Aave’s Next Act

View in Browser

Sponsor: MegaETH — Crypto has new apps, finally.

- 📅 Google Accelerates Post-Quantum Timeline to 2029. The tech giant's quantum and AI team also released a new research paper about threats posed to cryptographic encryption schemes.

- 5️⃣ Five U.S. Regional Banks With $600B Deposits Tokenized with ZKsync. Earlier this month, five regional banks partnered with ZKsync to launch the Cari network; here's why.

- 🌱 Tether Announces USAT Stablecoin Expansion to Celo Network. It marks the GENIUS Act-compliant stablecoin's first expansion beyond the Ethereum L1.

| Prices as of 7pm ET | 24hr | 7d |

|

Crypto $2.34T | ↗ 2.6% | ↘ 3.2% |

|

BTC $68,194 | ↗ 2.5% | ↘ 3.4% |

|

ETH $2,095 | ↗ 3.7% | ↘ 2.6% |

This week, Aave Labs deployed its long-promised V4 lending markets to Ethereum.

Although its current scale is modest – V4 reported just $1.07M in active loans against $4.75M in total deposits at the time of writing – its creators’ ambitions are anything but: Aave Labs CEO Stani proclaimed his team’s latest design as a revolutionary lending breakthrough that stands to unlock markets for entirely new categories of assets.

Today, we’re diving into Aave V4, unpacking what’s actually new with “hub-and-spoke” lending markets and exploring how this design might redefine the future of onchain leverage.

Rather than iterate on its existing V3 lending marketplace, Aave deployed V4 in parallel, meaning both exist at the same time and operate separately.

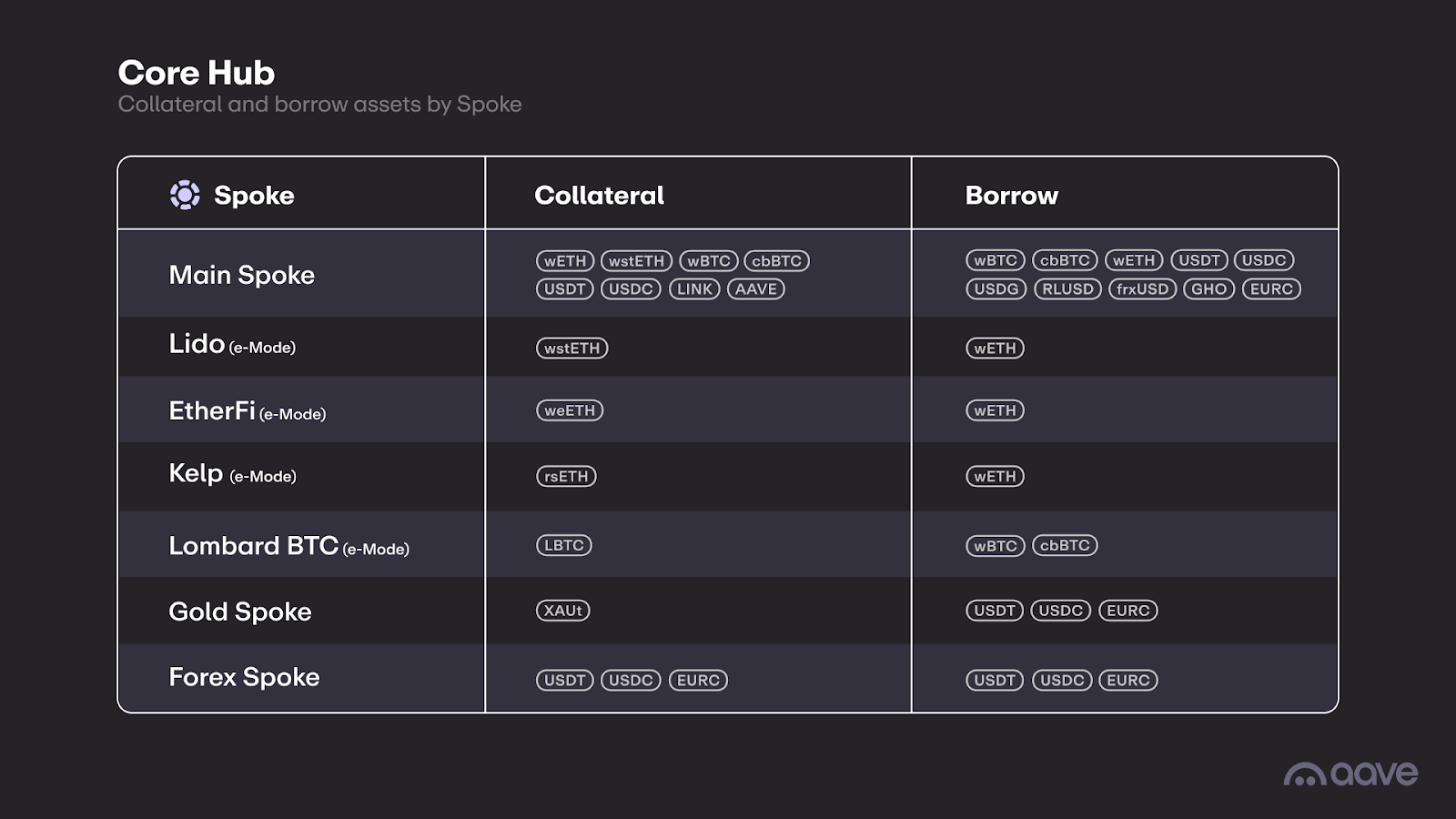

While Aave V3 creates a single bank on each network it is deployed – with commingled assets and shared insolvency risk across all users – V4 introduces a “hub-and-spoke” design, which is intended to make Aave’s lending markets more modular, customizable, and capital efficient.

Essentially, V4 provides the functionality needed to allow for multiple individually siloed Aave liquidity “hubs” to exist simultaneously on the same network, in theory allowing Aave to support a broader range of assets as collateral.

“Hubs” act as shared pools of capital, where users’ lent deposits are aggregated and made available across multiple markets simultaneously. Connected to “hubs” are “spokes,” or individual lending environments that can define their own collateral types, risk parameters, and liquidation rules.

When users supply capital through a spoke, it flows into the hub; when borrowers draw funds, they are pulling from that shared hub liquidity layer.

Although Aave V4 is launching with guardrails attached – the Aave DAO is charged with managing supply/borrow caps and approving new spoke integrations – the possibility of true permissionless market creation cannot be discounted.

In a comment to The Block about V4’s launch, Aave Labs CEO Stani Kulechov alluded to this possibility, stating, "It's going to be DAO-governed, but in the future, there's an ability to actually create permissionlessness. The question is whether the model is safe."

Crucially, V4’s modular, hub-based liquidity model means that these newly created markets don’t have to bootstrap capital from scratch. Builders can spin up bespoke lending markets while tapping into Aave’s shared liquidity layer, keeping capital concentrated while allowing experimentation at the edges.

In a video posted to X, Aave Labs CEO Stani Kulechov highlighted what sets Aave V4 apart from its predecessors.

“The biggest difference between Aave V4 and V3 is that the architecture is completely modular,” Kulechov explained, noting that this design makes the protocol far easier to extend as new use cases emerge. According to Stani, that flexibility promises to unlock entirely new categories of lending, enabling users to borrow against unconventional assets, such as data.

Should that grandiose vision materialize, Aave V4 could incite a gold rush in onchain lending – one that inspires the tokenization of everything from real-world assets to data streams, as investors chase the leverage enabled by Aave’s shared liquidity.

Still, that’s not to say Aave’s path forward will be frictionless.

For starters, new lending markets don’t automatically bootstrap themselves. If an asset lacks established demand, lenders may be hesitant to supply capital, creating a cold start problem for the very markets V4 is designed to enable.

Governance adds another layer of complexity. While the DAO is tasked with managing risk parameters and approving new spoke integrations, this newfound authority comes at a sensitive time. Several key Aave community steward groups exited in recent months, citing concerns around centralization and governance direction.

Ultimately, Aave V4 should be viewed as a new foundation rather than a finished product. Its architecture expands what’s possible, but only time will tell how effectively it delivers.

We're past "in it for the tech" or "in it for the money." MegaETH is bringing you products worth using, powered by USDM.

Not financial or tax advice. This newsletter is strictly educational and is not investment advice or a solicitation to buy or sell any assets or to make any financial decisions. This newsletter is not tax advice. Talk to your accountant. Do your own research.

Disclosure. From time-to-time I may add links in this newsletter to products I use. I may receive commission if you make a purchase through one of these links. Additionally, the Bankless writers hold crypto assets. See our investment disclosures here.