Level up your open finance game three times a week. I’m releasing this Free for Everyone until November 1. Get the Bankless program by subscribing below.

Dear Crypto Natives,

Market Monday! Every week I scan the open finance market to surface the best opportunities and insights for us.

On days like today I include a longer opening note…

Because before we do the how, we have to know the why.

Why are we doing this—why bankless? Because crypto is more than Hold. It’s Lend, Borrow, Stake, Invest, Spend, Earn, Trade, and Bet too—a complete money system. One with less banks and more sovereignty.

If we’re going to thrive in this parallel financial system we need all the money verbs and we need them as bankless as possible. We can’t get stuck like Charlie Shem did this week in a tribalistic fear of trying new things. (Charlie changed his mind btw 🔥)

This doesn’t mean we accept everything and descend into crypto relativism.

Bankless is the art of navigating the extremes of maximalism and relativism. And we can’t navigate on the word of people with misaligned intentions. Neither can we let our ideas be subverted by narratives of the moment.

We navigate by using crypto money—all the verbs.

By using crypto we become the primary source. The experts. The most informed.

We make better decisions. We increase our crypto wealth. We level up.

We go bankless.

Now that we know the why we can get to the how…because it’s Market Monday.

- RSA

We hit view source on Compound and learned a few things. The big questions in crypto often come down to this—who’s got the keys to the safe?

MARKET MONDAY:

Scan this section and dig into anything interesting

Market numbers

- ETH up to $184 from $171 last Monday

- BTC up to $10,498 from $9,796 last Monday

- Maker stability fees eased down to 14.5% from 16.5%

Market opportunities

- (Lend) BlockFi added Flex (e.g. lend in BTC get interest in ETH—1% fee)

- (Lend) DyDx with best DAI lending rate—above 11%

- (Trade) with lowest slippage in DeFi (no custody—good for big orders)

- (Borrow) wBTC at 3.7% on Compound seems like a steal

- (Give) Pool money and donate to a cause

- (Bet) on sports event (doubt we’ll see big bets until they support DAI)

- (Lend) BlockFi still with best rates—ETH at 3.30% & BTC at 6.2%

New stuff

- Monolith users unboxing their crypto credit cards

- Liking this experiment by Nick Sawinyh on stablecoin lending

What’s hot

- ETH locked in Set up 890% this week!

- 236k more ETH locked up in DeFi last month

- DAI loans comprised over 60% of new loans originated last week

Money reads

- On Supply Caps like 21m (read memetic part) - Arthur Breitman

- Supply impact of ETH (p.s. wrong on ETH issuance numbers) - TradeBlock

- Brilliant manifesto that also applies to ETH (he’ll get there) - Nic Carter

- Use Ethereum if you want it to succeed — RSA

- Recap comment on current DeFi risks (i mostly agree) - Limzero

WHAT I’M DOING

Check out a few opportunities I’m capturing right now with my crypto money

Entering a no-loss lottery. I entered the PoolTogether no loss-lottery for the experience (you can’t make money on it—the EV is same as lending on Compound, only with extra smart contract risk). The concept appeals to mass psychology though. Entrants pool DAI into a lending protocol by buying $1 Lotto tickets and one lucky entrant wins all the interest at the end of 7 days. Lose? You get your money back. I put in $3 for a .004% chance of winning $100 or so. With some UX, globally permissionless lotteries may easily go mainstream. And if they do, I wonder how much DAI gets locked up? In the meanwhile the pools keep getting bigger.

Lending ETH on Binance. Well I would have if Binance wasn’t shutting down in the US (re-opening later). I’ll explain. Binance launched a crypto lending product. Their second lot included crypto money. Lending deals were good. ETH at 6% fixed is incredible. The catch: the deals are sold in lots so you have to be quick and the term is short (14-days). Bigger catch: how great do you feel with your money in a hazily regulated crypto bank casino? My answer: Not great. Fine to test in small test amounts, nothing more. If your faith in CZ is strong and you’re not in US, check their next lot in a couple weeks. For me this was only exploratory—a look at the future of crypto bank lending products. Where Binance goes Coinbase cautiously follows.

WEEKLY ASSIGNMENT:

Make time to complete this assignment before next week

Send a first transaction via InstaPay (20m). InstaPay is a payment channel. It scales payments on Ethereum while preserving security. Like Lightning. I want you to use it to send a transaction.

First, get an invite for Metamask on your mobile. Use the guide if you need help. Store any key phrases. Make sure you have .03 ETH or more in the wallet.

Now:

- Turn on InstaPay in App: Settings > Experimental > Payment Channels

- Go to InstaPay and Deposit .03 ETH

As you deposited ETH it was automatically converted to DAI. You’re now ready to send the DAI to someone. If you know a crypto native, try sending a few cents of DAI to their ETH address. Or send a few cents to my address. Here’s the QR Code.

{kind=link}

What is this magic? It’s the payment channel tech that will be integrated in every wallet and used to scale Ethereum payments to near Visa-like speeds. Doesn’t clog the main chain. Transaction costs low. And it’s here today. See? Magic.

Extra Credit Learning

- (Beginner) Check fast vs standard Gas prices just for fun (bookmark this site)

- (Beginner) Video: Arianna explains money protocols (first 12 mins)

- (Intermediate) Learn how to open a Set (I like 20 day MA ETH)

- (Intermediate) Video: Using Compound with Ledger

- (Advanced) Learn about DeFi Synthetic Assets

MAIN TAKES:

Read my takes but draw your own conclusions

- What you should know before using Compound. Ameen wrote a fantastic piece on Compound risks. Let’s acknowledge first that having “view source” on a bank is the thing that makes open finance magical. So what did we see in the source code? Three classes of risk: 1) hack 2) custody 3) bank run. Security practices limit the first. Bank run risk exists in all lending, at least it’s transparent. Custody risk was my main concern. Custody risk in Compound is similar to Coinbase—if evil, they could steal your money. Considering their pedigree this seems unlikely. And in the end I was satisfied with Compound’s plan to accelerate custody risk mitigation. They’ll do it. Not just because they’re mission-driven but because the community will hold them accountable. View source is powerful.

- Get ready for lower DAI interest rates because as long as the price of DAI remains above a dollar Maker will continue to ease its stability fee—we’ve now seen two weeks of 2% consecutive drops ending at a 14.5% stability fee as of now. Maybe a good indication for DAI demand or a bad indication for ETH margin longs. Maybe both! Given there is now so much DAI locked in money protocols I think we’re seeing evidence of the former. Either way, don’t expect double-digit interest rates on lending protocols to last while the stability fee is moving down. Apps depending on high DAI rates may want to monitor this closely.

- Money startups will drive protocol growth. New money lego startups are now emerging everyday. Take Idle Finance. A mashup of Compound + Fulcrum + DAI with a Wyre API. A startup can create an interest-rate optimizing virtual bank in weeks. Basically impossible to do on legacy finance rails. Most of the experiments in recent ETH hackathons are open finance. The vast majority of startup incubator projects are choosing Ethereum. I think we’ll about to see an explosion of new money lego startups. Some will thrive, many will die, but the winners will provide fresh users for the money protocols.

MINI TAKES:

- Maker launching an new price oracle makes me consider the growing influence of money protocols on their host chains—Maker and others will almost certainly play a role in deciding the fate of future hard forks or governance decisions

- Crypto credit cards seem almost worth trying and I particularly like the approach approach Monolith is taking (UK only for now)—if you’ve had experience with one reply to this tweet and share

- Glad to see Paxos release gold IOUs on Ethereum because apparently DigixDAO forgot to execute a growth plan even after a two-year head start

- I’m still dying for a good mixer for ETH address privacy and while it seems like they’re finally coming none are ready for primetime—people still obfuscating transaction trails by hopping funds through centralized exchanges

- The VanEck BTC ETF announced this week is not really an ETF it’s just a trust product like Grayscale—if you’re trying to get BTC in a retirement account I still recommend jail breaking your IRA as a first step

- Binance issuing a stablecoin on Ethereum instead of their own Binance chain says it everything—banks will launch assets on the most neutral chain

- Ledger supporting ERC20 probably means in near future you’ll be able to bank using money protocols inside the Ledger Live app

TWEET-A-QUESTION

Tweet me your question—I reply to one per week

David Sherry:

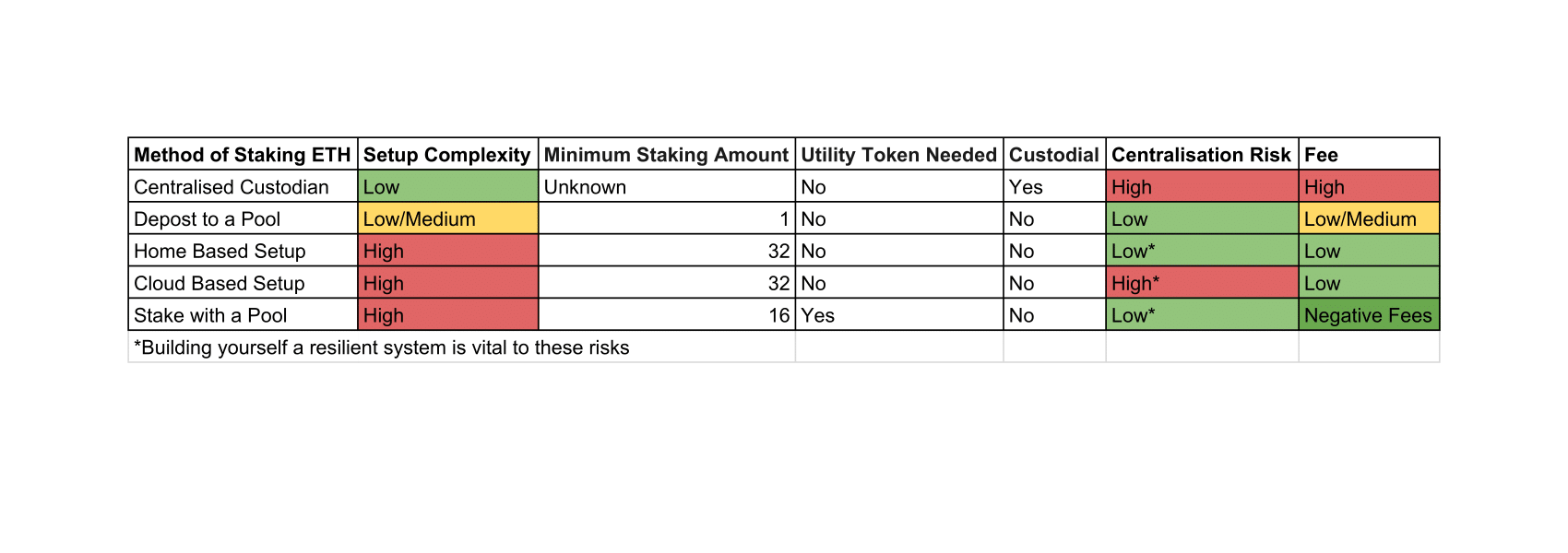

Hey RSA, how many ETH will you need to stake when it’s ready?

RSA:

If you want to run your own node you’ll need at least 32 ETH to stake. Running your own node requires running ETH 2.0 client software. A consumer laptop should be fine for this. If you want someone else run your node you’ll be able to stake with less then 32 ETH in a non-custodial staking pool or on custodial exchanges like Coinbase.

Upon launch staking participation will require more expertise and more risk. But it’ll get easier and less risky over time. Eventually, staking will be the least risky way to lend ETH. I expect the interest rate on staking to become the risk-free rate of ETH in the Ethereum economy—just as lending USD to the US via T-bill is the risk-free rate of money in the US economy.

Cool right?

P.S. This chart on staking is a pretty accurate

{kind=link}

Some recent tweets…

Actions

- Execute any good market opportunities you saw

- Complete weekly assignment: send DAI with InstaPay

Continue leveling up. $12 per month. But 20% off if you subscribe before November 1.

I need your help…

To onboard 1 billion people to open finance. To do that we need to become evangelists. If you believe in what we’re doing don’t keep it to yourself—share Bankless with as many people as possible.

Post. Tweet. Tell.

That’s how we take back our money system.

Not financial or tax advice. This newsletter is strictly educational and is not investment advice or a solicitation to buy or sell any assets or to make any financial decisions. This newsletter is not tax advice. Talk to your accountant. Do your own research.

Disclosure. From time-to-time I may add links in this newsletter to products I use. I may receive commission if you make a purchase through one of these links. I’ll always disclose when this is the case.