revenues have reached an all-time high, now exceeding more than $40,000. Interestingly, we can also see that Lido did not experience as severe a decline in revenues compared to some other projects during crypto’s recent market sell-off. For example, while protocols such as Uniswap and Compound saw a peak-to-trough decline in revenues during this period of 92% and 86% respectively, Lido’s “only” fell by 40%.

These data points suggest that Lido’s revenue may not be as susceptible to influence from market and DeFi activity when compared to other projects. It also illustrates how Lido benefits from the secular nature of staking: Holders are going to want to stake their Ether irrespective of market conditions, meaning that Lido will be able to grow from within any backdrop.

Users

Since going live on mainnet, over 9,500 addresses have deposited funds into Lido. Despite this strong overall growth, a deeper look into user metrics raises some areas of concern.

A substantial portion of staked funds has come from a small number of large holders. More than 325,000 ETH (44%) can be attributed to just 14 users that have deposited more than 10,000 ETH, while an additional 231,000 (35%) can be attributed to an additional 67 users that have deposited between 1000-10,000 ETH.

This means that 0.69% of depositors account for 79% of deposits, suggesting that Lido’s customer base, and therefore sources of revenue, are highly concentrated and dependent on this small group of holders. Although a “run on Lido” cannot occur in the short term due to the lack of withdrawals from the Beacon Chain, it’s certainly worth keeping an eye on.

Discounted Cash Flow Valuation

Next, we’ll dissect a Discounted Cash Flow model on Lido and the LDO token.

Assumptions

This model makes major assumptions and uses conservative parameters. It’s intended more to reflect how Lido may be undervalued relative to its growth potential rather than be an end-all-be-all proclamation of its worth.

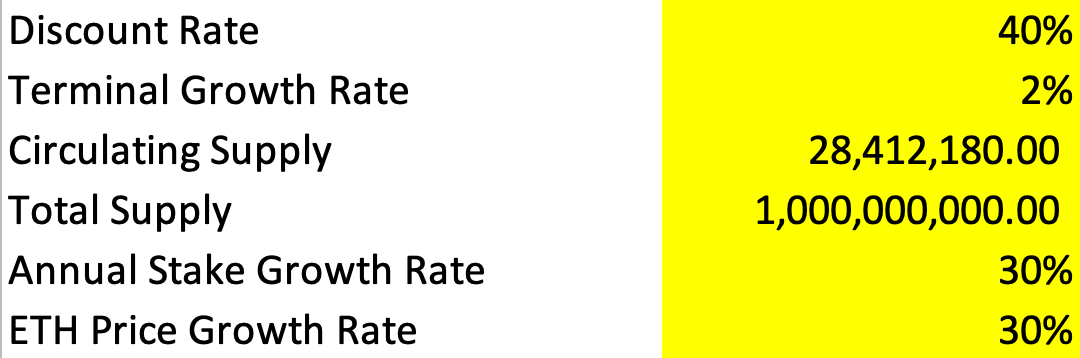

The model uses a discount rate of 40%, a figure in line with rates used by venture capitalists to reflect the high risk associated with early-stage investments. In addition, it uses a terminal growth rate of 2%, which is in line with that of global GDP growth.

For growth estimates, the model assumes the total amount of ETH staked will increase 30% per year, jumping from 7.3 million staked today to 20.9 million in 2025. It also assumes a 30% annual increase in the price of ETH, meaning that it would rise from $3000, around where it sits today, to $8568 in 2025.

Finally, the model uses Justin Drake’s projection of a 6% long term ETH staking yield and assumes that the Lido DAO take rate will remain at 10%.

Valuation

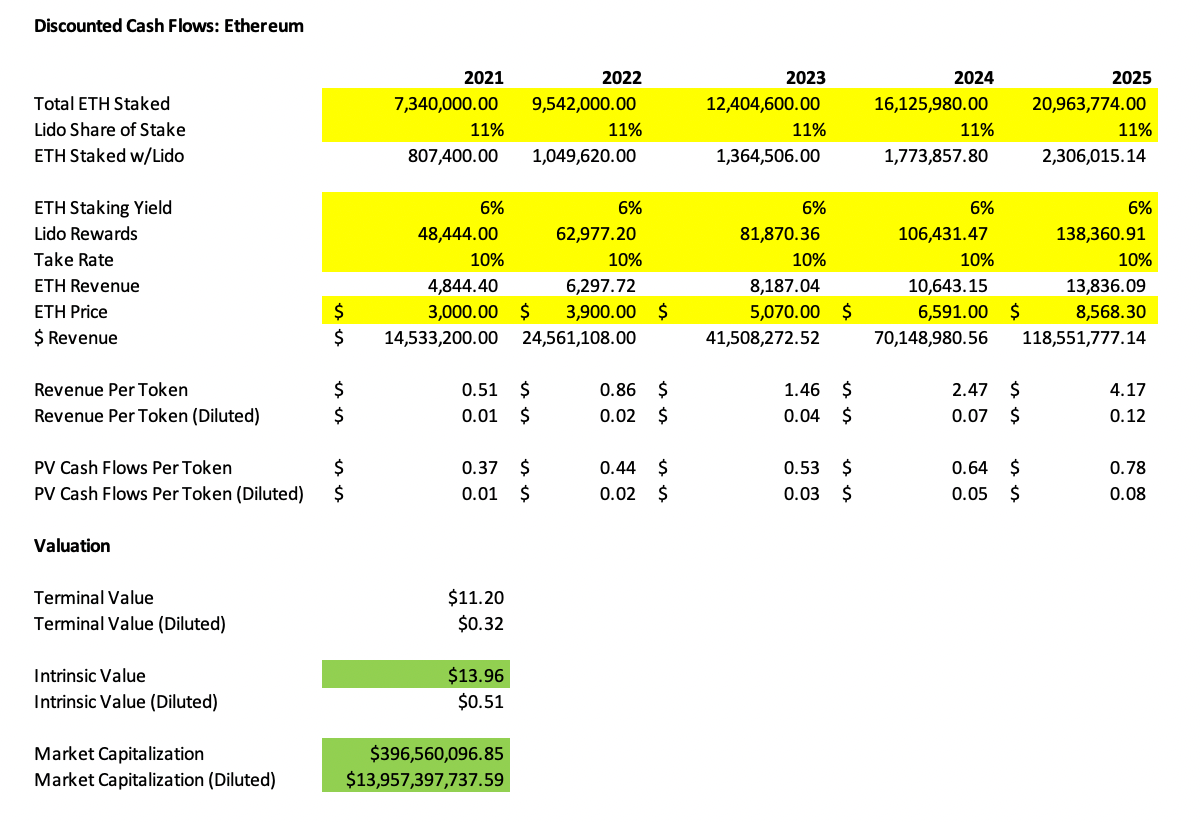

🤓 To play around with the model, which includes a hypothetical valuation of both the Terra and Solana staking services click here.

Using these parameters, we can calculate that LDO has an intrinsic value of $13.96, which would value it at a circulating market cap of $396 million, and FDV of 13.9 billion.

LDO currently trades at $4.74, meaning there could be 194% upside if it were to trade at its modeled intrinsic value.

Relative Valuation

Now, let’s see how Lido is valued relative to some of its peers.

This is a tricky exercise, as its most direct competitors like centralized exchanges and other liquid staking services such as Rocket Pool, are either companies (mostly private) or in the case of the latter, have yet to go live. Because of this, we’ll use other market-leading DeFi projects that are generating protocol-level revenue in different sectors, such as money markets, stablecoins, and perpetual swaps for the peer group.

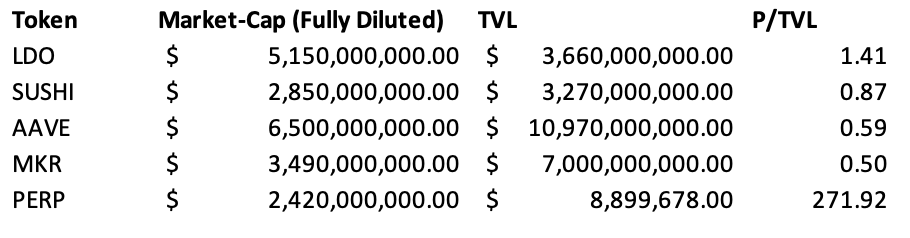

Price/TVL

On a Price/TVL basis, Lido appears to be trading at a premium to other DeFi protocols with a ratio of 1.41, which is substantially higher than the next closest protocol, SushiSwap. This could indicate that either Lido is overvalued relative to these other protocols, or that the market may be valuing its liquidity at a higher rate.

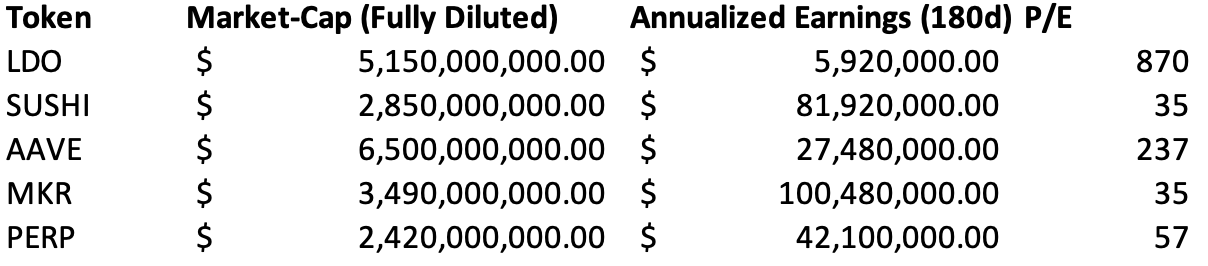

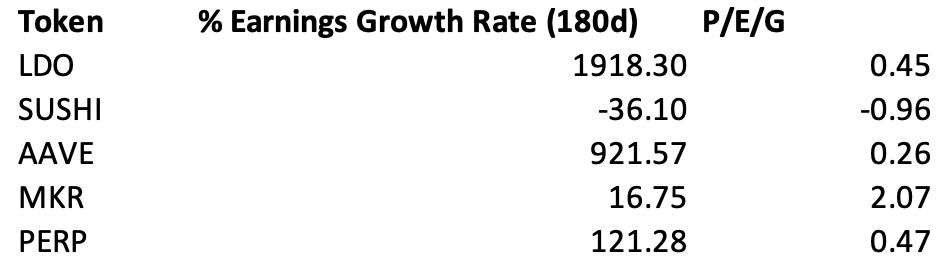

Price/Earnings and Price/Earnings/Growth

When looking at PE, Lido appears to be incredibly overvalued compared to the group. The protocol trades at 870x its earnings (based on annualized protocol revenue from the past 180 days), meaning it trades at more than a 3x greater multiple than that of the next closest token, AAVE, and a nearly 25x greater multiple than SUSHI and MKR.

However, looking at Lido’s price/earnings relative to its growth tells a different story. Due to its incredibly high growth rate of 1918%, LDO’s PEG is just 0.45, putting it in-line with that of PERP and AAVE.

This means that despite the high PE, relative to how fast it is growing Lido is valued at a market rate.

Risk Factors to Consider

As with any other crypto asset, Lido carries tremendous amounts of risk. Let’s highlight the major ones that we covered throughout the piece, as well as a few other potential areas of concern.

Protocol Trust Assumptions

While Lido is non-custodial, the protocol is not yet fully trustless. Due to the limited functionality ETH 2.0 staking at the time of the Lido’s launch deposits made into the protocol before July 15th, about 81% of deposits are not non-custodial. Rather, the withdrawal key (the private key that controls the ability to withdraw staked funds) for these assets is controlled by a 6/11 multisig scheme, with prominent DeFi community members and entities as signers. Were these signers to be compromised, decide to collude, or mishandle their key, a substantial portion of user funds would be at risk, which likely would adversely affect the price of LDO.

🌐 To read about Lido’s plan to make the protocol fully trustless, click here

User/Revenue Concentration

A substantial portion of Lido’s deposits, and therefore sources of revenue, are concentrated within a small group of depositors.

Governance Centralization

The LDO token supply, and therefore governance power is concentrated within a small group of stakeholders.

Token Emissions

LDO has undefined token emissions and a very low circulating float to the total supply of tokens.

Regulatory Risks

The provision in the United States infrastructure bill could place unruly regulation on Proof-Of-Stake validators, which could increase the difficulty of finding high quality node operators.

Conclusion

Although there are serious vectors of centralization, with its useful product, wide and diverse moat, large TAM, strong competitive positioning, and a possibly undervalued token, Lido has stellar fundamentals. The former issues can be fixed over time and was an intentional design choice in order to launch on mainnet.

That said, with more infrastructure coming online surrounding Eth2, along with the merge, the market for decentralized staking providers is anything but solidified. But for now we’ll ask:

Can LDO help steal the thunder from the JPEG mania?

NOTHING IN THIS ARTICLE IS FINANCIAL OR INVESTMENT ADVICE. DO YOUR OWN RESEARCH.

DISCLOSURE: The author holds LDO tokens.

Action steps

- Research Lido and the LDO token

- Stake your ETH (at your own risk!)