Easy Money or Greatest Ponzi? ($)

View in Browser

Sponsor: Brix — Access real-world yield in DeFi. Built on MegaETH.

- 🟠 Bitcoin Developer Coalition Floats BIP-361 to Freeze Quantum-Vulnerable Wallets. Bitcoin’s current quantum defense plan seeks to solve a future threat at the detriment of its most sacred rule.

- 💸 Tether Leads $150M Drift Post-Hack Recovery Effort. The recovery plan includes the issuance of another Drift token and will see the Solana-based perpetuals exchange adopt USDT.

- 🇺🇸 CFTC's Selig Credits AI Efficiency Amid Staffing Crunch. Proper enforcement in markets remains a "top priority" for the federal derivatives regulator.

| Prices as of 6pm ET | 24hr | 7d |

|

Crypto $2.53T | ↗ 0.7% | ↗ 4.0% |

|

BTC $75,097 | ↗ 0.2% | ↗ 3.7% |

|

ETH $2,349 | ↘ 0.9% | ↗ 6.1% |

Market Plays:

- 🪙 Trying Apyx

- 🌈 Staking $RNBW

- 🥏 Exploring Blank on Solana

- 💼 Trading Nado’s megacap perps

- ⛏️ Trading GMX’s XAU & XAG perps

Hot Reads:

- 🌉 Bridging the Yield Gap — Ross

- 💳 Crypto Debit Cards 2026 — defiprime

- 🔮 A Guide to Perpetual Futures — Jay Drain Jr.

- 💸 How Many Traders Are Profitable on Polymarket — Andrey Sergeenkov

- 🐈⬛ Hyperliquid: In Singapore with Jeffrey Yan — Dom Cooke

Farming Opps:

- 🟠 BTC: 6% APR with Ekubo’s LBTC-WBTC pool on Starknet

- 🟠 BTC: 2% APR with Vesu’s WBTC vault on Starknet

- 🔵 ETH: 5% APY with Pendle’s agETH PT on Ethereum

- 🔵 ETH: 10% APY with Convex’s ETH-cbETH vault on Ethereum

- 🟢 USD: 8% APY with Pendle’s sUSDai PT on Arbitrum

- 🟢 USD: 8% APY with Convex’s USDC-RLUSD vault on Ethereum

Airdrop Hunter:

- ⭐️ Grove: Hunt Grove airdrop

- 🤖 USDai: Claim CHIP allocation

- 👄 Fluent: Claim BLEND airdrop

- 😨 Fomo: Explore airdrop opps

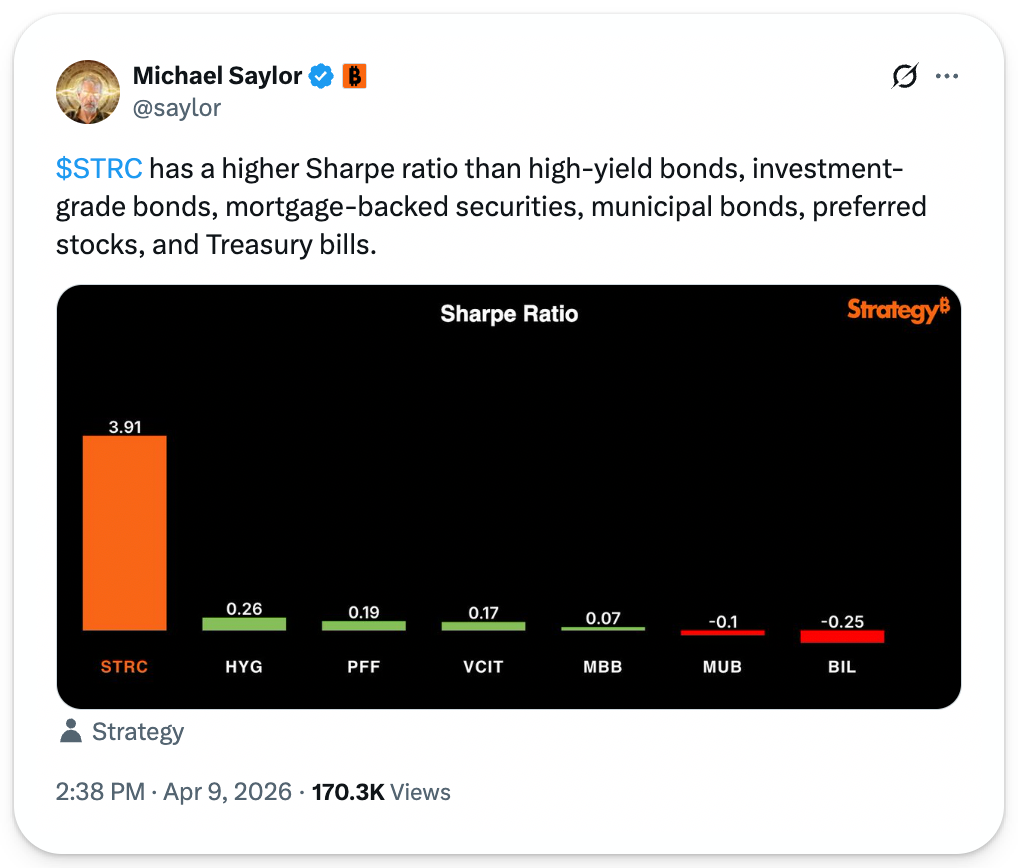

Depending on who you ask, STRC is either "the greatest ponzi known to man" or "mathematically the best risk-return credit instrument in the entire $200T+ credit market."

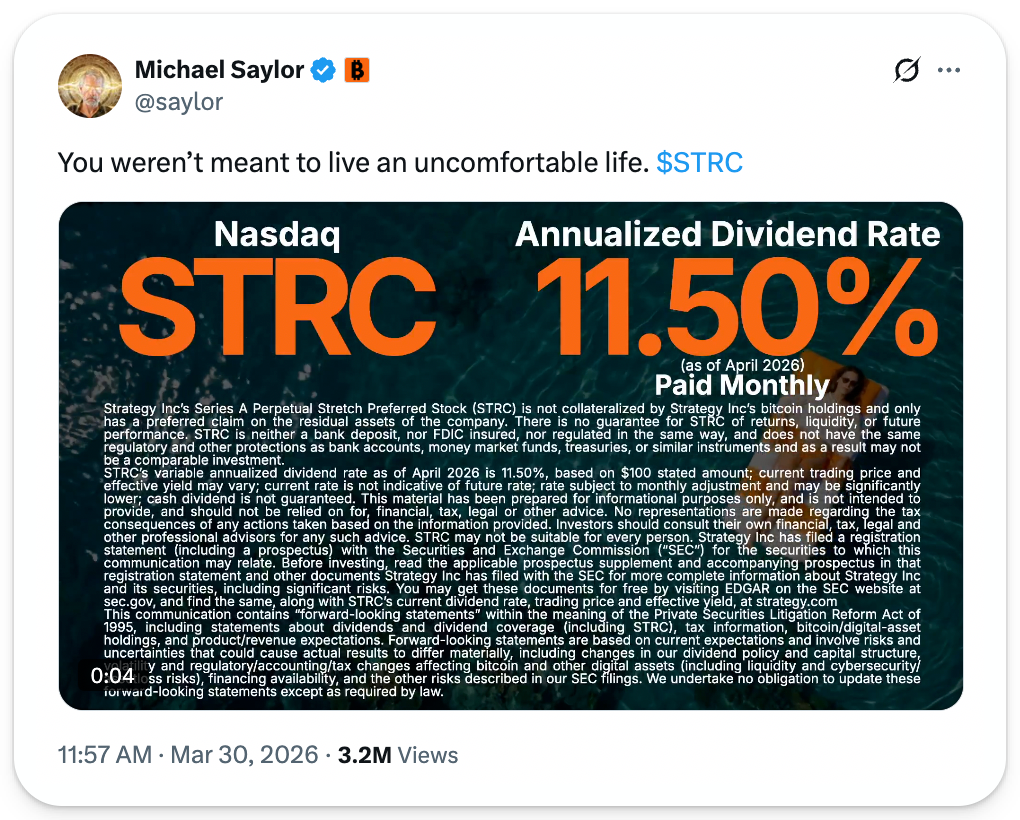

This so-called “perpetual preferred stock” currently pays its shareholders 11.5% annual dividends, accruing monthly, and is backed by the full faith and credit of BTC treasury behemoth Strategy.

While STRC experienced another ex-dividend drop on Wednesday, effectively shutting off Strategy’s access to this lucrative funding spigot, the DATCo already secured an estimated $1.2 billion via STRC earlier this week, enough capital to fund the purchase of ~17.2k bitcoins.

Understanding STRC

STRC (pronounced “Stretch”) is a publicly traded security on Nasdaq Exchange.

A modern marvel of financial engineering, STRC touts extraordinary yield for income-focused investors – conveniently packaged as a relatively stable instrument that helps Strategy raise capital to buy more bitcoin without selling MSTR common stock.

Unlike Strategy’s once-prevalent convertible bonds (last offered in February 2025), which are rule-based, fixed-term instruments with predefined coupons, maturities, and conversion terms, STRC’s structure is far more flexible.

STRC is not debt, meaning Strategy has no legal obligation to pay dividends or repay principal. However, it sits above common stock (MSTR) in the capital stack, providing holders with a preferred claim to Strategy’s residual assets in a liquidation event (after payments are made to bond holders), but the securities themselves are not directly collateralized by bitcoin.

Dividend payments are variable and set monthly by Strategy, currently amounting to 11.5% annually on the $100 stated amount, paid monthly in cash. This structure gives Strategy full discretion to dynamically adjust payouts in response to market conditions, enabling the firm to lower dividends when demand is strong and increase payments when demand softens.

Although dividends are cumulative, allowing missed payments to accrue and compound, there are no contractual default triggers if dividend payments are skipped. In practice, this leaves STRC holders with no recourse, as missed payments do not confer the same rights as afforded to Strategy’s convertible bond holders.

Risk–Return Profile

For Strategy, STRC delivers maximum optionality, allowing the DATco to raise money today in exchange for the promise of future dividends, which will return capital to the instrument’s holders over a multi-year period (approximately 6.2 years assuming holders continually reinvest their monthly dividend checks, or 8.7 years assuming they retain the cash).

So long as Strategy can maintain these dividend payments – supported by the continued performance of its BTC treasury strategy – the firm can raise theoretically infinite amounts of capital to buy more bitcoin, propping up the token’s price in the process to bolster the value of its holdings, and enabling it to buy even more bitcoin.

For investors, STRC delivers above-market monthly cash yields with reduced volatility compared to MSTR common stock, and the promise it will trade in a tight band around $100.

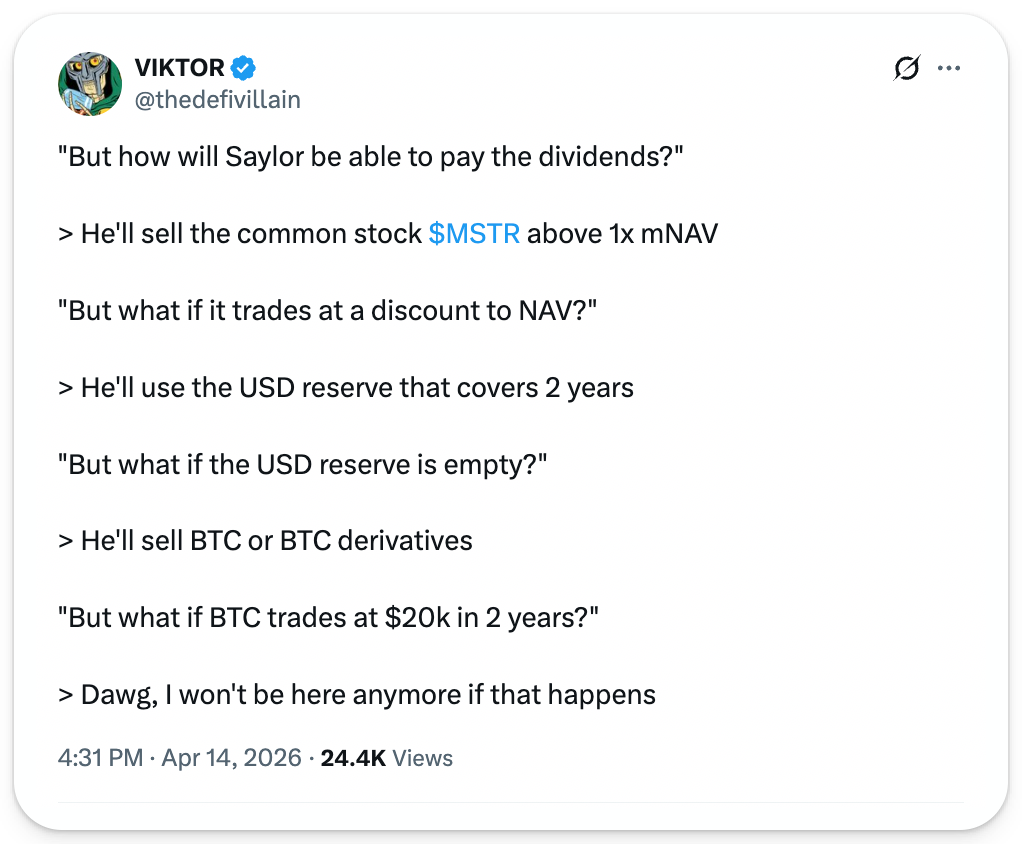

Still, there is no free lunch in finance: the same flexibility that makes STRC attractive to Strategy makes the security a risky gambit for its predominantly retail holderbase.

At any time without warning, Strategy can choose to reduce or defer the interest payments it previously promised to pay out to STRC holders (developments bound to materially impair the instrument’s value), and there is no guarantee of long-term sustainability should BTC falter.

This inherently unstable yield dynamic has drawn plenty of Crypto Twitter comparisons to the ill-fated Terra experiment, an algorithmic stablecoin project propped up by the promise of 20% returns that imploded in spectacular fashion after the price of the ecosystem’s native LUNA token collapsed into the abyss.

Further, while demand for STRC has been insatiable, its structure bears an uncomfortable resemblance to that of a Ponzi scheme, requiring a continual inflow of new investor capital to sustain the offering, as the total revenue generated from Strategy’s core software operations ($477M for 2025) is insufficient to cover its $1.2B annual dividend obligation.

Stretching for Yield

Strategy has deliberately stashed $2.25B in a dedicated USD liquidity fund to cover dividend obligations if new funding dries up, but the reserve can only sustain payments for roughly 22 months, placing the company at risk in the event of a prolonged BTC bear market.

In an absolute worst-case scenario, Strategy could offload its 780k BTC reserve (worth $58B at current market prices) to theoretically fund dividend obligations for 47 years. The question remains whether an option like this would impact underlying confidence in Strategy, putting pressure on the value of its reserves and undermining the company’s thesis of raising capital at attractive terms to accumulate and hold BTC indefinitely.

Whether STRC proves to be a durable financing innovation or a fragile yield machine will ultimately depend on Bitcoin’s trajectory and continued investor appetite – variables Michael Saylor, at least, appears to have little doubt about.

Emerging markets provide some of the best yield on Earth. Opportunities shouldn't be constrained by geography or capital. Brix provides access to real yield, not made-up onchain mechanisms. Let the Yield Flow.

Not financial or tax advice. This newsletter is strictly educational and is not investment advice or a solicitation to buy or sell any assets or to make any financial decisions. This newsletter is not tax advice. Talk to your accountant. Do your own research.

Disclosure. From time-to-time I may add links in this newsletter to products I use. I may receive commission if you make a purchase through one of these links. Additionally, the Bankless writers hold crypto assets. See our investment disclosures here.