How Will Bitcoin Handle This Halving?

The quadrennial Bitcoin Halving is yet again upon us, scheduled to occur later tonight, and will programmatically reduce the block rewards paid out to miners by 50% for the fourth time in history!

Many have attempted to prophesy the potential impact of this event on BTC price, but the arrival of the Halving raises another equally important question: how will Bitcoin afford its security budget going forward?

Bitcoin miners are (primarily) profit-motivated actors and will only operate when the combination of income from inflationary block rewards and transaction fees exceeds their costs; the Halving will reduce emissions and drastically increase miner dependence on transaction fee revenue.

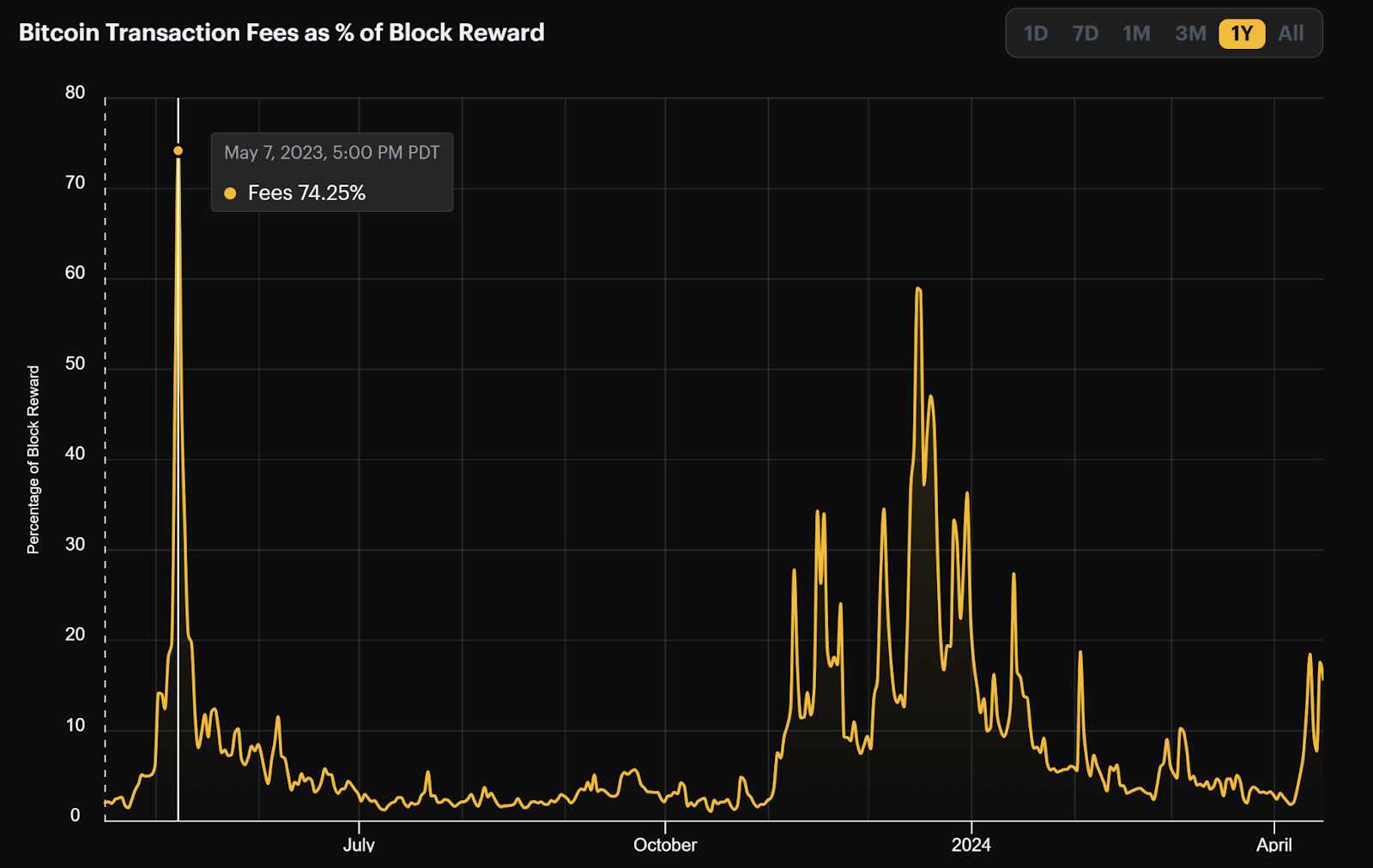

While Bitcoin transaction fees have spiked at times during the past year, comprising up to 74% of the block reward on a single day in the early stages of BRC-20 mania, there is immense volatility in this revenue stream, as demonstrated by the nearly 6-month period following the peak in which transaction fees comprised a low single digit percentage of the block reward.

Speculative demand for various forms of “tokens” and “NFTs” on Bitcoin has been the primary driver of transaction fees, which ticked up in alongside a rally in broader risk markets in late October before staging a resurgence this month as traders positioned themselves for the latest chain’s latest phonomena: Runes.

Existing on the cutting edge with respect to the limitations of Bitcoin and considered by many to have the chance of being the chain’s official fungible token standard, Runes are catalyzing the latest wave of demand for Bitcoin blockspace, with traders hoping that their participation in projects offering exposure to this narrative pre-launch could allow them to cash in big.

next 100x opp is runes on Bitcoin, 95% of CT is not paying attention to this at all

— Ansem 🐂🀄️ (@blknoiz06) April 16, 2024

compare volumes on Solana memecoins to current unisat volume & consider the wealth effect if Bitcoiners have their own native altcoins to buy

provenance will b v imp here also imo

h/t: @0xjakee pic.twitter.com/9ohvBM7rcl

Unfortunately, as attested to by crypto’s numerous boom and bust cycles, speculative fervor only lasts for so long…

Ethereum’s NFTs were cloistered from the early innings of the previous bear market, with floor prices on the Bored Ape Yacht Club collection peaking at 128 ETH as liquid token prices began turning lower in late April 2022, but momentum has largely faded from the scene.

This week a Board Ape sold for under 10 ETH for the first time since August 2021, leaving those who purchased the top down $350k, despite the fact that ETH is trading at nearly the same price as it was two years ago.

First sale under 10 eth …

— bunny 🍌 (@DaBunnyOFFICIAL) April 15, 2024

What went wrong? pic.twitter.com/454MJiq8FY

In the early months of 2024, traders chasing extraordinary returns flocked to all forms of memecoins and other types of vapor, but the past two weeks of price action pushed the vast majority of their tokens (including plays linked to Runes like PUPS) deep into the red.

It would come as little surprise to see this cycle’s crop of memecoins and vaporware reduced to nothing more than capital losses and wallet dust, disappointing HODLers just as they have time and time again throughout crypto’s history.

Given the extreme volatility of Bitcoin’s transaction fee revenue and the fact that it is entirely dependent on speculative activity which can randomly evaporate for prolonged periods of time without warning (as demonstrated above), for the sake of easy math, let’s simplify this value to 0.

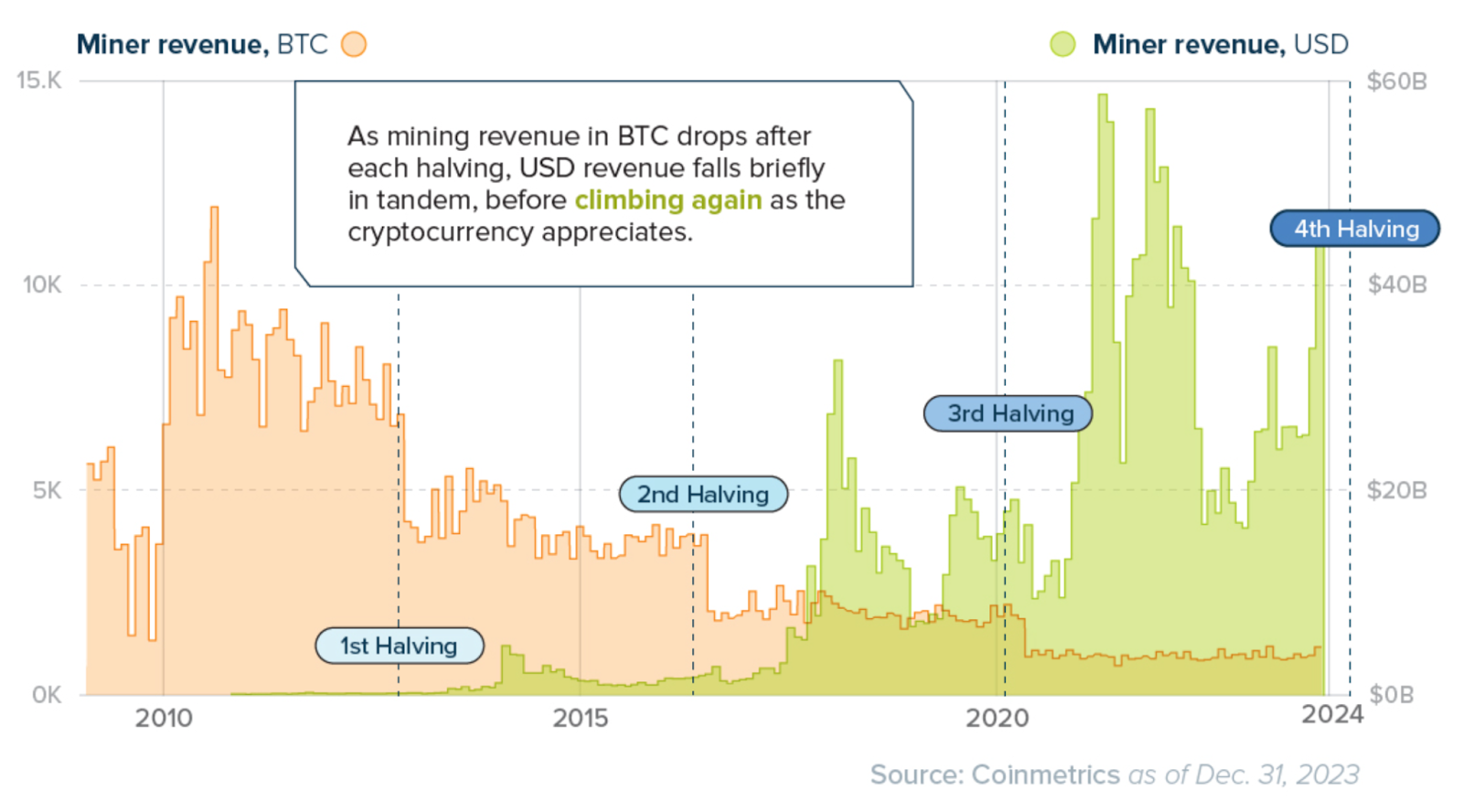

Corresponding with the 50% reduction in block rewards that will occur post Halving, BTC miners will need to double the amount of tokens they produce – or the value of those tokens – to remain profitable and in operation.

During prior Halvings, an equilibrium in which individual miners earn more BTC-denominated rewards has never been achieved.

Instead, Bitcoin’s hash rate – the amount of computing power securing the network – drops following the event before immediately rebounding as the substantial supply restriction imposed by the Halving allows prices to flourish, in turn attracting additional miners who remain profitable despite making less BTC.

The third Halving in May 2020 followed a similar pattern as the first two, but enjoyed the added benefits of a mid-COVID monetary stimulus turned liquidity injection in addition to the Halving-imposed supply constraints.

This Halving, the impacts of block emissions reduction will be smaller than ever, decreasing by 3.125 BTC per block. With Bitcoin currently producing an average of 144 blocks per day, this results in a net supply reduction of 450 BTC per day, worth approximately $27M at current market prices.

To put the minuscule size of this supply reduction into context, BlackRock’s spot BTC ETF alone frequently slurps up hundreds of millions of dollars per day in Bitcoin and has only experienced inflow days of less than $27M on four days (three of which came this week), meanwhile BTC futures markets across top exchanges averaged $80B in volume per day last month!

While the supply restrictions from this Halving should yield a more muted impact on BTC's market price than in the past, the effect on miners and their profitability will be just as severe, meaning this will likely be the first time that hash rate contracts for a prolonged period of time in response to emissions reduction.

Decreasing hash rate on the Bitcoin Network would make it easier to launch a consensus attack on the chain, placing its security at risk.

It is unlikely transaction fees from speculation can counter the decrease in emissions on its own, but Bitcoin supporters are hopeful that the increased adoption of L2 solutions can assist in remedying the issue.

Not only would Bitcoin L2s pay transaction fees, applications built on top of Bitcoin L2s would likely use BTC as their money, and while BTC has already accrued a significant monetary premium and it remains questionable how much marginal value there is to accrue, this could be a factor that helps bolster token price over the longer term!

1/ We recently compiled a list of Bitcoin Layer 2s, but how do they differ under the hood?

— DWF Ventures (@DWFVentures) March 25, 2024

In this thread, we will dive deeper into how we classify these Layer 2s, and walk through Bitcoin's scalability journey to highlight how they aim to leverage Bitcoin as a base layer 🧵 pic.twitter.com/1KnIKFnkAa

Tragically, the vast majority of these chains remain in the concept phase, and even if they were live today, it is unlikely the transaction revenue that they produce would be enough to supplant the reduction in issuance, considering that Ethereum’s much more mature L2s only paid $33M in fees to the L1 during the month of February, making up little more than one day of lost miner revenue.

For Bitcoin, it is likely that some combination of increased transaction fees and a higher token price is necessary to maintain the same level of hash rate post-Halving. Unfortunately, it is doubtful these factors will be supportive going forward…

The Halving is considered by many to be a grail event practically ordained by Satoshi to increase the price of BTC; a failure for historical patterns to hold will almost certainly shake bulls out of this crowded trade.

Only 21 million #Bitcoin

— Bitcoin Magazine (@BitcoinMagazine) April 18, 2024

The halving is soon.

And demand keeps increasing.

Bullish 🚀 pic.twitter.com/Wvt51UU0bc

As discussed above, implementation of L2s is not currently a viable strategy to increase transaction revenues or monetary premium, and with the current nexus of onchain entirely due to speculation, if the price of BTC continues to trade lower, all of this activity is at risk of vanishing from the chain.

The last Halving resulted in a fairly immediate 25% reduction in Bitcoin’s hash rate, but should the price of Bitcoin continue to plunge after emissions are abruptly halved and miners lose 50% of their BTC-denominated income stream overnight, an increasing amount of hash power would be forced to come offline, worsening Bitcoin’s security issues this time around.

Those who found themselves fleeced by Ethereum’s Merge in September 2022 are all too familiar with the failure of emissions reductions on the margin to produce a meaningful impact on price.

A similar trade could be playing out for Bitcoin, which would wreak havoc on the network’s economic security, potentially forcing the community to alter the BTC issuance curve, leading to questions regarding BTC’s entire value proposition and challenging its status as crypto’s leading blockchain.

Bitcoin’s endgame solution for circumventing the Halving’s inevitable hardships on miners has always been increasing the number of use cases for its blockspace, but with emissions set to be slashed tomorrow and no silver bullet in sight, it appears development efforts may have come too late to prevent near-term instability.

Feeling feisty today - here are 2 unpopular opinions:

— sassal.eth/acc 🦇🔊 (@sassal0x) November 29, 2023

- The 21m BTC cap will be removed and/or Bitcoin will become a PoS network

- The Bitcoin chain will be sunset and BTC the asset will survive as an ERC20 on Ethereum

These things may happen within the next 10-20 years