Michael Saylor's Master Plan

View in Browser

Sponsor: MegaETH — Crypto has new apps, finally.

- 💰 Trump Team Schedules Mar-a-Lago Memecoin Conference for April 25. It is unclear whether the President will be able to physically attend the publicly touted event.

- 👔 Potential Buyers Evaluate Partial Acquisition of Gemini Exchange. Interested parties are reportedly hunting for a regulatory shortcut to more easily enter European and British crypto markets.

- 🇺🇸 Ethereum Developer Announces Candidacy for U.S. Congress. Joe "CupOJoseph" Schiarizzi is running for Congress as a Democrat in Virginia's new 7th district.

| Prices as of 5pm ET | 24hr | 7d |

|

Crypto $2.46T | ↗ 1.2% | ↗ 7.6% |

|

BTC $72,195 | ↗ 0.9% | ↗ 7.9% |

|

ETH $2,198 | ↗ 0.1% | ↗ 7.1% |

Michael Saylor thinks Bitcoin is headed to $21 million, but the real story in this conversation is how he believes it gets there.

In his first appearance on Bankless, Saylor breaks down Strategy’s evolving capital machine, why STRC may be the most ambitious instrument the company has built yet, how he thinks about quantum risk without panic, why his view on Ethereum has become more constructive, and what he means when he says the endgame is giving the world an 8% bank account forever.

Subscribe to unlock the full episode in Early Access!👇

Once a week, Premium subscribers get access to the top Market Plays, Hot Reads, Farming Opps, and Airdrop Hunts that our analyst team is tracking! Don't miss out! 👇

Once treated as the black sheep of finance, DeFi is now being seriously examined by institutions – its core mechanisms tested, validated, and increasingly viewed as a credible alternative to legacy systems.

In a report published last week, the Bank of Canada explored decentralized lending with a case study on Aave V3, the largest DeFi lending protocol by TVL.

Authored by Bank of Canada economist Jonathan Chiu and University of Toronto researcher Furkan Danisman, the paper analyzed transaction data from Aave V3’s Ethereum mainnet deployment, examining revenue flows, borrower behavior and liquidation events.

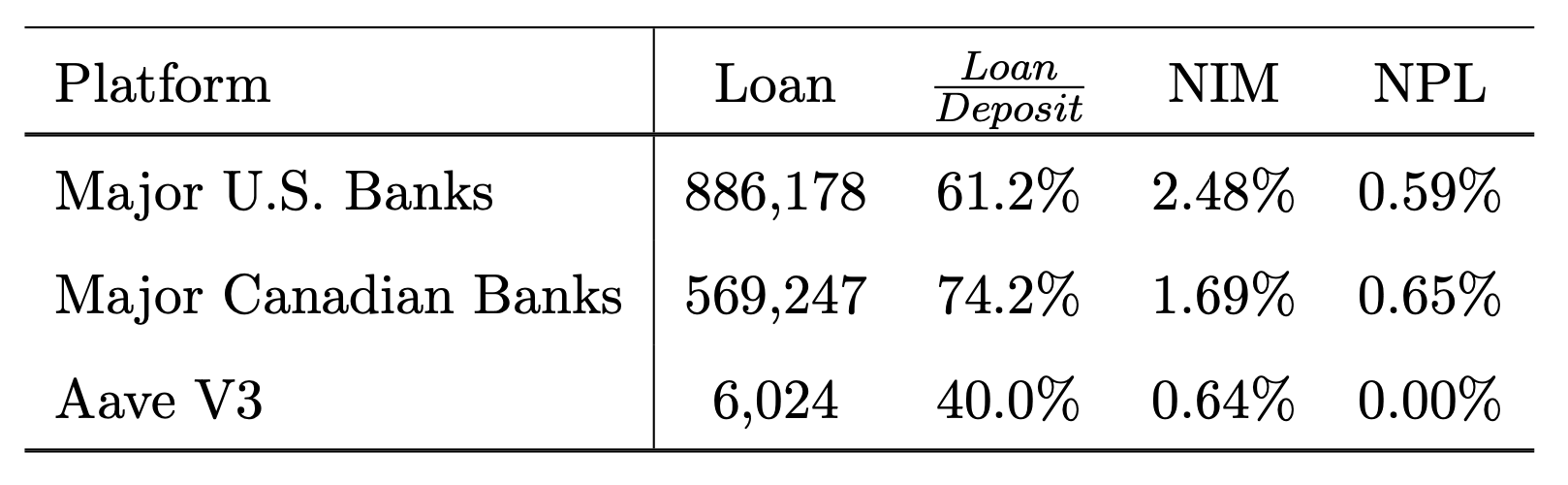

The analysis found that Aave’s revenue is largely generated from the spread between borrow and supply rates – paralleling banks’ net interest margin – with other earnings derived from crypto-native liquidations and flash loan fees. Among Aave borrowers, leverage was common, with about 20% of borrow volume and 8% of transactions involving recursive leverage, whereby users borrow one asset, swap it for collateral, and re-borrow to amplify positions.

Despite the drama created by liquidations, the paper found no persistent negative price impact from liquidations on broader crypto markets, assuming proper controls (like required overcollateralization and rule-based liquidations) are applied.

The Bank of Canada’s paper took the stance that decentralized, intermediary-free lending is both technically and operationally viable today.

However, it stops short of outright endorsing models like Aave, highlighting key limitations around capital efficiency, constrained leverage, and broader systemic fragility within the crypto ecosystem.

But for legacy financial system guardians, like the Bank of Canada, even a tacit embrace of decentralized technology is monumental.

Still, finance is structured around tangible incentives, and where there’s meaningful profit to be made or efficiency to be gained, the institutions managing capital are bound to explore.

The Bank of Canada explored Aave as a case study for the safety of decentralized lending. Its analysis found no evidence of non-performing loans, and discovered that the DeFi protocol was capable of operating sustainably with a lower net interest margin than traditional banks, features that, in theory, make Aave safer than a traditional bank and allow it to return a greater portion of interest to depositors.

While the Bank of Canada’s analysis validates that decentralized lending can function efficiently, it also underscores what still holds institutions back. The requirement that borrowers overcollateralize positions on Aave reduces capital efficiency. At the same time, further inefficiencies arise from idle capital sitting in Aave pools, waiting to be borrowed or withdrawn.

Together, these dynamics increase the amount of unused capital in the system, raising the minimum return threshold needed for institutional participation to make economic sense.

Additionally, when interacting with any onchain application, smart contract hacks remain a very real risk consideration. For institutions to even consider interacting with even the most mature DeFi applications, the anticipated upside must justify the potential of total loss, or they must view the prospect of exploit as minimal.

And while the Bank of Canada highlights Aave’s track record of zero non-performing loans, the DeFi lending market has indeed accumulated bad debt in the past. Before allocating capital, an institution would need to get comfortable with Aave’s multi-billion-dollar exposure to Ethena, for example, which depends on the custody and operational capabilities of multiple third parties.

For institutional capital, the returns received from decentralized solutions must simply exceed the returns they can earn on traditional equivalents by a margin large enough to justify these additional, harder-to-quantify risks, and if DeFi yields fall below that threshold, there’s little economic motivator for large allocators to participate.

DeFi has proven it works – now it’s a matter of when the institutions fully lean in.

We're past "in it for the tech" or "in it for the money." MegaETH is bringing you products worth using, powered by USDM.

Not financial or tax advice. This newsletter is strictly educational and is not investment advice or a solicitation to buy or sell any assets or to make any financial decisions. This newsletter is not tax advice. Talk to your accountant. Do your own research.

Disclosure. From time-to-time I may add links in this newsletter to products I use. I may receive commission if you make a purchase through one of these links. Additionally, the Bankless writers hold crypto assets. See our investment disclosures here.