🏴 Fed Up with Feds

Web3 has a steep learning curve. MetaMask Learn is a free-to-use education platform available in 10 languages to help you get started with basic Web3 topics and concepts.

Dear Bankless Nation,

American regulators are sharpening their knives, looking to levy more fines and shut down more services in the crypto space.

Investor protection is their purported goal, but by making one-off enforcement actions without setting any clear guidelines or working with the sector’s biggest players, it’s unclear that anything they’re doing is actually productive for a vast, varied and fast-growing new financial ecosystem.

- Bankless team

P.S. Our Monday Mint episode with Punk6529 is live! Collect a limited edition copy of the episode now (only a couple left!)

Crypto Is Under Assault

Bankless Writer: Donovan Choy

After a wildly challenging last few months of 2022, the crypto industry spent much of January attempting to rebuild. Markets recovered somewhat, FTX-exposed enterprises started to pull out of the wreckage and builders asked “What’s next?”

In the first couple weeks of February, we’ve seen regulators descend on the crypto space with the self-professed mission of cleaning it up for investors, but they’re doing so through shutting down services and fining American companies rather than working with them to help create safeguards for consumers while staying competitive with overseas alternatives.

Last week, in an unprecedented move, the SEC fined Kraken $30 million for failing to register their staking service as a securities product offering. Kraken’s staking service offers yields as high as ~21% to clients for locking up various cryptocurrencies to be staked on a corresponding PoS blockchain.

In response, Kraken announced that it would unstake all previously staked assets and halt its staking services for American users, with the exception of staked ETH which is locked up as per Ethereum protocol rules until the Shanghai upgrade in March.

Is the SEC banning crypto staking across the board? If so, should the industry be gravely concerned?

Coinbase doesn’t appear to be worried. The largest U.S. crypto exchange is taking the line of argument that Kraken fell foul of securities laws because its staking yields were additionally derived from an active form of investment.

In the official SEC press release:

… since 2019, Kraken has offered and sold its crypto asset “staking services” to the general public, whereby Kraken pools certain crypto assets transferred by investors and stakes them on behalf of those investors… Kraken touts that its staking investment program offers an easy-to-use platform and benefits that derive from Kraken’s efforts on behalf of investors, including Kraken’s strategies to obtain regular investment returns and payouts.

Unlike Kraken, Coinbase claims that yields from its staking services are solely determined by supply and demand forces based on the proof-of-stake consensus mechanisms of the underlying blockchain protocols.

Here’s what their POV boils down to: staking is presumably fine in the SEC’s eyes if crypto companies are merely taking your crypto and running a validator node for you. When the SEC knocks on your door, Coinbase can say “we’re not investing for our clients, all we’re doing is running a managerial service to secure the blockchain, no Howey Test violation here”.

But they argue that Kraken (or Nexo who also recently halted their Earn product) can’t use that same argument because their product is in effect: “We’ll not only put your crypto to work running a validator node, we’re also making active investment decisions!” Whether or not the SEC buys Coinbase’s argument and leaves the rest of centralized crypto staking alone is up for debate.

The problem is that even if Kraken purports to offer its staking service as a security product (they don’t), the SEC isn’t showing the green light to anyone.

To-date, there is not a single known case of an American crypto company having successfully registered its yield product as a security. This despite Gary Gensler’s claims in a CNBC interview that all would’ve been OK if Kraken had simply registered using “a form on our website with our disclosure review teams”.

I find the SEC’s “all crypto projects have to do is come in and register” line unbelievably insulting.

— Jason Gottlieb (@ohaiom) February 11, 2023

It assumes there’s this vast quantity of sophisticated securities lawyers advising clients, “nah man, screw the SEC, yolo baby, do whatever you want.” 1/6

SEC Commissioner Hester Pierce echoes this point in her dissenting statement: “In the current climate, crypto-related offerings are not making it through the SEC’s registration pipeline.”

Crypto companies may indeed want to follow the rules, but what exactly are those rules, Mr. Gensler?

If the SEC was serious about mitigating the risks involved in crypto staking, there are plenty of low hanging regulatory fruit. For instance, mandating greater transparency for centralized crypto institutions by using proof-of-reserves, or placing a cap on staking amounts. Instead, the SEC opted for a bout of political theater by enforcement of arbitrary standards, all while leaving other players in the same space guessing as to whether their services were actually compliant.

The SEC’s actions change nothing in terms of risk mitigation for Americans.

Suppose we can agree that crypto staking is too risky for small time investors. That is after all, the point of the Securities Act enacted in the wake of the 1929 stock market crash. In the absence of domestic centralized staking options, the hapless masses that the SEC wants so badly to protect can turn to companies outside of the U.S. who offer the same services — even Web2 Fintechs are entering the sector, as seen by UK-based Revolut’s announcement last week to launch its own crypto staking-as-a-service.

Alternatively, users can opt to stake crypto through a permissionless liquid staking protocol like Lido or Rocketpool.

These alternative options can require the average user to scale a much steeper learning curve and open themselves up to new risks. Gensler, who himself taught a MIT blockchain course, is likely more than aware.

But perhaps the silver lining lies in these unintended consequences. Just as with the crackdown on Tornado Cash last year, the SEC’s actions serve as a stark reminder for the endgame of full decentralization.

Even in its partially-decentralized state, Lido is already proving that point. Today, Lido controls 29% of staked ETH on the Ethereum beacon chain. Contrary to popular opinion, Lido is not one single entity. Its war chest of ETH is passed onto 30 node operators who stake them through thousands of nodes, making the protocol far less vulnerable to Gensler’s next surprise.

The SEC can order some of these U.S.-based individual node operators to shut down their nodes. But that would likely only disrupt Lido temporarily, as they cannot stop every node operator.

Distributed validator technology (DVT), an area of research that the Ethereum foundation has pursued since 2019, is also set to further decentralize node validation. DVT uses multi-party computational (MPC) processes to enable co-running of nodes by different entities sharing a private key, allowing nodes to keep running even if one entity goes down.

The SEC’s clumsy handling of Kraken illustrates one thing: regulators can hamper their citizenry’s access to crypto, especially through centralized services, but crypto itself is unassailable because its technological foundations are decentralized.

That will only grow to be truer overtime.

🙏 Together with ⚡️ACROSS⚡️

Across is the bridge you deserve: fast speeds, low fees, great support, no hacks, and we love our users. Try it once and you’ll understand why Across users love us back and have bridged $billions with it.

Yield farmers will also find attractive yields for providing bridge liquidity! 👀

👉 If you have questions, check Twitter or the Discord!

MARKET MONDAY:

Scan this section and dig into anything interesting

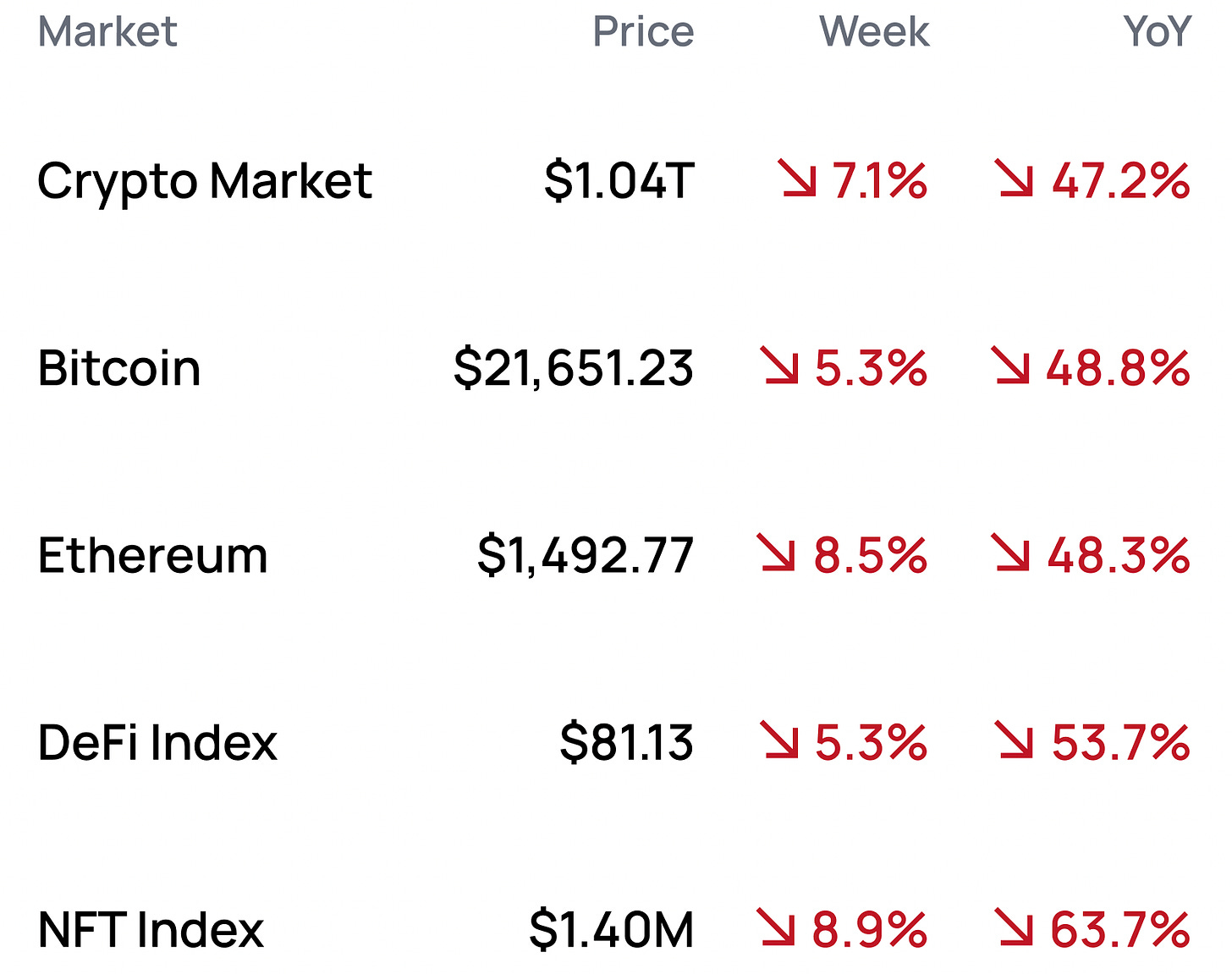

Market Numbers 📊

*Data from 2/13 2:00 pm EST (DeFi Index = $DPI, NFT Index = $Blue-Chip-10)

Market Opportunities 💰

- Lend and borrow rETH on Aave V3

- Privately borrow LUSD using Liquity on Aztec

- Check your eligibility for the Optimism airdrop

- Earn curator rewards on Sound

- Access US Treasures on-chain with Flux Finance

Yield Opportunities 🌾

- USD: Earn 28% LPing the USDT-USDC pool in Camelot on Arbitrum

- USD: Earn 24% LPing the USDT or USDC pool in IPOR on Ethereum

- ETH: Earn 22% LPing the alETH/ETH pool in Velodrome on Optimism

- ETH: Earn 16% LPing the frxETH/ETH pool in Velodrome on Optimism

- BTC: Earn 4% LPing the sBTC/WBTC pool in Curve on Ethereum

What’s Hot 🔥

- Reddit NFTs are popping off

- Aave’s GHO stablecoin launches on the Goerli Testnet

- Gaming tokens rip to start the year

- Lido announces their V2

- Hadeswap buys Solana Monkee Business

Money reads 📚

- State Of the Network: Issue 193 - Coinmetrics

- Bent too Far - How Umami’s Institutional Ambitions Almost Tore the DAO Apart, Forcing out CEO - Samuel McCulloch

- Thread on Ethereum Staking Withdrawals - Korpi87

- Ceteris Paribus: What is Euler Finance? - Sooper

- Thread on Tracking Whale Wallets - Thor Hartivigsen

- Read - Introducing Infinity Pools: Or how I learned to stop worrying and love leverage

Governance Alpha 🚨

- Uniswap votes to deploy on BNB Chain

- Aave looks to freeze BUSD markets on V2 Ethereum

- ENS explores reducing renewal fees

- RAI considers ending FLX staking

- Synthetix moves towards launching V3

Trending Project: Umami Finance 📈

Analyst: Ben Giove

- Ticker: UMAMI

- Sector: DeFi - Asset Management

- Network: Arbitrum

- FDV: $9.1M

- Hotness Rating: 🔥🔥

- Umami is an Arbitrum based asset management project. Umami is developing delta-minimized vaults on GLP, the liquidity pool token of GMX, which will hedge out price exposure to the assets in the pool. Umami is governed by the UMAMI token, which upon the release of the GLP vaults, can be staked to earn 50% of the revenue generated by the product.

- Umami has been embroiled in controversy over the past few weeks. The drama first began on January 31, when the former lead of the project, Alex O’Connell, announced that the project would stop distributing ETH payouts to UMAMI stakers. Previously, Umami shared a portion of the yield generated by the project's treasury with stakers. The price of UMAMI fell 37.9% in the immediate aftermath of this news.

- Things escalated on February 8, when it was revealed that the Umami team resigned from their positions at Umami Labs, the company leading development on the project, due to O’Connell’s management. Per an article from Flywheel, O’Connell had been attempting to seize the assets held in the Umami DAO treasury by placing them under the control of Umami Labs. After the team’s resignations, O’Connell left the project and sold his UMAMI position, netting himself roughly ~$500K. This caused the price of UMAMI to briefly wick to near zero before recovering. Umami currently trades at a price of $9.17, which represents a -76.5% decline from its 52-week high of $39.10.

- Although we are still in the immediate aftermath of O’Connell’s rage quit, the Umami team and community appear to want to keep the project going and launch the GLP vaults. A proposal by community member Crypto Condom which suggests re-implementing fee-sharing and transitioning the project to a full DAO model, is making its way through Umami governance and appears to have early community support. This decision may also be influenced by the fact that Umami trades above the value of its non-native treasury assets (RFV) which as of writing is $5.68 per UMAMI.

Hotness Rating (🔥🔥/5): Umami is in crisis following the unceremonious (to put it lightly) departure of its former CEO. While it’s possible that the Umami brand is permanently tarnished, the transition to a DAO model and successful launch of the GLP vaults could breathe new life into a project which had already once been left for dead as an ex-OHM fork. Given that UMAMI currently trades ~1.7X above RFV, it’s unlikely that the DAO will vote to dissolve and return treasury funds to tokenholders in the short-term. Perhaps UMAMI will have an end of 2020/early 2021 SushiSwap style resurrection, but between trading above RFV and the massive near-term risks facing the project, non-degen investors may want to take a wait-and-see approach before adding it to their shopping carts.

Meme of the Week 😂

me in the US after buying 0.1 cbETH pic.twitter.com/ccGMSHl1ux

— Bankless (@BanklessHQ) February 9, 2023

Job opportunities 🧑💼

- Uniswap Labs: Senior Software Engineer, Protocols

Browse more roles (or add your own) at the Bankless Jobs Board