Insights From the FTX Implosion

Dear Bankless Nation,

Is anybody else exhausted from this chaotic week?

We recapped the wild series of events around FTX yesterday. 👈

The situation is changing rapidly, and there’s still so much that we don’t know.

Today’s newsletter takes a deeper dive into the data.

- When did users start withdrawing funds en masse from FTX?

- How much money is Alameda moving around on DeFi?

- Which DeFi protocols are being hit the hardest?

Our resident on-chain sleuth Ben takes us into the analytical deep-end. 🕵️

- Bankless team

These are among the darkest days in crypto.

The second largest centralized exchange FTX led by founder and CEO Sam Bankman-Fried is on the brink of collapse, with the exchange unable to meet user withdrawals 1:1 while alleged to be in the hole for as much as $8-10B in customer deposits.

It’s unclear what exactly FTX did to lose such an immense amount of funds, but many have speculated that there has been co-mingling of finances between the CEX and Alameda Research, a trading firm co-founded and owned by SBF.

But on-chain data tells us a partial story, so we can gain insight into how things have unfolded, connections between Alameda and FTX, and the impact of the exchange’s implosion on DeFi.

Here are some of the most interesting insights we’ve found.

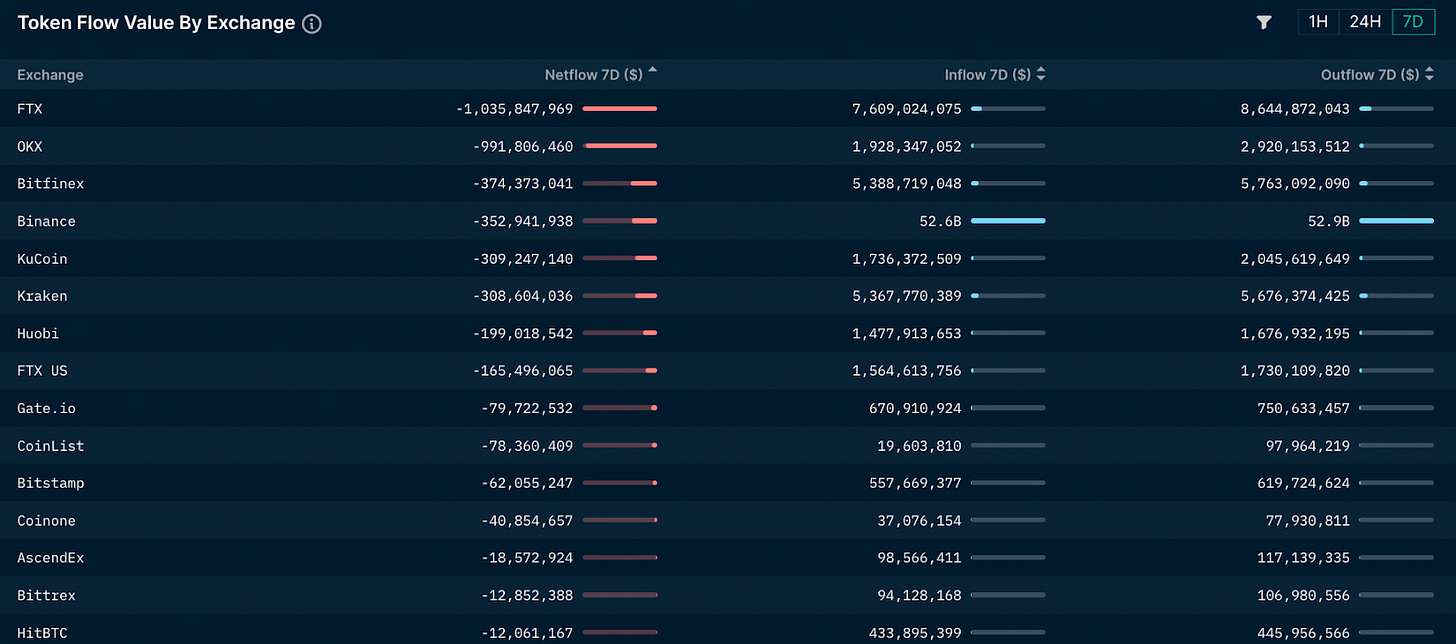

FTX Experienced A Massive Bank Run, And Whales Got Out the Door

Over the past week, FTX has seen more than $8.7B in withdrawals compared to $7.7B in deposits, good for net outflows of $1B. This, unsurprisingly, was the largest of any exchange during this period.

While panic began to set in on November 6 following CZ’s now infamous tweet, the exchange began to see notable outflows well before this.

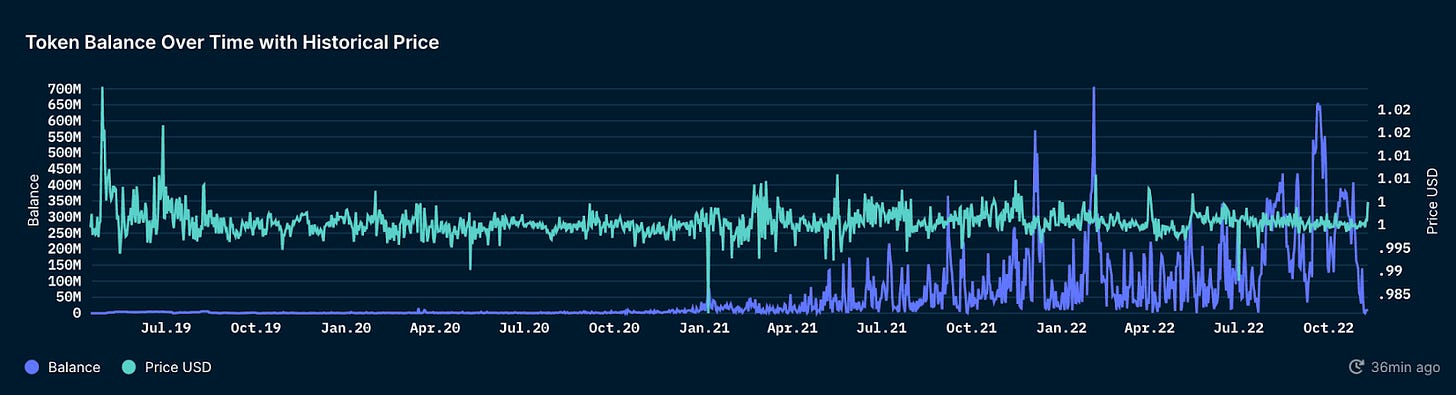

For instance, the USDC balance in FTX’s primary Ethereum hot wallet peaked out at $408.3M on October 26, though many of the withdrawals initiated during this period were from Alameda. This poses some interesting questions, such as whether they needed to pull funds to meet liquidity needs elsewhere (We’ll touch on this a bit later).

We can also see that the exchanges’ drop in stablecoin liquidity occurred at an incredible rate. The FTX wallet held $140.3M of USDC on November 4, but this was whittled down to just $3.1M by November 6 as the run began to fully take hold.

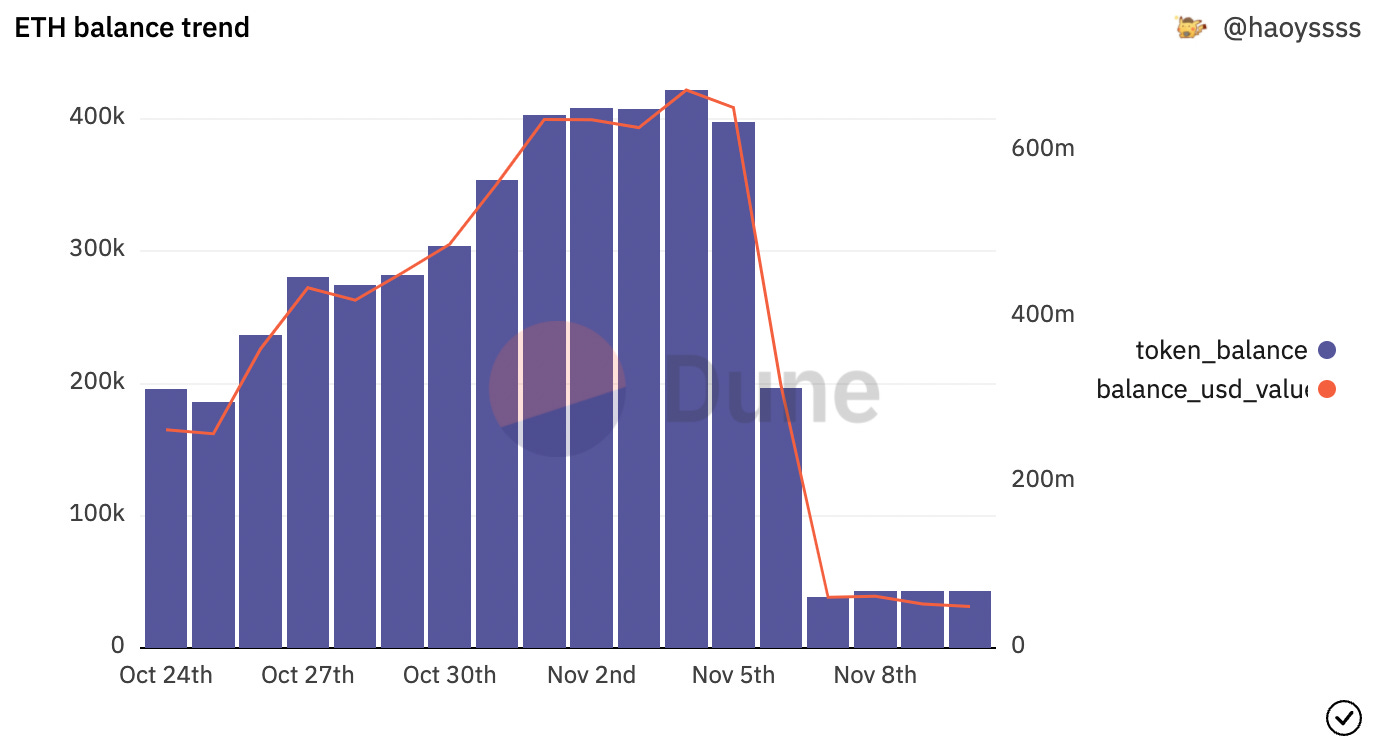

Ether held on FTX also dropped dramatically following CZ’s tweet, with more than 358,000 ETH being pulled from the platform between November 5 - November 7.

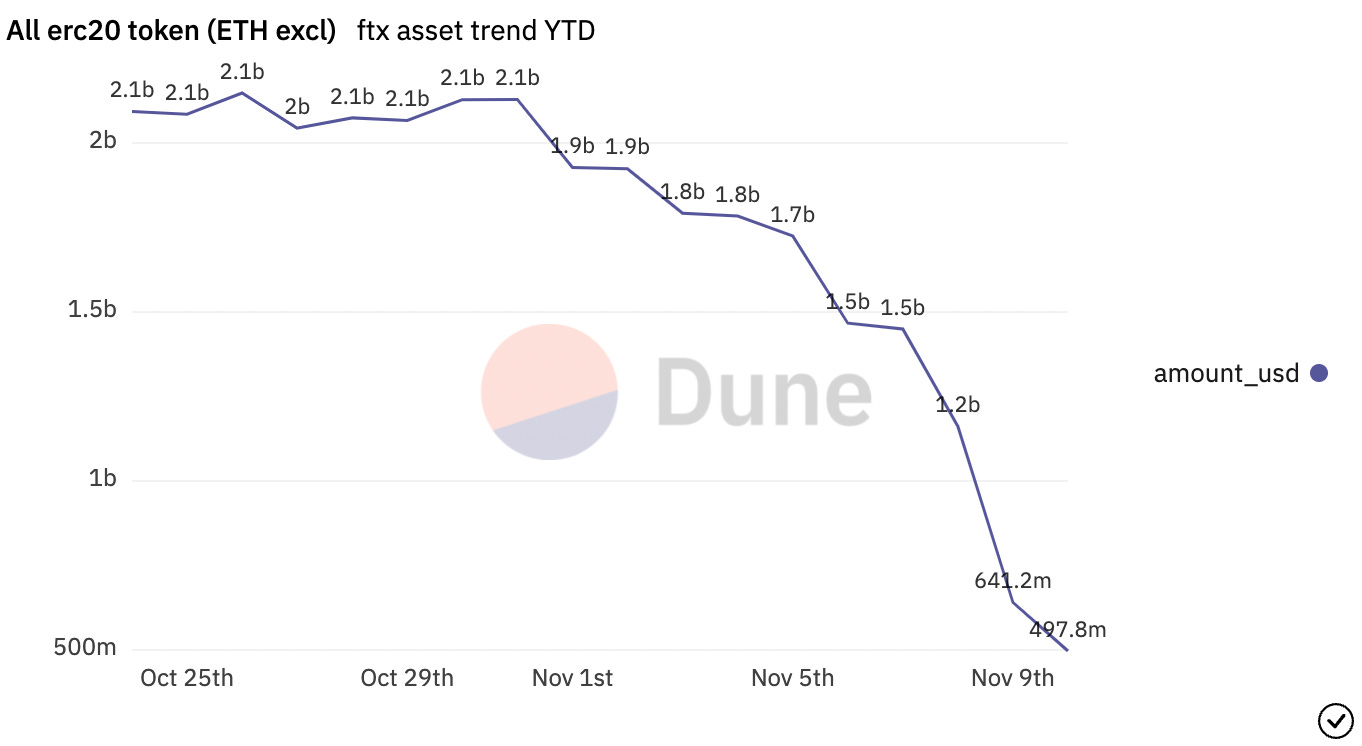

The final shoe to drop were non-ETH ERC20s, with the value of these assets held on the platform falling by ~$1B between November 5-November 10. Although some of this can be attributed to stablecoin outflows and price declines, the fact that this balance seemed to decline more gradually suggests that FTX users “fled to quality” in that they withdrew larger, more liquid assets first before moving on to the smaller, less liquid ones.

While many large players such as Multicoin Capital, have a significant amount of funds trapped on FTX, some whales were able to make it out the door with some or all of their funds.

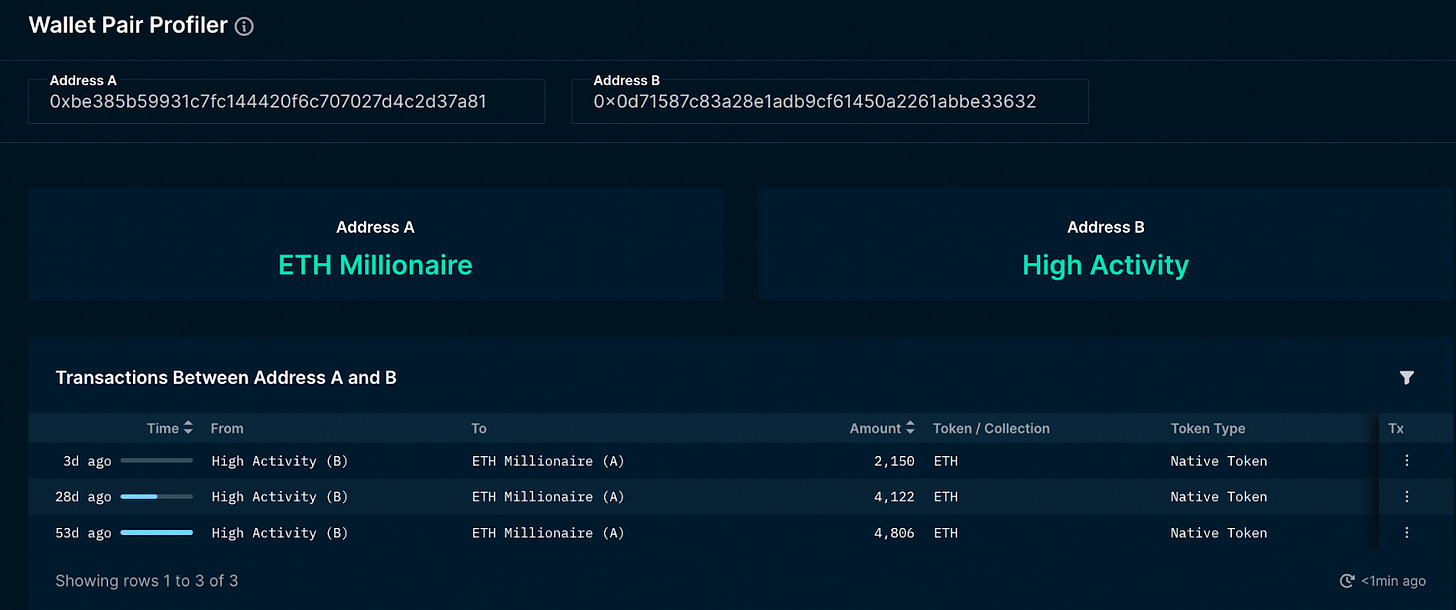

For instance, one wallet, 0xbe385b59931c7fc144420f6c707027d4c2d37a81, was able to withdraw $269M of USDC and USDT from FTX between November 6-8.

The entitry that withdrew ~$300m from FTX moved ~$33m so far to Binance.

— Hsaka (@HsakaTrades) November 10, 2022

Guessing it was Genesis or Alameda.https://t.co/aUr2xSGFKW pic.twitter.com/8ukE8X3HAr

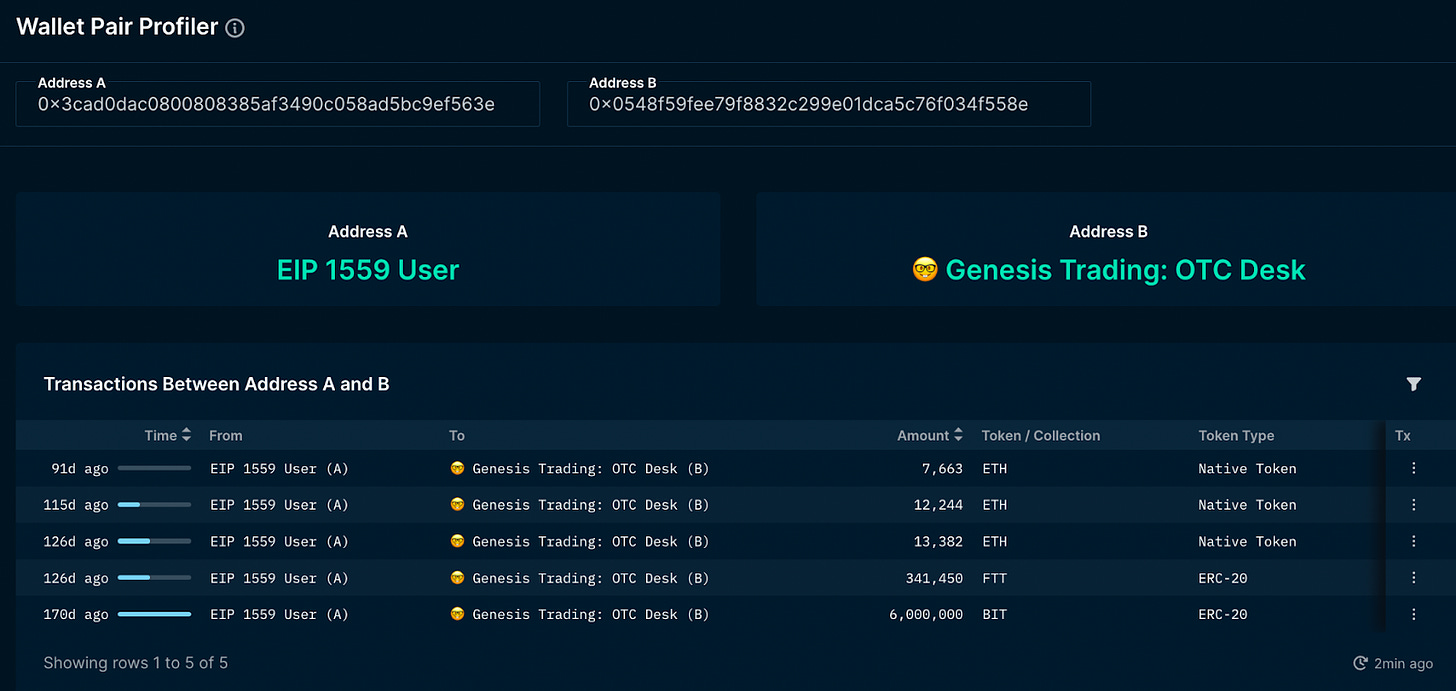

It’s unknown who the owner of this wallet may be, though we can glean some clues through looking at other addresses that it has interacted with.

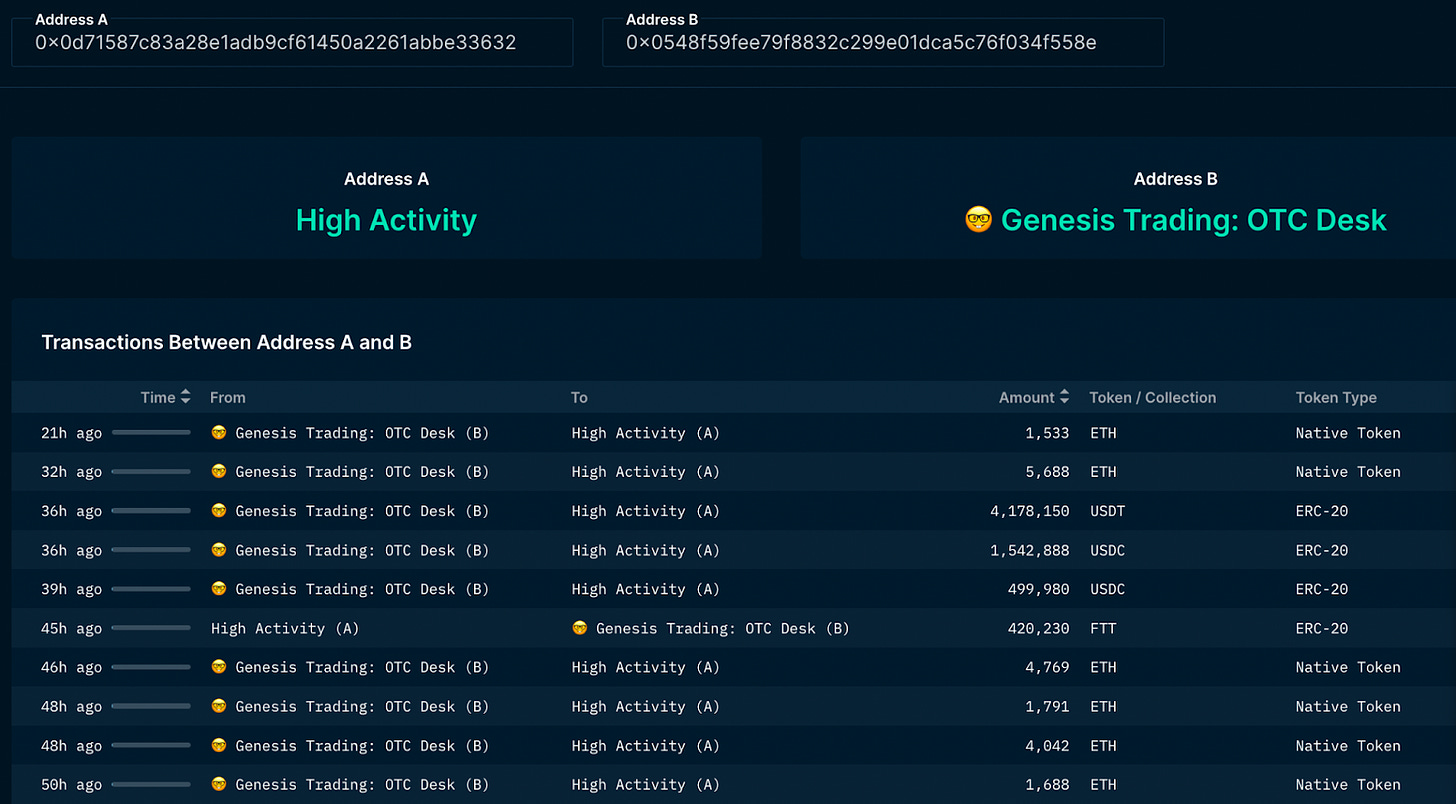

Since its creation, the wallet (which we’ll call wallet A) has received 11,008 ETH from another address: 0x0d71587c83a28e1adb9cf61450a2261abbe33632 (wallet B).

B has a similarly interesting history. Since creation, it has received 857,860 ETH from Genesis OTC while sending 507,785 of ETH to Three Arrows Capital.

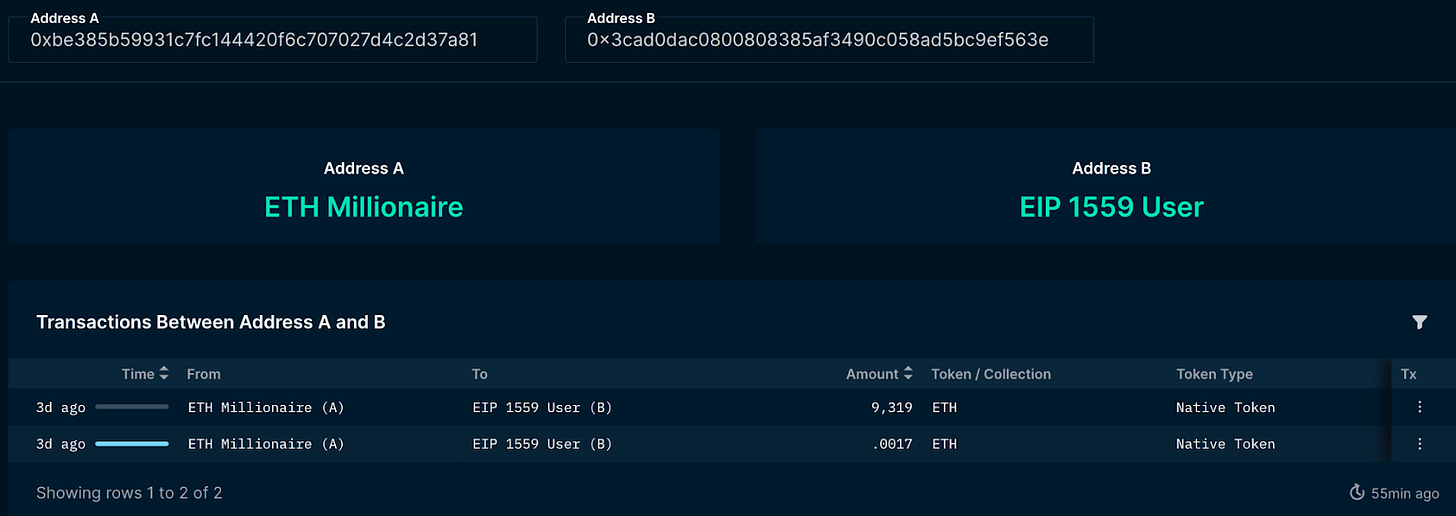

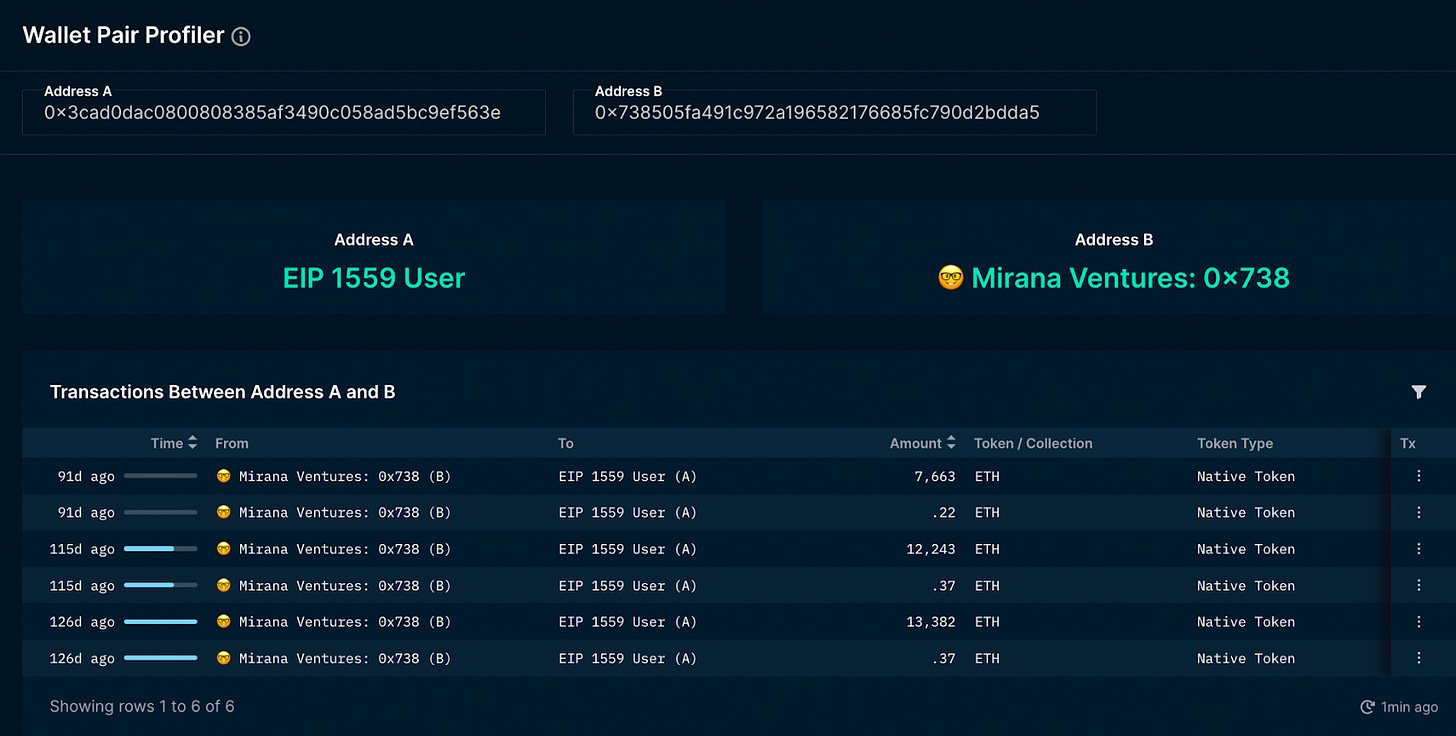

A has also sent 9319 ETH to another wallet 0x3cad0dac0800808385af3490c058ad5bc9ef563e (wallet C). Wallet C has a notable interaction history of its own, as over time it has received 33,289 ETH from Mirana Ventures, the early stage investment arm of centralized exchange ByBit.

Shortly after receiving the ETH from Mirana, Wallet C transferred it to the same Genesis OTC wallet.

We will let you draw your own conclusions based on this transaction history.

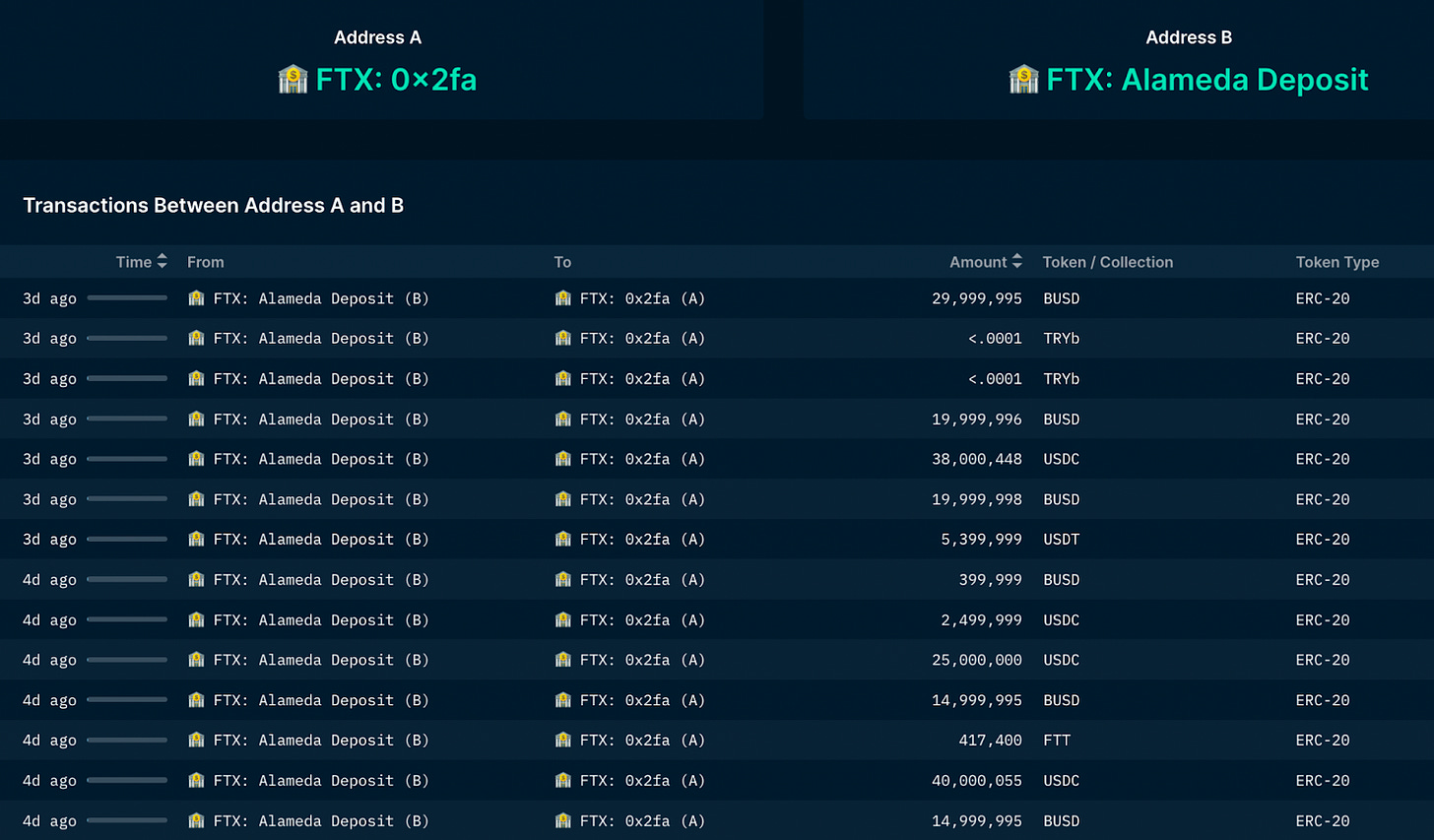

Alameda Helped Plugged The Hole

The events and revelations of the past few days have made clear that FTX and Alameda Research were more closely intertwined than many had thought. This idea is reinforced when looking at transaction data, as it suggests that the trading shop was attempting to help plug the hole at FTX.

As we can see, despite, as previously mentioned, having withdrawn tens of millions from FTX between October 25 - November 4, Alameda deposited over $360.9M of USDC and BUSD into FTX between November 5-7.

This seems to lend credence to the idea that FTX funds were co-mingled with Alameda, as no rational actor seeking to preserve their capital would deposit funds into a financial institution that is in the midst of experiencing a run.

It looks like Alameda tried, and failed to plug the seemingly massive hole at FTX.

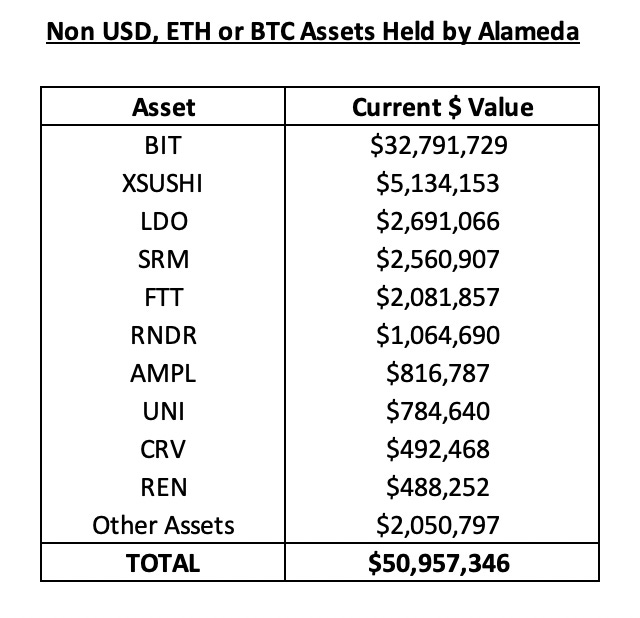

Alameda Still Holds ~$50.9M In Tokens And Has $12M in on-chain Under-Collateralized Debt Obligations

Despite speculation that the firm is going under following FTX’s collapse and the fall in the price of FTT (which the firm was using as collateral for loans), Alameda seemingly still holds millions in tokens on-chain.

According to a set of suspected Alameda wallets from Larry Cermak of The Block, the firm has ~$50.9M worth of assets that are not USD, ETH or BTC. Of this, their largest position is BIT, the token of centralized exchange ByBit, which the trading shop acquired via a token swap for FTT. Despite rumors to the contrary, it appears Alameda is still holding the 100M tokens, worth ~$32M at current prices.

The largest positions in projects that are not directly linked to FTX or Alameda are xSUSHI and LDO, with the firm holding a combined $5.8M worth of tokens. Given their precarious state, it seems likely that Alameda liquidates their position in each of these tokens, looming as a small supply overhang in an increasingly illiquid market.

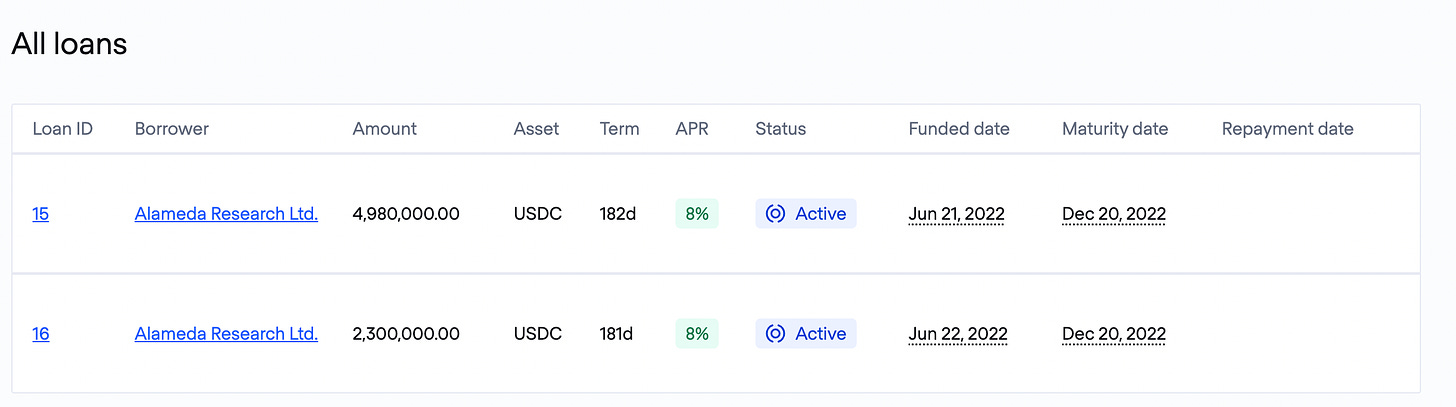

Given that they were incredibly active in DeFi, Alameda unsurprisingly has more than just token exposure. The firm also has a combined ~$12.8M in outstanding debt from Clearpool and TrueFi, two under-collateralized lending platforms.

Alameda has historically been a frequent user of these products, as they once had their own pool Maple Finance, the largest undercollateralized lender platform in DeFi. Thankfully, this pool has been deprecated and no Maple pools have exposure to the trading shop.

In addition, it is also worth noting that the $5.5M in loans made to Alameda via Clearpool was via a permissioned pool, with firms Apollo Capital and Compound Credit Partners being the only lenders.

MIM, USDT, stETH comes under pressure

Although Alameda has some exposure to DeFi tokens and undercollateralized lenders, the DeFi protocol most significantly impacted by the chaos of the past few days has been Abracadabra, an over-collateralized lending platform where users can mint Magic Internet Money (MIM), a USD-pegged stablecoin.

Alameda was a major user of Abracadabra, where they used FTT as collateral to mint MIM.

Abracabdra’s exposure to the firm and FTT was immense, as on November 3rd, more than 35% of the outstanding MIM supply was backed by FTT.

This caused DeFi users to reduce exposure to the stablecoin when FTX and Alameda’s troubles became apparent.

How do we tell? By looking at the biggest stablecoin exchange Curve.

The MIM-3CRV pool on Curve, MIM’s largest source of liquidity, became significantly imbalanced. As of writing, the pool’s composition is just 13.8% 3CRV to 86.2% MIM, rather than the ideal 50/50 split.

This liquidity drain caused MIM to significantly de-peg, falling as low as $0.93 before almost fully re-pegging.

This quick bounce back is likely due to the nature of CDP-based stablecoins, as Alameda was incentivized to buy cheap MIM, creating demand for it, in order to repay their debt which they have in full. MIM also benefits from a very high A-factor on Curve which allows it to hold its $1 peg even if its pool is significantly imbalanced.

Despite Alameda’s debt repayment, the stablecoin liquidity crunch has spread to other assets such as USDT.

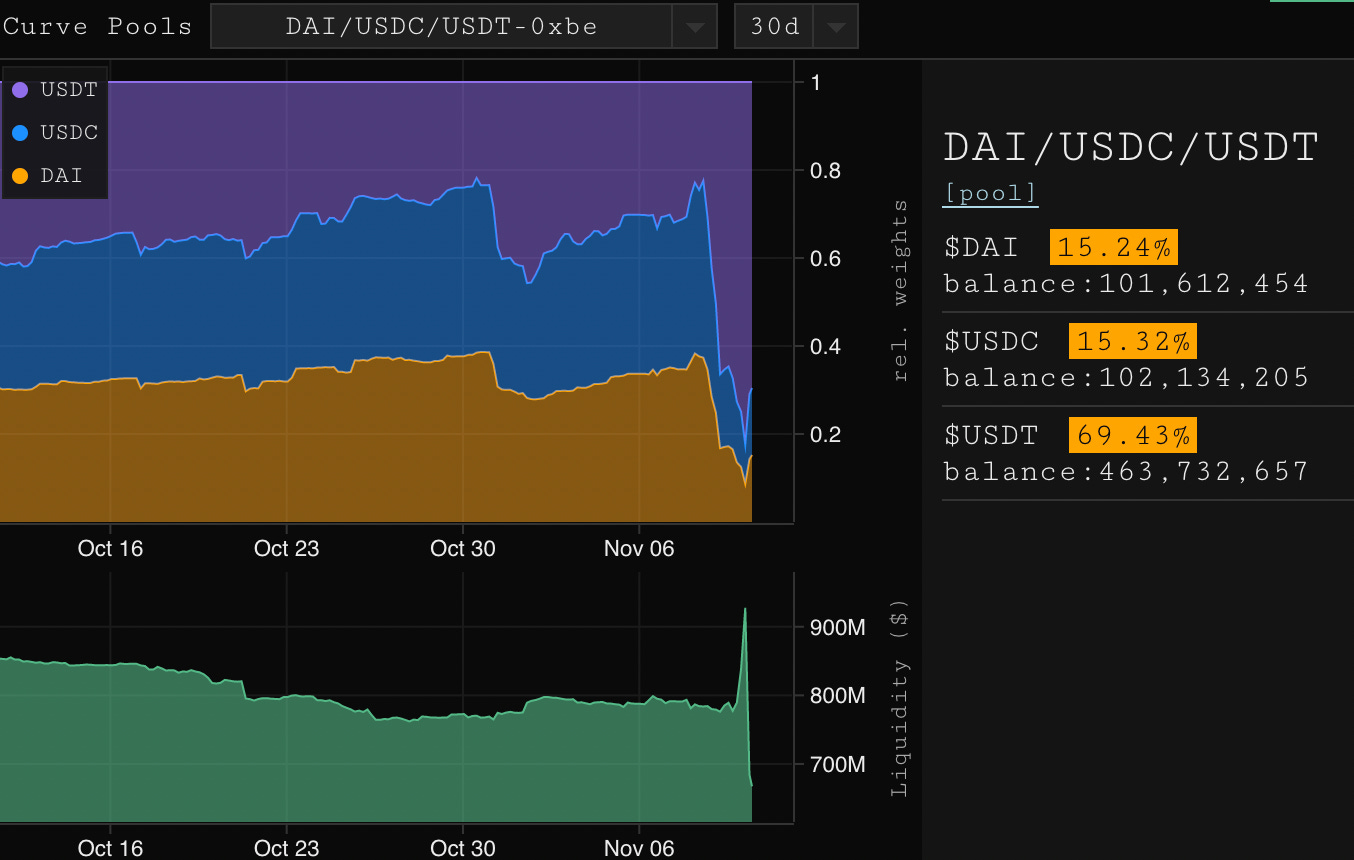

The 3Pool on Curve (DAI/USDC/USDT) is also significantly imbalanced, with a composition of 15.2% DAI, 15.3% USDC, and 69.4% USDT, instead of the ideal ⅓ split between each.

This suggests that liquidity providers are fearful of having exposure to USDT, instead “fleeing” to USDC and DAI by withdrawing it from the pool.

Other DeFi users are also betting against USDT, as utilization rates for the asset are at 87% on Aave and 92% on Compound respectively, causing borrow rates for the stablecoin to soar. This suggests that users are borrowing USDT in order to short it, likely fearing that Tether has credit exposure to FTX and Alameda, an allegation which they have denied. USDT briefly traded down to $0.97 on November 9, but has since traded back to peg.

These Curve pool imbalances are indicative of the tremendous amount of fear in the market, particularly around stablecoins Alameda had confirmed or suspected exposure too. Savvy investors may want to pay attention to their composition over the coming days and weeks, as these pools' rebalancing could suggest that panic in the markets has subsided.

Conclusion

The transparency of blockchains allows us to glean numerous insights around the impact of FTX’s stunning collapse - and we’ve only scratched the surface in this piece.

As we can see, funds were being shuttled between FTX and Alameda before and during the run on the exchange, lending credence to the idea that the two entities were more closely tied at the hip than anyone could have imagined. We also know that a very large entity was able to withdraw hundreds of millions in stablecoins during the run, recouping some or all of their funds.

We can also see that Alameda still has more than $50M in tokens that are at risk of being dumped onto the market as well as north of $12M in outstanding loans which seem to be at very high risk of default.

Finally, we can see that the collapse of FTX has caused chaos across DeFi, with liquidity drying up for both MIM and USDT, with DeFi users taking major short positions against the latter.

More information will come to light in the coming days, weeks, and months. But the beauty of blockchains means that you can seek out answers in the meantime.