Citizen DeFi Play: The Morpho Trade

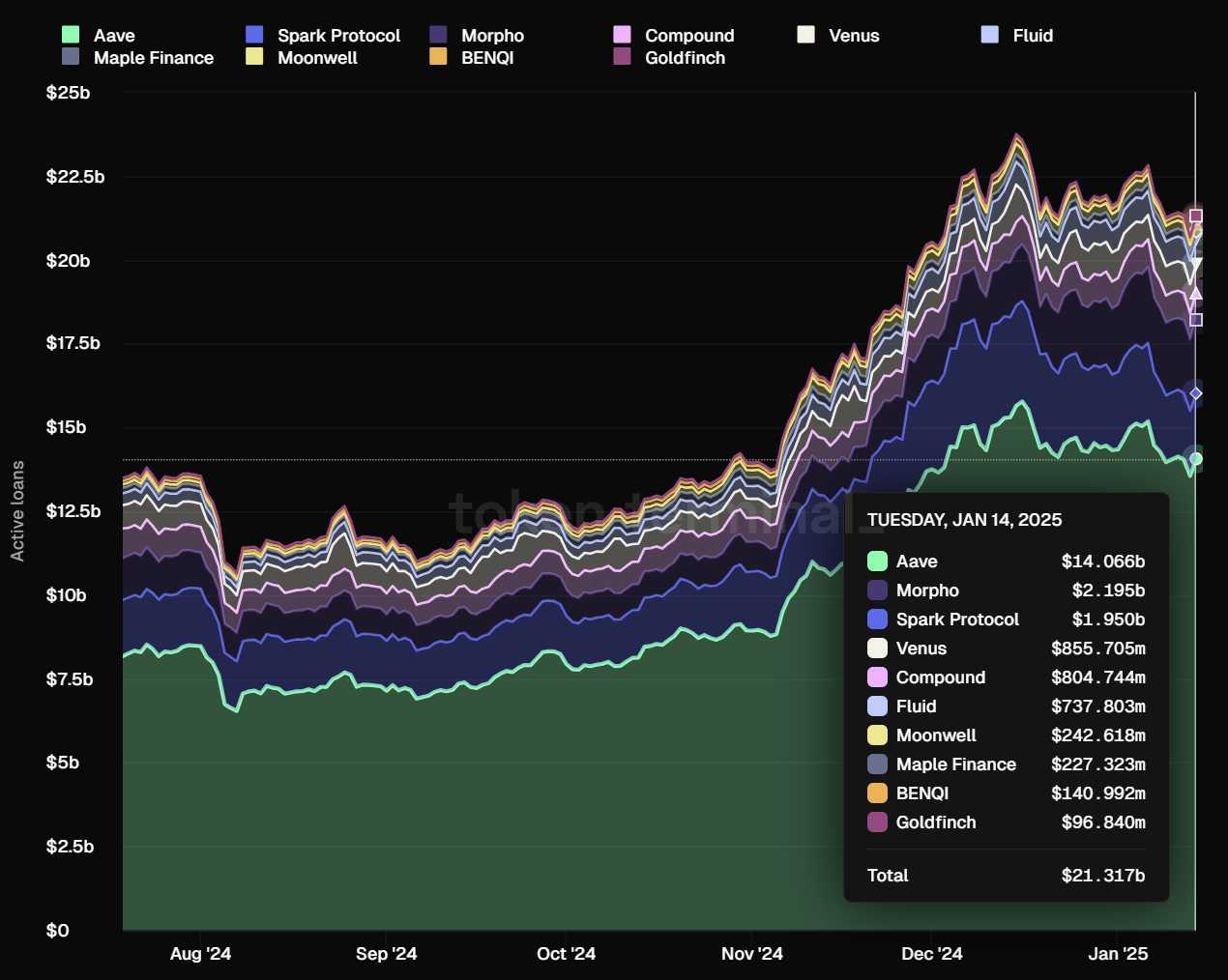

Morpho’s lending markets have exploded in popularity since October, and just last week, Morpho flipped Spark to become crypto’s second-largest onchain lending market!

From custom lending markets to a unique risk management approach, Morpho has redefined what it means to be a DeFi lending primitive. Today, we unpack Morpho’s innovative approach to lending 👇

The Morpho Basics

Morpho’s lending markets may only be available on the Ethereum and Base networks, but that hasn’t stopped the application from becoming a focal point for permissionless onchain lending in recent months.

While Aave enjoyed a brief stint as Base’s dominant lending force after flipping the total value locked inside competitor Moonwell last August, Morpho would be crowned as the new champion in the closing days of 2024. At the time of this analysis, Morpho was the second-largest onchain lending market in existence, with $2.2B in active loans and $3.7B in total value locked spread across its Ethereum and Base implementations.

In stark contrast to traditional lending markets, where protocol governance is responsible for mitigating the risk that a loan “goes bad” (i.e., the value of a borrower’s posted collateral falls below their borrowing amount), Morpho places the onus of preventing losses on its users.

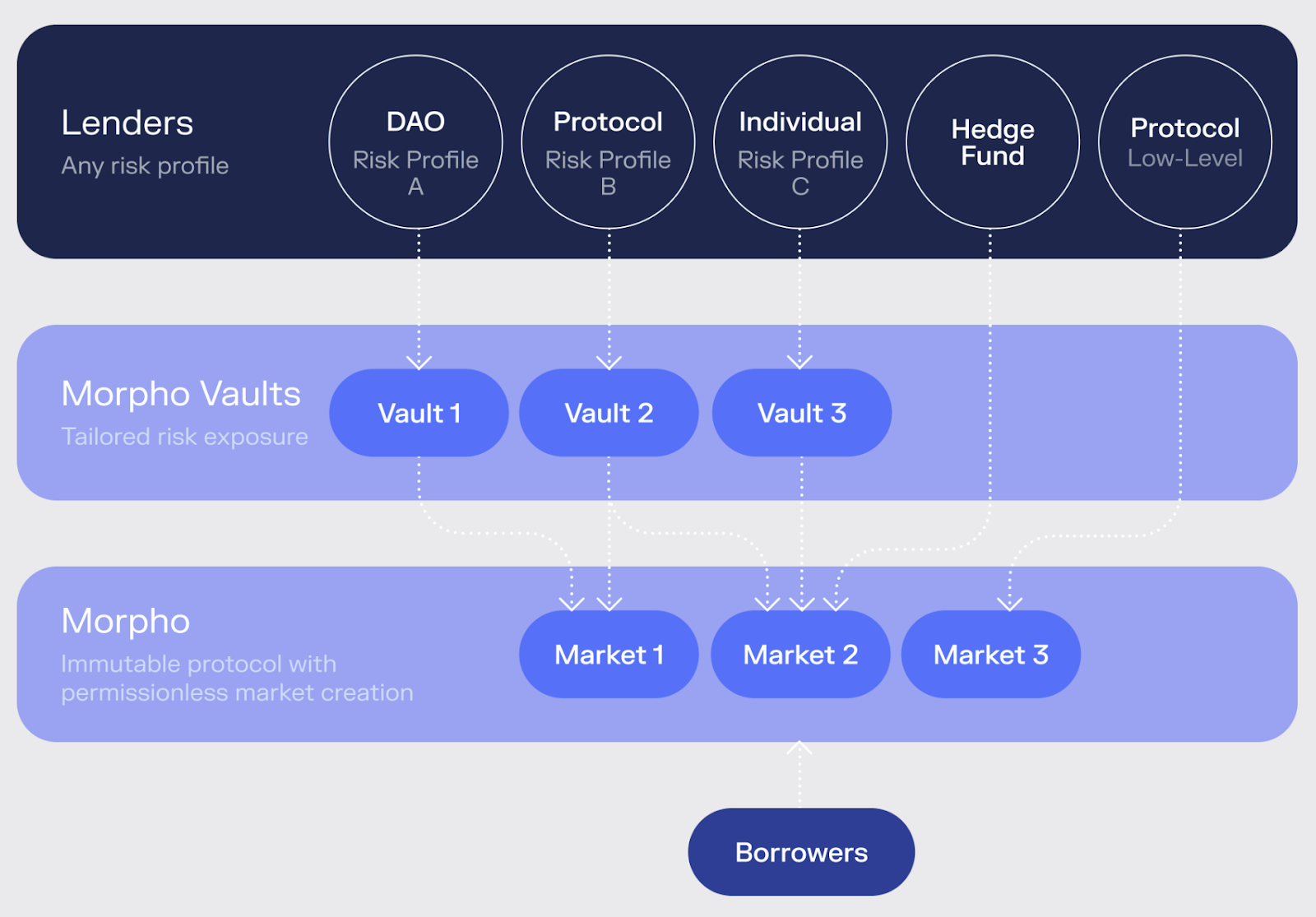

Unlike its competitors, Morpho allows anyone to permissionlessly create custom lending markets for practically any fungible token that is compliant with Ethereum’s ERC-20 standard.

To provide some amount of protection from the risks of crypto-collateralized lending, Morpho’s UI pushes retail depositors to supply tokens into “vaults,” or actively managed lending vehicles created by third parties who use their own discretion to deploy user capital across available Morpho lending markets to earn yield.

Borrowers, on the other hand, must interact directly with the market they wish to receive a loan from but can shop around for available opportunities by collateral/loan token type, liquidation threshold, available liquidity, and borrow interest rate.

If the loan-to-value ratio of a Morpho borrower’s position exceeds the liquidation threshold established for their market, their loan becomes “unhealthy” and can be forcibly repaid. Such liquidations occur when the value of a borrower’s collateral tokens falls, the value of their loan token increases, or too much interest accrues to their position.

Like many other lending markets, Morpho relies on utilization-based interest rate curves to autonomously price interest rates based on market supply and demand dynamics. Should unused lender liquidity suddenly evaporate from a market, borrowers will be subject to egregiously high interest rates, which compel position closure and incentivize new deposits into the market.

Since protocol inception, the MORPHO token has been emitted as a borrower subsidy and lender reward. It became transferable on November 21, 2024.

As risk management responsibilities fall on lenders and market creators, MORPHO holders play a limited role in protocol governance but can vote to enable optional fees to collect up to 25% of the interest payments made in any market.

Advanced Applications

Morpho may sacrifice capital efficiency by isolating lent funds to specific borrow pools, but this trade-off enables the protocol to venture into uncharted territory that other lending platforms wouldn’t dare explore!

With the risks of insolvency isolated exclusively to lenders who opted into a given pool, Morpho can offer extremely high-leverage loans on high-risk assets that no other bluechip lending market would be willing to make.

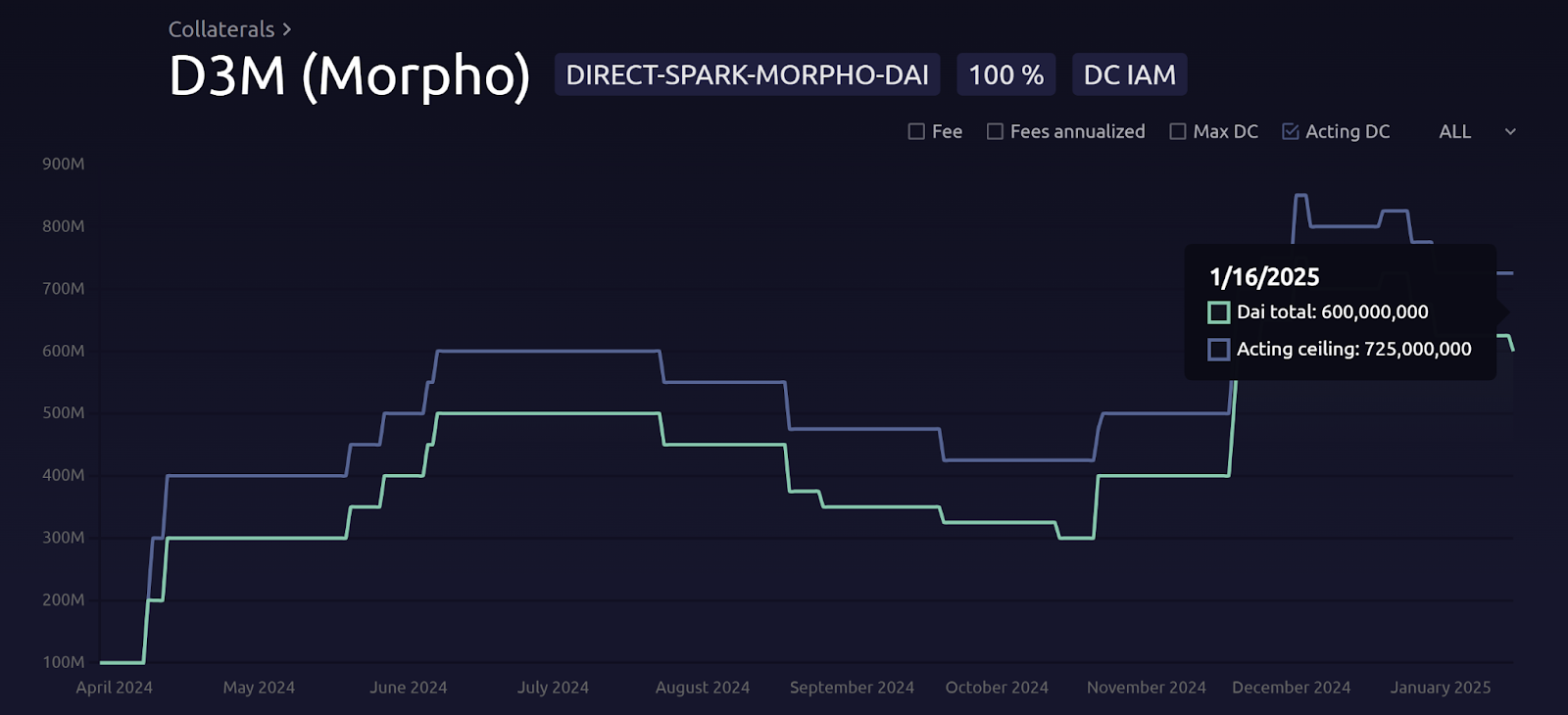

MakerDAO notably composed its lending operations with Morpho beginning in late March 2024 to tap Ethena’s lucrative synthetic dollar yields and now supplies $600M of DAI liquidity (down from $750M in December) across various markets, including high-risk Pendle PT pools.